Higher interest rates mean that the next president, whoever it is, will find it much harder to reduce taxes and increase spending.

For all the bold talk of tariffs and price controls, the economic legacy of the next president will mostly depend on something far more mundane: the tax code — specifically, the 2017 Tax Cut and Jobs Act, much of which will expire next year. Whoever is in the White House, working with whichever party controls Congress, will need to decide whether to extend it, change it or let it expire.

Given that Donald Trump favors extending all of it, and Kamala Harris most of it, odds are that the TCJA will survive and most voters will keep their lower tax rates. If so, it may well be the last gasp of the free-lunch era — the delusion the US can cut taxes, increase spending, and never pay the consequences.

But America’s fiscal reality is catching up with its political reality. By the end of the next president’s tenure, if not sooner, politicians will have to start dealing with budget constraints again.

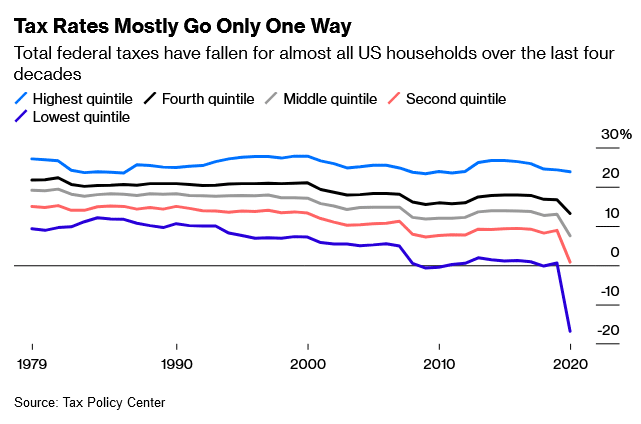

Ever since George H.W. Bush’s presidency, increasing taxes on anyone but the richest Americans has been unthinkable. This may explain why taxes rates have fallen for most Americans over the last several decades, even as the size of government has increased.

This also helps explain why it is so unlikely that either candidate will allow the TCJA to expire. Harris has promised to not increase taxes on anyone who earns less than $400,000, which suggests she will keep all the provisions from the law that apply those earners, who make up about 98% of the working population. Trump plans to make all the provisions of TCJA permanent. Both candidates are also promising tax cuts beyond those in that law, proposing to expand the earned income tax credit and the child tax credit (Harris), eliminate taxes on overtime or Social Security benefits (Trump), or end taxes on tips (both Harris and Trump).

On the spending side, Harris wants to add a new entitlement by having Medicare offer long-term care. She would increase some taxes for high earners as well as the corporate tax rate, and perhaps tax higher earners’ wealth, too.

Overall, Harris’ plan is considered more fiscally responsible — because it increases the primary deficit by only $2 trillion. Trump’s would increase it by $4.1 trillion.

These are both silly numbers, and the fact that the Harris number is less silly should not give voters or bond markets much comfort. Both parties suffer from their own delusions: Republicans that tax cuts and higher tariffs pay for themselves, Democrats that government growth can be funded entirely by higher taxes on rich people.

The question is how long markets will continue to indulge these fantasies. The inflation of the early 2020s, which was caused in part by excess stimulus spending, was a reminder of how reality can intrude. Another reminder may come in the form of rising term premiums as the election nears. Interest rates may fall a bit after the election, but historically speaking, big debt tends to increase rates.

Of course, some people argue that this time is different — but really, it’s the last 20 years that were different. Washington was able to keep spending because investors and foreign governments bought US debt no matter how expensive it got. That may be changing. Foreign appetite for Treasuries is waning both because of other nations face their own economic challenges, and because less trade overall means less need for US Treasuries. Now buyers tend to be investors seeking higher-yielding assets, which suggests that the government may not be able to count on selling its debt and offering such low rates for much longer.

It is possible that faster growth will pay for the debt. But that is a big gamble, especially in a less global and higher-rate environment. Another constraint on policy will be higher inflation, which is more likely with an older population and a more protectionist trade regime. The latest bout of inflation may also have made expectations less stable, pushing up term premiums. On the upside, higher inflation will erode the debt, but at what political cost? Recent history suggests it will be great.

A near zero-rate environment propped up the delusion that profligate fiscal policy was virtually cost-free to taxpayers and politicians alike. In a higher-rate environment, that delusion is harder to sustain. The CBO projects interest payments will take up nearly 4% of GDP in the next 10 years, and eventually exceed 6%. That assumes the 10-year bond rate stays at about 4%. If rates go to 5% or 6%, debt becomes an even bigger burden on the budget. At that level, simply rolling it over pushes up rates and starts to crowd out private investment.

Next year’s debate about the Tax Cut and Jobs Act may be the last one in which each side competes to be more reckless. The US is entering a higher-rate environment, with spending increasing and unfunded entitlements coming due, and demand for debt is changing. Something has to give: Everyone will have to pay higher taxes, or the government will have to spend less.

My bet is on the former. Either way, it’s the end of an era. In fiscal and monetary policy, as in an increasing number of corporate cafeterias, there’s no such thing as a free lunch.

Read the full article HERE.