Jobs numbers for May and June are revised down sharply, while July’s figures fall short of expectations

U.S. job growth slowed in July, a signal that pockets of weakness that had been marring the labor market are starting to take hold.

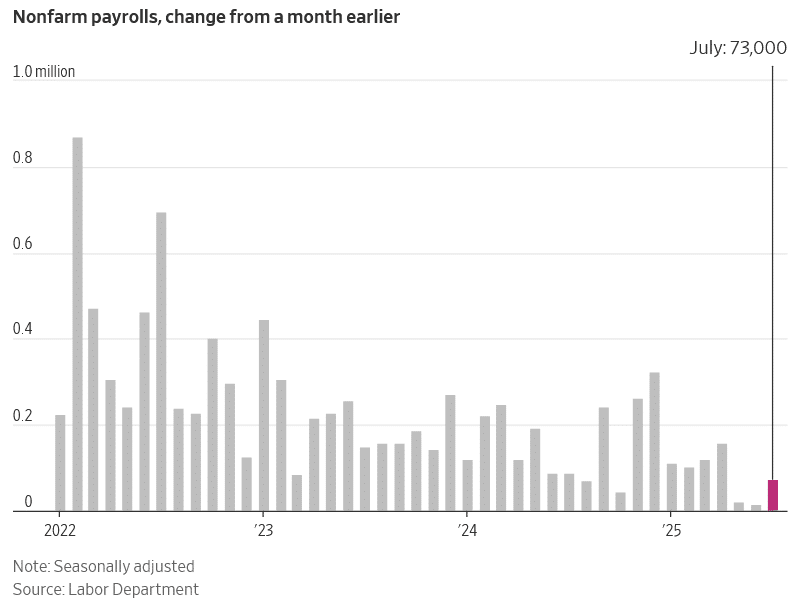

The U.S. added a seasonally adjusted 73,000 jobs in July, the Labor Department reported Friday, below the gain of 100,000 jobs economists polled by The Wall Street Journal had expected to see.

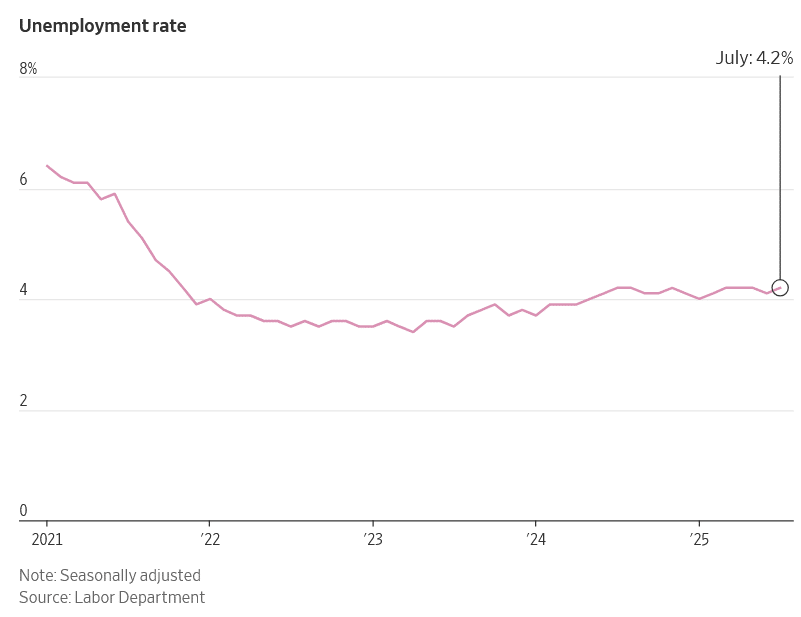

The unemployment rate rose slightly to 4.2% from 4.1%.

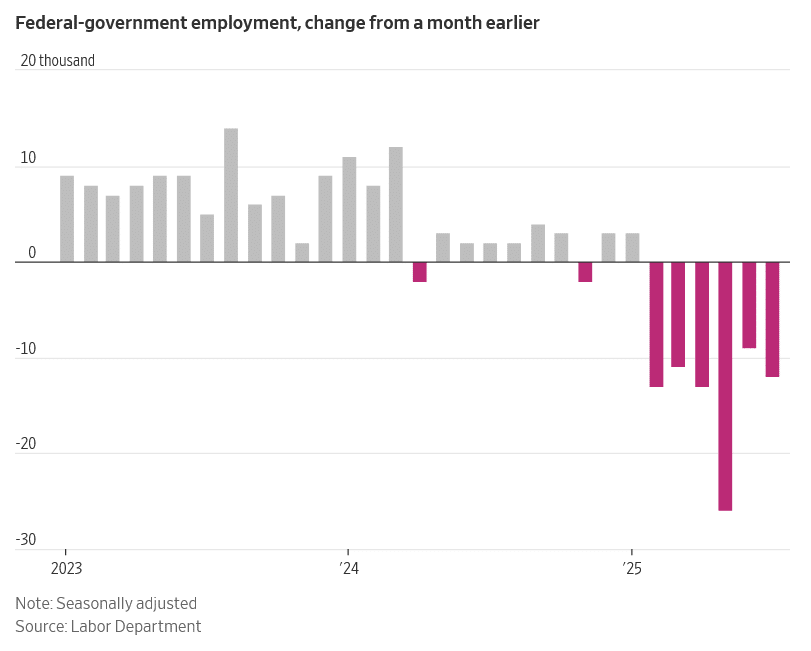

The health care and social assistance sectors accounted for a large share of the new jobs. Those sectors tend to do well no matter how the economy is doing. Federal-government layoffs continued to drag on payrolls, with that sector losing 12,000 jobs.

Hiring in May and June was much weaker than previously reported. Revisions showed employers added a combined 258,000 fewer jobs in those months than previously estimated.

Stock futures were down fell ahead of the report, after President Trump raised tariffs on scores of countries Thursday. They remained in the red afterward. The weak jobs data is likely to fuel bets on Federal Reserve rate cuts.

July’s report comes as economists and policymakers are trying to figure out which of two competing narratives about the economy is more true.

One view is that of surprising resilience. Tariff threats, though they have started to seep into some prices, have yet to translate into pronounced inflation. Consumers, after holding back earlier in the year, are feeling a bit more confident.

The other perspective is that cracks are starting to appear and could deepen. Some companies, such as Procter & Gamble and Chipotle Mexican Grill, are reporting that customers are becoming more sensitive to prices. Young consumers in particular are cutting back on discretionary spending, and much of the economy’s growth is being driven by the wealthiest Americans.

“Everyone is trying to understand what direction the economy is taking,” said Jonathan Pingle, chief U.S. economist at UBS.

Guy Berger, senior fellow at labor-market think tank Burning Glass Institute, is of the opinion that the economy is still stable.

“You look at almost every major indicator,” Berger said, “and they have all been pretty steady since last fall.”

One factor that hasn’t been steady, though, is the policy backdrop. “I would not bet a lot of money on things staying stable going forward,” Berger said, citing tariffs, restrictions on immigration and a big new tax bill.

Economists are paying particular attention to changes in the supply of workers. A dramatic decrease in border crossings is constraining the number of people from abroad coming into the labor force. High-profile immigration raids are keeping many workers at home. Meanwhile, the U.S. is aging, boosting retirements and limiting the number of younger people joining the workforce.

A year and a half ago, the economy needed to add 166,000 jobs a month to keep the labor market steady, according to Peterson Institute for International Economics senior fellow Jed Kolko. As of June, Kolko said, the needed number was only 86,000.

“It’s fallen so much because this immigration surge has ended,” Kolko said. In other words, a job creation number that might have looked lackluster a year and a half ago might actually be strong today.

Recently, the number of jobs created each month has been slowing, but the unemployment rate has risen only slightly.

“People are going to have to get used to employment gains that are meh that will not tell us on their own that the job market is weak,” said Berger. “That is a weird thing for people to get used to.”

Read the full article HERE.