The view from the summit doesn’t look so good.

Clouds and vertigo have tempered the S&P 500’s new all-time highs in the form of heavy tariff threats, brewing discontent from trading partners and political allies, and a growing apprehension that inflation’s reacceleration — just barely under control — will only get worse.

Investors are still riding the momentum of the Trump bump and the continued growth of corporate earnings. The S&P’s new heights and swelling portfolios can attest to that. But the stock charts also seem to be masking the anxiety of the current moment, which has seen consumer sentiment fall to a seven-month low.

Why does it feel like a storm is coming despite the market’s fear gauge, the CBOE Volatility Index, showing calm seas?

Perhaps it’s because things look… different. As Josh Schafer wrote yesterday, European stocks are beating American stocks. People are especially excited about gold. And the frothy meme stock and crypto enthusiasm has faded. Even the Magnificent Seven aren’t very magnificent, with Meta Platforms (META) breaking away. To be clear, these aren’t bad things. But they add to an unfamiliarity, a cousin of anxiety that’s been brewing.

“Short-run market and economic expectations, fear and doubt index, and inflation all moved in negative direction by magnitudes not seen since 2022,” Andy Reed, Vanguard’s head of investor behavior, wrote in a note Wednesday on Vanguard’s investor sentiment survey, pointing out falling expectations for GDP and the stock market. “It looks like 2022 all over again, but this time is different.”

The elephant in the room is, of course, inflation — the figure behind both the poor consumer sentiment numbers and some of the market’s recent moves. And they all come back to the biggest GOP elephant of them all, President Trump.

The latest round of tariffs, announced earlier this week, were fresh 25% levies on imported cars and similar duties on pharmaceuticals and semiconductors. They wouldn’t kick in until later in the year, giving time for foreign companies to bring investments and operations to US shores. At least, that’s how Trump says things could unfold for those transactional-savvy entities wishing to avoid the duties.

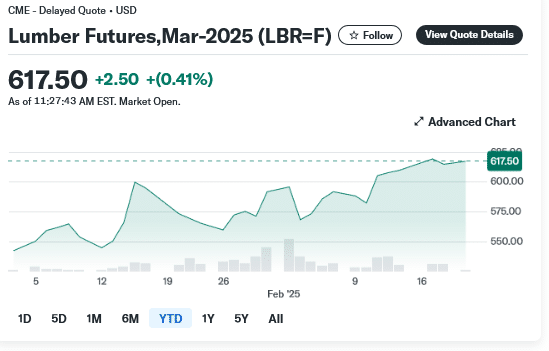

But even the threats of tariffs matter: Just look at lumber futures, despite the Canadian reprieve.

For now this unease stays locked out of the soaring S&P 500, perhaps owing to the extended timeline or to a growing insensitivity to Trump’s threats. (And markets haven’t been reacting to his social media posts like they used to, data shows.)

And this is unusual. Vanguard’s Reed noted that concerns over market and economic crashes typically move in lockstep, but are diverging historically as “investors now see higher chances of an economic disaster than a market crash.”

It’s hard to tell, though, if this is Wall Street’s numbness to Trump’s outlandishness or a calculation that all the trade war noise is just another gambit in the art of the deal and not something that will erase growth and boost inflation.

Still, there’s a measured sense that crisis of some kind will come, whether people plan for one or not.

“Investors normally show robust optimism, even in the face of bad news, and their expectations were flying high in 2024 alongside the market,” Reed wrote. “But since October, investor expectations and concerns over tail risks moved sharply in the negative direction and much closer to those of economists, while inflation concerns loom large.”

Trump’s allies in Washington and in the media have attempted to deflect criticisms of price increases with a plea for more time, and the White House’s economic advisers have a plan to bring down borrowing costs for Americans by boosting economic growth and productivity while cutting government spending.

It’s only been a month, and the lag of economic data gives the president another buffer, as does the Fed’s wait-and-see approach.

But if Trump’s saber-rattling and legislative agenda turn out to be inflationary, the central bank’s next cut will seem more and more like a mirage.

And without the monetary relief that Wall Street has long counted on, the gains of Trump’s first days in office may prove to be even more fleeting.

Read the full article HERE.

Following uncertainty in the global economy caused by Donald Trump’s tariff policy, gold price today witnessed strong buying in early morning deals. MCX gold rate opened upside at ₹84,946 and touched an intraday high of ₹ ₹85,162 per 10 gm within a few minutes of the Opening Bell on Monday. In the international market, the COMEX gold price oscillates around $2,915 per troy ounce, while the spot gold price hovers around the $2,904 per ounce mark (at 9:50 AM).

According to market experts, the gold rate today is on an uptrend because of two factors: the US dollar rate hitting a two-month low and uncertainty surrounding US trade policy. They said that gold prices are expected to remain in a bull trend and predicted $3,000 and $3,080 per ounce if the economic uncertainty caused by Donald Trump’s tariff policy doesn’t end soon.

Weakness in the US dollar rates

On the immediate reason fueling the gold price today, Anuj Gupta, Head—Commodity & Currency at HDFC Securities, said, “The Gold rate today is in a bull trend due to two factors: the US dollar rate hitting a two-month low and uncertainty surrounding US trade policy. ”

Why is the gold price skyrocketing?

Ventura Securities says, “With the increased US trade tariffs, there’s a lot of uncertainty surrounding the U.S. trade policy. These have increased the demand for safe-haven assets like Gold. Spot gold hit a record high of $2,943, and Comex gold $2968 an ounce. There are talks around about tariffs on gold, which also has sparked a rush for the physical metal in London, Switzerland and Asia to ship to the US ahead of any new levy.”

Rising demand by central banks

Pointing towards the rising demand by central banks for the precious yellow metal, Ventura Securities said, “Gold price keeps trading at record highs on the back of increasing demand by central banks for their reserves to maintain an expected surge in fiscal deficits which could raise inflation manifold and probably a recessionary fear across the globe. Central banks acquired 1,045 tons of gold in 2024, marking the 3rd consecutive year of purchases surpassing 1,000 tons. Central banks bought more gold over the last 3 years than in 6 years before 2022.”

Gold price outlook

Ventura Securities said on the outlook for gold prices, “Gold price today seems to head $3,000 per ounce and likely to well cross $3,080. The recent strength stems from a mix of higher tariff safe haven demand, geopolitical uncertainties, inflation concerns, central bank policies, and continued strong demand from both central banks and retail investors.”

Gold price today: Other triggers to look at

Gold price is pressured due to the strength of Treasury yields and dollar bias after Federal Reserve Chair Jerome Powell has been cautious and flagged as not hurrying to cut interest rates.

Powell also noted that US monetary policy had been sufficiently loosened after 100 basis points of rate cuts through 2024 (From 5.50% to 4.50%).

Due to the strength of the USD, bigger gains in gold are restricted, and interest rates are still elevated. Since US importers face inflation due to tariffs, the FED has less impetus to cut interest rates. High interest rates present more pressure on non-yielding assets like gold.

CPI inflation data for January was 3.0% YOY as expected from December (Rose 2.9% YOY). A stronger CPI report could prove more damaging for riskier assets but may boost the US dollar.

Powell says, “If the economy remains strong and inflation does not continue to move sustainably toward 2 per cent, we can maintain policy restraint for longer. If the labour market were to weaken unexpectedly or inflation was to fall more quickly than anticipated, we can ease policy accordingly.”

“Gold will continue to be volatile, but as long as “uncertainty” prevails, it is likely to remain bullish,” Ventura Securities report said.

Read the full article HERE.

Gold’s (GC=F) glittering run in 2025 may have more room to rise higher, Goldman Sachs believes.

On Tuesday, the investment bank lifted its year-end price target for gold to $3,100 an ounce, from $2,890 previously. Goldman says “structurally higher” central bank demand will add 9% to the price of gold by the end of the year, also helped by a slight boost from ETF holdings.

But Goldman added that concerns about President Trump’s tariffs could be an “upside” risk to gold prices.

“However, if policy uncertainty — including tariff fears — stays high, higher speculative positioning for longer could push gold prices as high as $3,300 an ounce by year-end,” Goldman strategist Lina Thomas wrote in a note to clients.

In a gold note of its own today, UBS said it could see a path for gold hitting $3,200 an ounce.

“A more forceful rally relative to our previous expectation is likely to be driven by deep-rooted bullish sentiment, with gold seen as a safe-haven asset amid a highly uncertain and volatile macro environment,” UBS said.

Precious metals such as gold are currently having a solid ride some two months into the year, as investors hedge their exposure to stocks amid uncertainty over policy from the Trump administration and the Federal Reserve.

Year to date, gold prices are up 9.7%% to $2,925 an ounce. They are hovering around record highs. Over the past year, gold has gained an impressive 43%. By comparison, the S&P 500 (^GSPC) and Dow Jones Industrial Average (^DJI) are up over 20% and 15%, respectively.

Meanwhile, silver (SI=F) prices are over 40% higher for the year, and platinum (PL=F) prices are up more than 10%.

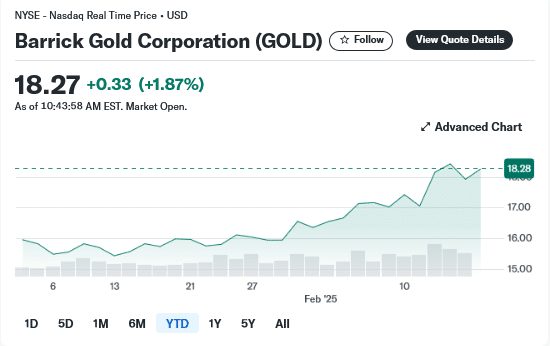

Stocks exposed to the gold trade have subsequently come on strong.

Shares of gold miner Barrick Gold (GOLD) have gained 16% year to date. At the same time, the SPDR Gold Shares ETF (GLD) has tacked on 10%.

Barrick Gold, in particular, is basking in gold’s record run.

The miner posted its highest net earnings in a decade last year. Operating cash flow in the fourth quarter rose 18% to $1.4 billion, bringing the total for the year to $4.5 billion. It marked the highest level hit for the company since 2020. Barrick Gold sent $500 million on share buybacks last year and $700 million in dividends.

“Gold is becoming more important as a safe haven in a geopolitically uncertain world,” Barrick Gold CEO Mark Bristow told analysts on an earnings call last week. “Needless to say, it’s an exciting time to be a gold and copper miner with more upside in the commodity price, in my opinion, anyway.”

Some traders, however, think a short-term pause in gold prices is nearing, given its rapid ascent in value.

“There are signs of short-term exhaustion,” New York Stock Exchange strategist Michael Reinking said in a note.

Noted veteran trader Kenny Polcari said: “It feels a bit tired to me … it feels a bit stretched … so while I like gold as part of a portfolio — I am not chasing it … up here.”

Read the full article HERE.

Some fear growing speculation in options, meme stocks and crypto

Investors are fearful that some market gains are outpacing typical measures of underlying value after strong economic growth helped power the S&P 500 to record after record in a nearly two-year bull market.

Trade wars and DeepSeek’s challenge to the AI boom have barely dented the enthusiasm. Meme stocks are back, options are on fire and bitcoin is trading around $100,000. That makes some traders nervous, because rising speculation can lead to market imbalances that at times presage sharp corrections.

“There have been signs of froth for a while,” said Seema Shah, chief global strategist at Principal Asset Management. “The market is vulnerable to disappointment.”

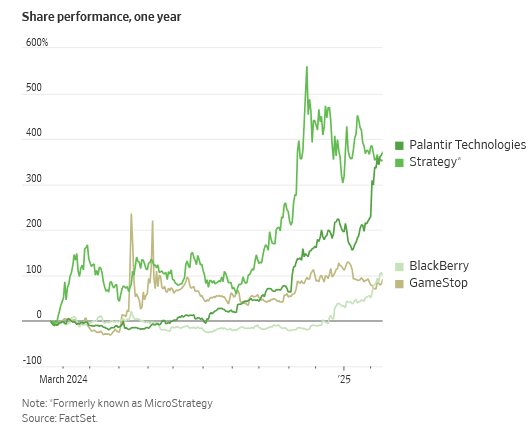

One source of concern: Ordinary investors are really bullish about a handful of popular companies.

Shares of Palantir Technologies, a highly popular stock among individual investors, surged 24% on Feb. 4 after the data-analytics company reported strong sales growth and robust demand for its artificial-intelligence products. Palantir’s stock has jumped roughly 58% this year and was last year’s best performer in the S&P 500.

Traders are also bidding up shares of Strategy, formerly MicroStrategy, the software company turned bitcoin-buying machine. The company’s market capitalization was recently about $87 billion, nearly twice the value of the bitcoins it holds.

Meme stocks have also jumped. Shares of GameStop, BlackBerry and online pet-products retailer Chewy have all soared more than 90% over the past 12 months, according to FactSet.

“There’s always stocks that it’s hard to understand what the market sees,” said Michael Brenner, asset allocation strategist at FBB Capital Partners. “You are starting to see some of these things stack up. And then the question just becomes, are there enough of these things to tip the market over?”

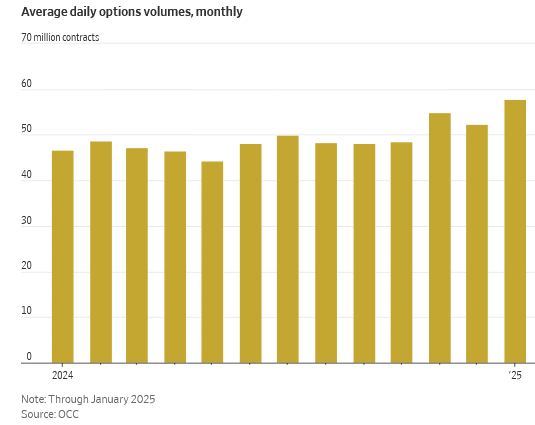

Activity is surging in options contracts, which give traders the right to buy or sell a stock at a set price. Options are a popular play among traders seeking bigger payouts than traditional buy-and-hold investing. But those bets can quickly go south, too.

About 58 million options changed hands daily on average in January, a monthly record in data going back to 1973, according to equity derivatives clearing organization OCC. That follows a record year for options trading volumes in 2024.

Zero-day-to-expiry options tied to the S&P 500 saw record trading volumes on Jan. 31, according to Cboe Global Markets. So-called 0dte options contracts, among the market’s riskiest trades, allow investors to bet on whether stocks will rise or fall by the end of the day.

Speculators are venturing beyond traditional stocks and bonds, too.

Prediction markets, where users bet on the likelihood of future events, have offered an array of contracts since some investors won big betting on President Trump’s election victory. They have listed contracts tied to everything from Federal Reserve meetings to the Los Angeles wildfires to Luigi Mangione, the suspect in the killing of healthcare executive Brian Thompson.

Americans are also embracing sports gambling on platforms such as DraftKings and FanDuel. And speculators are rushing back into cryptocurrencies, which are prone to unpredictable boom-and-bust cycles.

Bitcoin, one of the hottest trades, reached an all-time high of $109,224.74 in January, boosted by optimism that the Trump administration will usher in a golden age for crypto. It traded around $97,215.64 as of 4 p.m. ET on Friday.

Investors have piled into exchange-traded funds tied to the cryptocurrency, funneling nearly $17 billion into U.S.-listed spot bitcoin ETFs since Election Day, according to Morningstar Direct data through Wednesday.

Meme coins, or digital tokens that serve no economic purpose and whose value is based on the popularity of internet memes, have also taken off. The market value of coins launched by Trump and first lady Melania Trump, dubbed $TRUMP and $MELANIA, have peaked at about $15 billion and $2 billion, respectively, since their January debut, according to CoinMarketCap.

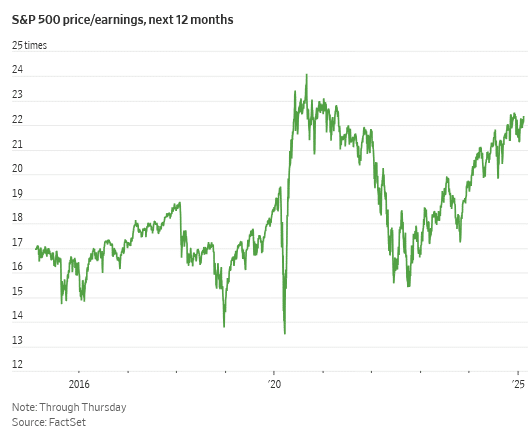

Meanwhile, stocks look generally expensive.

Companies in the S&P 500 recently traded at 22 times their expected earnings over the next 12 months, according to FactSet. That is above their 10-year average price/earnings ratio of 19 and within striking distance of the 26 hit in 2000 before the dot-com crash.

While stretched valuations don’t necessarily portend a selloff, they can weigh on long-term returns and make continuing growth in corporate profits more important to stock performance.

Strong earnings growth has helped support the rally this year: Companies in the S&P 500 have reported a 16.7% jump in profit so far this reporting season.

Some analysts warn that elevated interest rates could cut into those profits. Fed Chairman Jerome Powell reiterated last week that the central bank is in no rush to lower borrowing costs. Consumer prices in January rose by their highest monthly rate since August 2023, the latest in a string of warm inflation reports.

“There is a sense that the Fed is in an easing cycle,” said Roger Aliaga-Diaz, Vanguard’s global head of portfolio construction. “If that were to interrupt because inflation is starting to pick up again…that will be a little bit of a shock to the market.”

Read the full article HERE.

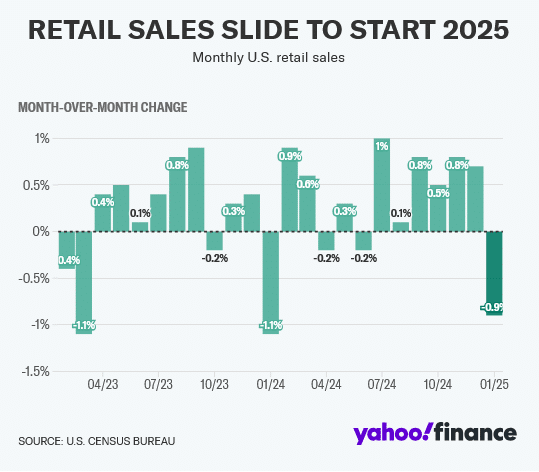

New data out Friday showed retail sales declined more than expected in the first month of 2025.

Headline retail sales fell 0.9% in January, more than the 0.2% decline economists had expected, according to Bloomberg data. This marked the largest month-over-month decline in retail sales since January 2024.

Retail sales in December were revised up to 0.7% from a prior reading that showed a 0.4% increase in the month, according to Census Bureau data.

“The traditional holiday hangover and a nasty winter freeze combined to cool topline retail sales,” RSM chief economist Joe Brusuelas wrote in a post on X.

The control group in Thursday’s release, which excludes several volatile categories and factors into the gross domestic product (GDP) reading for the quarter, declined by 0.8%. Economists had expected a 0.3% increase.

January sales, excluding auto and gas, fell 0.5%, also below consensus estimates for a 0.3% increase. A 4.6% decline in sporting goods and hobby sales led the declines while sales at motor vehicle and parts dealers fell 2.8%.

Friday’s retail sales data wrapped up a busy week of economic data releases. Earlier in the week, two fresh inflation readings for the month of January showed prices increased more than Wall Street had expected but economists found positive news for markets and the Federal Reserve within the details

When evaluating categories from both the Consumer Price Index (CPI) and Producer Price Index (PPI) that feed into the Fed’s preferred inflation gauge, the Personal Consumptions Expenditures (PCE) index, economists argue price increases likely slowed in the month of January. “Core” PCE, which excludes the volatile categories of food and energy, is expected to clock in at 2.6% in January, down from the 2.8% seen in December.

As of Friday morning, markets see less than a 50% chance the Federal Reserve cuts interest rates until at least its July meeting, per the CME FedWatch tool.

Read the full article HERE.

Producer-price index rises sharply early in 2025

The numbers: Wholesale prices rose sharply in January in another sign that lingering inflationary pressures in the economy will keep high U.S. interest rates from falling much anytime soon.

The producer-price index increased 0.4% last month, the government said Thursday. Economists polled by The Wall Street Journal had forecast a 0.3% gain.

The increase in wholesale inflation in the past 12 months rose to 3.5% from 3.3%. That’s the highest rate in almost two years.

The PPI report follows a sharp uptick in consumer prices in January, which rattled financial markets and raised the possibility of the Federal Reserve not cutting interest rates this year.

High borrowing costs have punished home buyers and made it more expensive for people to buy cars. The cost of borrowing has also discouraged business investment.

High rates tend to slow the economy over time, however, and reduce the rate of inflation. The Fed has paused further rate cuts until it sees more evidence that inflation is decelerating again.

Key details: The core rate of wholesale inflation, which omits volatile food, energy and trade margins, rose 0.3% last month.

The 12-month core rate slipped to 3.4% from 3.5%, however.

Core inflation rates in the PPI, CPI and the Fed’s preferred PCE price index are seen as better predictors of future trends. The Fed is aiming to reduce inflation more broadly to a low 2% annual rate.

The cost of services, one of the biggest drivers of inflation in the past few years, rose for the sixth straight month and didn’t offer much relief. Service prices are up 4.1% in the past year.

The cost of wholesale goods jumped 0.6% in January, mostly because of higher oil prices.

Food prices leapt 1.1% in January, largely because of a spike in the cost of eggs. Another outbreak of the bird flu forced chicken producers to slaughter millions of birds, leading to shortages and soaring prices.

Further down the pipeline, the rising cost of raw materials appears to be one of the biggest sources of inflationary pressures.

Most of the increase has taken place in the past several months, with raw material costs up almost 9% in the past year.

Big picture: Inflation is too high to justify a further reduction in borrowing costs.

What’s still unclear is the impact of President Trump’s economic agenda. Some of his policies could boost the economy, but others — such as tariffs — threaten to raise prices and add to inflation.

Looking ahead: The “stronger-than-expected PPI helps to confirm, especially after Wednesday’s hot CPI, that inflation did indeed come roaring back in January, and makes the Federal Reserve’s path much clearer, since there is arguably zero reason to cut interest rates right now,” wrote Paul Stanley, chief investment officer of Granite Bay Wealth Management.

Market reaction: The Dow Jones Industrial Average and S&P 500 were set to open mixed in Thursday trading.

Read the full article HERE.

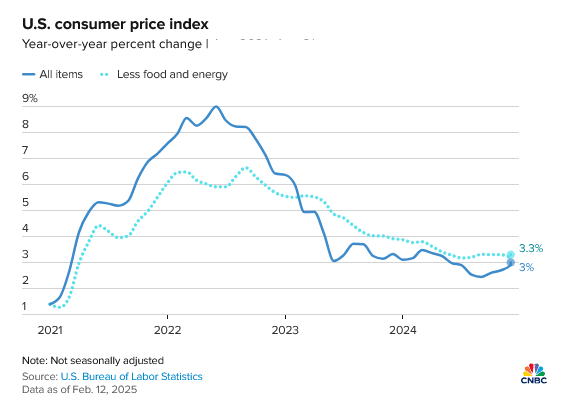

- The CPI accelerated a seasonally adjusted 0.5% for the month, putting the annual inflation rate at 3%, both higher than expected. The core CPI ran at 0.4% and 3.3% respectively, also above forecast.

- Shelter costs continued to be a problem for inflation, rising 0.4% on the month. Food prices jumped 0.4% and energy prices climbed 1.1% as gasoline prices increased 1.8%.

- Markets largely expect the Fed to stay on hold for an extended time and pushed the next rate cut probability out to September following the CPI report.

Inflation perked up more than anticipated in January, providing further incentive for the Federal Reserve to hold the line on interest rates.

The consumer price index, a broad measure of costs in goods and services across the U.S. economy, accelerated a seasonally adjusted 0.5% for the month, putting the annual inflation rate at 3%, the Bureau of Labor Statistics reported Wednesday. They were higher than the respective Dow Jones estimates for 0.3% and 2.9%. The annual rate was 0.1 percentage point higher than December.

Excluding volatile food and energy prices, the CPI rose 0.4% on the month, putting the 12-month inflation rate at 3.3%. That compared with respective estimates for 0.3% and 3.1%. The annual core rate also was up 0.1 percentage point from December.

Markets tumbled following the news, with futures tied to the Dow Jones Industrial Average sliding more than 400 points while bond yields scaled sharply higher.

“The ‘wait and see’ Fed is going to be waiting longer than anticipated after a red-hot January CPI inflation report,” wrote Josh Jamner, investment strategy analyst at ClearBridge Investments. “This report puts the final nail in the coffin for the rate cut cycle, which we believe is over.”

Shelter costs continued to be a problem for inflation, rising 0.4% on the month and accounting for about 30% of the entire increase, the BLS said. Within the category, a metric in which homeowners estimate what they could get if they rented their homes increased 0.3% on the month and was up 4.6% on an annual basis.

“Shelter costs continue to be the main driver of core inflation as higher mortgage rates push more Americans into a rental market in which vacancy rates are near record lows,” said Erik Norland, chief economist at CME Group. “Traders appear to believe that today’s data make additional Fed cuts less likely than they had expected previously.”

Food prices jumped 0.4%, pushed by a 15.2% surge in egg prices related to ongoing problems with avian bird flu that have forced farmers to destroy millions of chickens. The bureau said it was the largest increase in egg prices since June 2015 and it was responsible for about two-thirds of the rise in food-at-home prices. Egg prices have soared 53% over the past year.

Nonalcoholic beverages posted a 2.2% gain over the past 12 months, while in January tomatoes fell 2% and other fresh vegetables declined 2.6%.

New vehicle prices were flat, but used cars and trucks saw a 2.2% increase and motor vehicle insurance was up 2%, pushing the annual gain to 11.8%. Energy prices climbed 1.1% as gasoline prices rose 1.8%.

The report comes a day after Fed Chair Jerome Powell indicated the central bank could be on hold for a while when it comes to interest rates. Powell told members of the Senate Banking Committee that he thinks the Fed doesn’t need to be in a rush to lower rates as it evaluates progress on inflation and as President Donald Trump continues plans to levy tariffs against imports.

Markets largely expect the Fed to stay on hold for an extended time and pushed the next rate cut probability out to September following the CPI report, according to CME Group data. Traders also implied about a 70% probability that the Fed will cut only once this year.

Trump, though, is still pushing for lower rates. In a post on Truth Social about half an hour before the CPI release, the president said, “Interest Rates should be lowered, something which would go hand in hand with upcoming Tariffs!!!”

The CPI release, though, could complicate further easing in monetary policy.

The jump in prices ate into worker paychecks, as the CPI increase entirely offset the 0.5% move higher in average hourly earnings, the BLS said in a separate release.

Read the full article HERE.

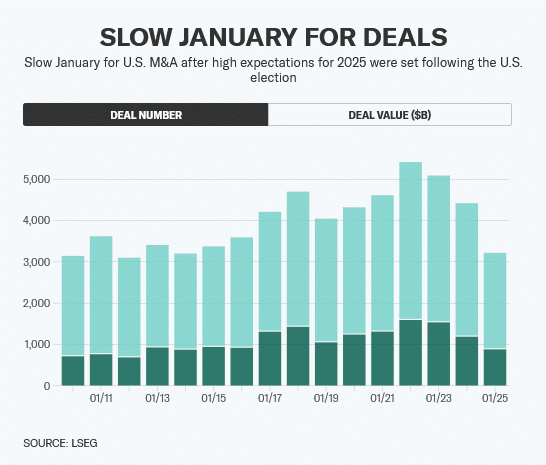

The start of Trump 2.0 is not quite what Wall Street expected.

Dealmaking had its slowest month in January in more than a decade. A prized tax break for hedge funds and private equity firms came under threat. And big banks got grilled over whether they “debanked” certain customers.

These complications were not part of the plan when Donald Trump was elected in November, an event that set off a round of optimistic predictions about an M&A boom, looser rules and a more favorable approach to big Wall Street firms in Washington, DC.

Instead bankers ended January with the lowest number of announced M&A deals within the US since that same month in 2014, according to LSEG data.

Trump’s new antitrust cops also signaled in the administration’s second week that they weren’t going to give a free pass to big mergers by blocking a potential union between Hewlett Packard (HPE) and rival Juniper Networks (JNPR).

And new uncertainties surrounding the president’s tariff plans are leaving many businesses unsure about when to make big moves and what direction borrowing costs might take in the weeks and months ahead.

“The uncertainties that we see from a geopolitical standpoint of view, around tariffs are — is definitely creating a little bit of uncertainties that may dent the capabilities for us, for everybody to execute,” Sergio Ermotti, CEO of UBS Group AG (UBS), told analysts Monday while speaking at a UBS financial services conference in Miami.

Ermotti was also quick to point out that “it’s not 1 quarter or 1 month” that will determine the year.

And to be sure, January can typically be a slower time for new deals than other parts of the calendar.

“It’s not surprising that a month and a half after the election, you don’t see a flood of responsive things to that. I do think it will pick up during the year,” Goldman Sachs CEO David Solomon said of the M&A environment on Tuesday at the same event.

The historically high level of corporate valuations may also be playing a role in a slower pace of dealmaking to start 2025, THL Partners co-CEO Scott Sperling told Yahoo Finance Live.

“That’s an unusual combination, and that, in and of itself, may have muted some of the financial returns that would be possible from certain types of M&A and certain types of deal doing,” Sperling told Yahoo Finance Live.

So far the downturn is not pulling down big bank stocks.

Since the beginning of January, JPMorgan Chase (JPM), Goldman Sachs (GS), Citigroup (C) and Wells Fargo (WFC), have risen between 12% and 15% as of Monday while Bank of America (BAC), and Morgan Stanley (MS) are up between 6% and 9%. All have outperformed major stock indexes in that period.

‘What you’re doing is wrong’

One big unexpected development for Wall Street in the early weeks of Trump 2.0 is a high level of political heat.

First President Donald Trump publicly confronted Bank of America (BAC) CEO Brian Moynihan at the World Economic Forum over a claim gaining traction in conservative circles: that customers are being ‘debanked’ for their personal beliefs or because they are part of the crypto industry.

The president also appeared to include JPMorgan Chase CEO Jamie Dimon in his confrontation. JPMorgan and Bank of America are the nation’s two largest banks. Both companies denied the claims they cut off their services to customers over personal beliefs.

“I don’t know if the regulators mandated that because of Biden or what, but you and Jamie and everybody else, I hope you open your banks to conservatives because what you’re doing is wrong,” Trump told Moynihan during a question-and-answer session.

The GOP kept a spotlight on the debanking issue last week during hearings before Senate and House committees. Massachusetts Democrat Senator Elizabeth Warren even signaled her support for the topic, saying she agreed with Trump.

Banks are still optimistic, however, that fixing that issue could ultimately turn out to be a positive for them if regulators relax some of their requirements that force banks to shed certain customers.

They have argued that US rules such as the Bank Secrecy Act discourage banks from dealing with customers that are considered high-risk — and that there needs to be clearer regulation on that front.

Industry lobbyists are pressing for that to happen. “An important part of the solution is fixing the regulatory structure,” a spokesman for the bank industry advocacy group BPI said in a statement to Yahoo Finance.

Lobbyists for the private equity and hedge fund industries may also be unexpectedly busy this year after the White House made it clear that Trump wants to close a tax break known as a carried interest deduction.

It allows investment managers to pay a lower capital gains tax rate on the income they receive from their work as compensation. It’s no small matter, with many capital gains subject to 23.8% taxes while the rate for regular wage income can be double that.

“The president is committed to working with Congress to get this done,” White House press secretary Karoline Leavitt said last week.

Read the full article HERE.

- Trump to announce 25% steel and aluminium tariffs

- New tariffs reflect more uncertainty in global trade -analyst

- Bullion hits a record high of $2,910.99 per ounce

- US CPI, PPI due later this week

Gold prices continued their record rally on Monday and broke through the key $2,900 level for the first time, driven by safe-haven demand as U.S. President Donald Trump’s new tariff threats amplified trade war and inflation concerns.

Spot gold surged 1.6% to $2,905.25 per ounce, as of 09:43 a.m. ET (1443 GMT), after hitting a record high of $2,910.99 earlier in the session. U.S. gold futures jumped 1.5% to $2,930.90.

“Obviously the tariff war is behind the rise; it just reflects more uncertainty and more tension in the global trade situation,” said Marex analyst Edward Meir.

Trump announced plans on Sunday to impose an additional 25% tariff on all steel and aluminium imports. He also said he would announce reciprocal tariffs this week, matching rates imposed by other countries and applying them immediately.

Tariffs may exacerbate U.S. inflation, with investors awaiting U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) data due later in the week.

If the CPI and PPI data surprise on the downside, it may weigh on the dollar and inflate gold prices, while an upside surprise could push up U.S. yields and strain gold, albeit mildly due to the market’s resilience and buyer interest during dips, Meir said.

Federal Reserve Chair Jerome Powell is also due to testify before Congress on Tuesday and Wednesday.

Bullion has already hit its seventh record high this year, driven by Trump’s tariff threats, which have fueled uncertainty over global growth, trade wars, and high inflation, prompting investors turn to gold as a safe-haven asset.

Phillip Streible, chief market strategist at Blue Line Futures, said gold’s 45-degree rally since December might create a self-fulfilling prophecy of further price increases, potentially leading it to raise its forecast to around $3,250 or $3,500.

Spot silver rose 1% to $32.12 per ounce after hitting a three-month high on Friday.

Platinum added 1.1% to $986.80 and palladium gained 2.2% to $985.50.

Read the full article HERE.

For the past several years, gold prices have staged a historic rally while silver has largely struggled to keep up. For investors, that could mean a buying opportunity.

It has been a great time to invest in gold which outperformed the S&P 500SPX-0.27% in 2024, and continued to shine in 2025. It hit a new high of $2,893 an ounce Wednesday but slipped to $2,876 on Thursday afternoon.

Silver has also performed for investors, but not quite as well. It returned 12% a year on average for the past three years, compared with 16% for gold.

On Thursday, silver traded at $32.65 an ounce, about 7% below its 12-month high of $35.04, reached Oct. 22, according to Dow Jones Market Data. Given that the two metals’ prices typically move together, that could mean silver is poised for a rally.

“While gold has broken out and continues to act well, silver remains below the highs hit in October,” wrote Jeff Jacobson, head of derivative strategy at 22V Research, in a note Wednesday.

Gold’s strength has widened the price differential between the two metals, he added, potentially setting the stage for a silver “catch-up” rally. We “have seen silver stage sharp rallies on both an absolute basis, as well as relative to gold, the last two times the silver/gold spread has gotten to these levels,” he wrote.

There are also fundamental reasons to be bullish on silver.

The supply of silver has been largely stagnant for the past decade. A big reason: Unlike gold which is mined directly, about three-fourths of silver is produced as a byproduct of other metals, such as lead, zinc, and copper. Prices for many of these base metals have been soft lately, giving miners less reason to dig them up.

As a result, the global supply of silver is expected to increase just 3% in 2025, forecasts the Silver Institute, a trade group. “Silver may be rallying, but miners are not getting the signal to increase activity” because their financial incentives are elsewhere, said Nitesh Shah, head of commodities research at WisdomTree.

At the same time, demand has been increasing steadily, largely thanks to a surge in interest in solar panels, an important industrial use for the metal. President Donald Trump’s election hit U.S. solar companies hard. But the U.S. is a relative sideshow when it comes to the global solar picture. China produces about 80% of the world’s solar panels, and the country has no plans to let up on its green energy push.

Solar’s share of global energy capacity is expected to surge to about 13% by 2028 from 5%, wrote Imaru Casanova, a portfolio manager at Van Eck, in a recent note. “The implications for silver are clear,” she said.

Read the full article HERE.