The fundamental message is that we’re close to the limits of growth

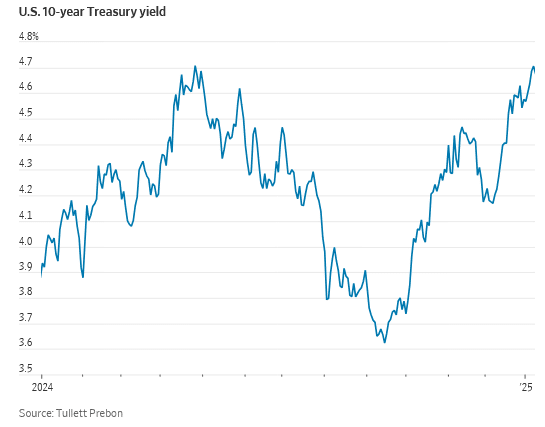

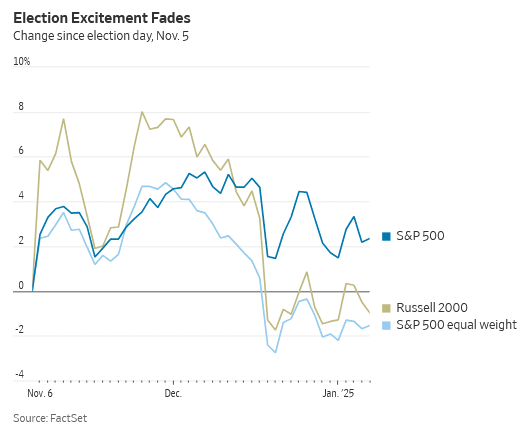

The 10-year bond yield came within a whisker of its high from last April on Wednesday morning, and stocks, especially smaller stocks, didn’t like it one bit.

It is part of a switcheroo by investors over the past month. They have shifted from thinking that higher Treasury yields are just an unwelcome side effect of the stronger growth promised by president-elect Donald Trump, to worrying that higher borrowing costs might end up being very important. If the concern is right, get ready for a bumpy ride in 2025.

The story really starts with the excitement in the run up to, and shortly after, the election. Stocks and bond yields both soared, as investors anticipated a ton of good stuff from a new Trump administration: deregulation and lower taxes to boost growth and tariffs to extract concessions from other countries. Higher bond yields didn’t matter with so much good stuff to dream about.

It took only a few weeks for reality to kick in. Trump might not do only the good stuff, with promised deportations and permanent, rather than negotiable, tariffs pushing growth down and inflation up.

Just as bad, the risk is growing that the economy can’t cope with much of the good stuff. When the economy grows faster than is sustainable the result is either inflation or higher interest rates, or both. Bond yields rose in anticipation.

By Christmas smaller stocks and the equal-weighted version of the S&P 500—which treats pipsqueaks the same as the Big Tech stocks that dominate the normal index—were both below pre-election levels. Meanwhile Treasury yields leapt, on their way to the 4.7% they hit this week.

The big question: Did stocks suffer because bond yields are so high, or merely because they rose very fast in a short space of time? If it is the level of yields that matters, equity markets have a problem. If it is the pace of change, the drop in stocks is merely a matter of indigestion and investors can wait it out.

I think stocks are suffering because of the fundamental message from bonds, not the speed of change. But it is true these are hard to tease apart.

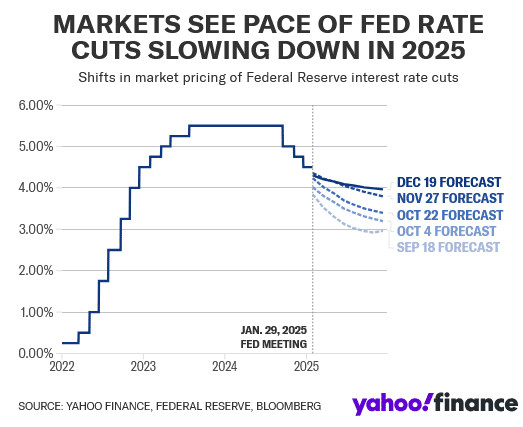

The fundamental message is that we’re close to the limits of growth. Instead of making everyone better off, when the economy runs too hot, it merely generates inflation, and the Federal Reserve has to cool it down with higher interest rates. To be clear, we’re not there yet: Futures traders still price in one Fed cut this year as the most likely outcome. But they think there is only a 16% chance of more than two cuts, while in early December that was seen as more likely than not. More fund managers predict no cuts this year.

Making things worse for stocks, there is also a supply problem. If the Trump Treasury shifts away from Treasury Secretary Janet Yellen’s focus on shorter-term borrowing, more bonds will have to be issued, even if the deficit doesn’t rise. Companies have been borrowing heavily, too, as they refinance maturing pandemic-era debt.

Higher yields caused by stronger growth are usually fine for stocks, because stronger growth means higher profit. But higher yields without more growth just mean pain.

Iain Stealey, international CIO for fixed income at J.P. Morgan Asset Management, said bonds are starting to look attractive both for their yield and their protective qualities in a downturn. That is despite stickier-than-expected inflation and possible inflationary policies from the new administration. But he hasn’t loaded up on bonds yet. Yields might still rise further. “The momentum definitely feels toward higher yields in the near term,” he said.

If yields keep rising, stocks could have a big drop, as they did when yields jumped toward 5% in October 2023. “When does it start to bite?” asked Guy Miller, chief market strategist at Zurich Insurance Group. “I suspect it’s a bit higher than where we are today, maybe another 50bp [half a percentage point] on 10-year yields.”

Investors who, like me, worry about high valuations and investors crowded into hot stocks might want to buy bonds now. Sure, higher near-term yields would bring immediate losses. But as Christian Mueller-Glissmann, head of Goldman Sachs’s asset allocation research, points out, even the price losses from a rise to a 5% yield on a bond bought today would be covered by less than six months of income from the bonds.

Investors who stick to stocks should have their fingers crossed that yields ease off again.

Read the full article HERE.

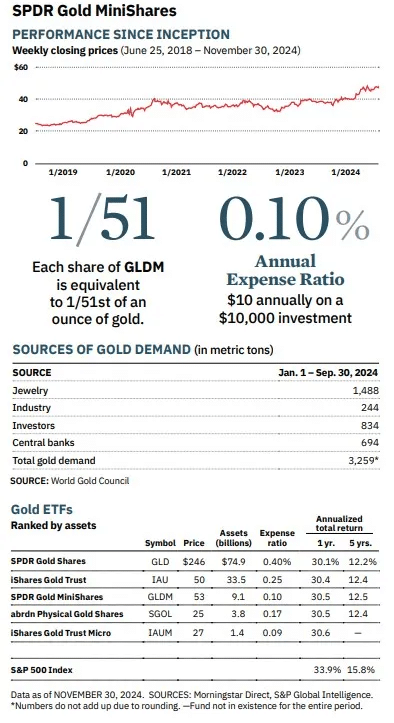

Here are some of the best reasons why you should include at least a little gold in your portfolio.

Costco shoppers have been clearing shelves of the retailer’s one-ounce gold bars. U.S. investors have poured almost $2 billion over the past 12 months into exchange-traded funds (ETFs) that hold gold bullion. And central bankers around the world have been snapping up 67% more gold bricks so far this year than they did as recently as 2021.

There are plenty of reasons investors should include at least a little gold in their portfolios. Although gold prices can be volatile, over the long sweep of history, the precious metal has maintained value.

Giovanni Staunovo, a commodities analyst at UBS Securities, says persistent inflation in the U.S. and wars in Ukraine and the Middle East have been key reasons gold prices have more than doubled in the past decade, to more than $2,600 an ounce.

He expects gold prices to reach $2,900 in 2025 thanks to continuing demand from central banks and interest-rate cuts that are likely to weaken the U.S. dollar, which typically moves inversely to gold prices. For many investors, a 5% allocation to gold strikes the right balance of risk and return, he says.

It may be fun to jingle an ounce of gold in your pocket, but ETFs have other advantages. You don’t have to worry about storage, and you can turn your gold fund into money with the click of a button.

The SPDR Gold MiniShares (GLDM) is one of the largest and fastest-growing gold ETFs. The fund has garnered more than $1 billion in net inflows over the past year, bringing assets to $9.1 billion. With an expense ratio of 0.1%, it is a lower-priced clone of the SPDR Gold Shares (GLD), which has more than $74 billion in assets and charges 0.4% in annual expenses.

The mini fund has slightly higher returns than its larger counterpart thanks to a lower expense ratio, but because it is smaller, it trades a bit less efficiently.

Read the full article HERE.

- Markets are gearing up for a heavy debt issuance this week with a US 10-year and 30-year bond auction.

- Fed interest rate projections see a cut in January out of the cards at the moment, the ECB faces challenges after hot European inflatin numbers.

- Gold price is moving within a pennant technical formation, respecting both upside and downside.

Gold’s price (XAU/USD) is coming alive on Tuesday, sprinting higher alongside with US bonds. Traders are starting to get concerned with two very chunky debt issuances set to take place this week with a 10-year bond and a 30-year bond allocation. Markets remain on edge as well meanwhile over the recent string of comments and headlines about the US tariff plans that President-elect Donald Trump wants to impose.

For a brief moment, there was a sigh of relief on Monday after the Washington Post shared a piece claiming that Trump was considering imposing a simple universal tariff on critical imports. After President-elect Trump quickly pushed back against those headlines, Gold’s price returned to levels where it opened the week.

This Tuesday does not seem any different, with the price of Gold at similar levels. Meanwhile, more risk-bearing assets are surging, with Bitcoin back above $101,000. US yields are also surging, with the 10-year benchmark at 4.62%, nearly a fresh eight-month high.

Daily digest market movers: Bond auctions on the forefront

- Inflation data from several European countries and the overall Eurozone shows that the European disinflation path is being broken up, with monthly gauges tied back up with inflation. This could throw a spanner in the works for the European Central Bank (ECB), which is foreseen to cut its policy rate by 25 basis points on January 30.

- The US 10-year yield rallied to 4.64% last week, a fresh seven-month high and not far off an eight-month high of 4.65%. This Tuesday, it is settling down near 4.62%.

- The CME Fedwatch tool is currently only showing a small 10% chance for a 25 basis points (bps) interest rate cut in January. Further on, expectations are for the Fed to remain data-dependent with uncertainties that could influence the inflation path once President-elect Donald Trump takes office on January 20.

- In the runup to the US Employment report on Friday, the JOLTS Job Openings for November are due at 15:00 GMT on Tuesday. The Institute for Supply Management (ISM) will also issue its December Purchasing Managers Index (PMI)report on the Services sector.

- The US Treasury will allocate a 3-year bond this Tuesday near 18:00 GMT. The very important 10-year bond auction is foreseen for Wednesday around 18:00 GMT.

Technical Analysis: Clawing back

It seems that the Gold price is sitting on the bench for now. Traders look to be very happy where the precious metal is currently trading. The weaker US Dollar (USD), together with the elevated tensions on tariffs and other geopolitical events, is not triggering any refugees into the safe-haven commodity. Should a clearer pattern emerge, expect a catch-up move in Gold prices.

On the downside, the 100-day Simple Moving Average (SMA) at $2,628 is holding again after a false break on Monday. Further down, the ascending trend line of the pennant pattern should provide support around $2,608 as it did in the past three occasions. In case that support line snaps, a quick decline to $2,531 (August 20, 2024, high) could come back into play as support level.

On the upside, the 55-day SMA at $2,656 is the first level to beat. It will not be an easy task as it was already proved twice last week as a firm resistance. In case it breaks through, $2,688 will be the ultimate upside level in the form of the descending trendline in the pennant formation.

In order to focus on what will be important in determining gold prices in 2025, we first need to lay out three important points that help frame New York-based CPM Group’s outlook for gold prices this year.

First, the single most important set of factors in setting the price levels and directions of gold prices are the levels and trends in investment demand for physical gold. That demand in turn is determined by a myriad of economic, financial, and political concerns and uncertainties that cause investors to think they need to own more or less gold.

Investment demand drives prices. Prices drive mine production, secondary recovery from scrap, and fabrication demand.

Second, CPM Group issued a long-term gold buy recommendation in releasing its Gold Survey in November 2000. We laid out the case that there was about to be an upward shift in the investment demand curve: More investors and more types of investors in more parts of the world would want to buy more gold for a longer period of time than ever before.

The result of this gold renaissance would be that gold prices, then around $260 per oz., would rise far beyond the 1980 record $850 and stay there for decades.

Historic trends

Prior to 1980, hostile economic and political trends would cause investors to buy more gold for a year or two. After such a period, conditions would improve and investors would buy less gold. Gold prices would subside until the next one or two-year set of crises would start the cycle again.

In 2000, CPM stated that the next cycle would see investors buying more gold for decades, not years.

Finally, there have been major shifts in the international and national political contexts around the world. One of the more significant ones is the imminent return of Donald Trump as president of the United States.

His return to power this month could dramatically alter the economic and political fortunes and landscape. It is not clear what his presidency will mean and do to the world, given the internal inconsistencies of his stated plans, but they are likely to be negative for world growth. It is too early to tell.

With these underlying realities in mind, the outlook for gold in 2025 suggests further price increases.

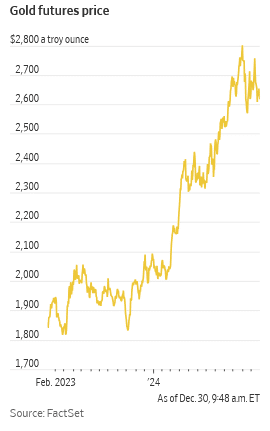

Gold prices have risen sharply since the middle of 2019. In 2024, gold averaged $2,370 per oz. as of Nov. 26, 21% higher than the 2023 average of $1,952.

CPM expects that gold prices might rise further in December, yielding an approximately 23% rise in the annual average gold price for all of 2024. We’re now projecting another 13% increase to an average price around $2,730 per oz. in 2025.

Prices may rise in the first quarter, and calm down a bit in the second quarter of this year, before beginning to rise again, depending on how the economic and political environments evolve.

Recession threats?

CPM has been projecting a recession at some point, perhaps most likely in 2025 or 2026. If the US government slashes its spending and pursues hostile postures toward any number of countries, a recession could arrive sooner and be more severe.

Trump often considers imposing tariffs. This raises the spectre of a deeper recession sooner.

Republican president Herbert Hoover and Congress sought to combat the Great Depression by enacting the Tariff Act of 1930, known as the Smoot–Hawley Act.

It raised tariffs on more than 20,000 imported goods mostly by 40% to 60%. Smoot-Hawley and the retaliatory tariffs in other nations caused a 67% decline in US trade, imports and exports, deepening and prolonging the severity of the Great Depression.

Rising output

Regarding gold market fundamentals, CPM projects around a 1.5% increase in global mine production in 2025 to around 88.6 million ounces. This would follow an increase of around 0.5% in 2024.

Mining share prices are likely to continue to lag gold metal prices, reflecting long-term shifts in investor attitudes and distinctions between gold bullion and mining equities.

Secondary supply, or recycled gold, in 2025 is projected to rise around 10% to about 40.9 million oz. due to the higher gold prices and anticipated worsening consumer economics in many parts of the world.

Total supply of newly refined gold is projected to be around 136.9 million oz., adding in around 7.4 million oz. from transitional economy exports. This would be up around 3.8% in 2025 from 2024.

Banks skittish

Central banks are projected to continue to be net buyers of around 8 million oz. in 2025, roughly unchanged to a bit lower than in 2024. Monetary authorities tend to be more price sensitive than private investors.

Central banks pulled back from buying as much gold as they had been buying since gold prices broke above $2,200 at the end of last March. This hesitancy is expected to continue in 2025, since prices are expected to stay strong and rise further.

One big risk is that a politically and economically collapsing Russia might sell several million ounces of its 75 million oz. of monetary reserves.

Investors bought 24 to 26 million oz. of gold on a net basis annually from 2021 through 2023. They are estimated to have bought around 32 million oz. in 2024. CPM is projecting investors will buy around 44 million oz. in 2025 as political and economic conditions elevate investor concerns.

A range of economic and political issues seem likely to keep investors interested in adding gold to their portfolios. That should keep gold prices high and most likely drive them to new record prices over the course of 2025.

Read full article HERE.

Gold prices inched higher in Asian trading on Friday, on track for a weekly gain as a slight pullback in the dollar provided support, though the greenback remained close to its two-year peak, keeping pressure on bullion.

Spot Gold rose 0.2% to $2,662.94 per ounce, while gold futures expiring in February gained 0.3% to $2,677.70 an ounce by 00:05 ET (05:05 GMT).

Gold set for weekly gain, strong dollar limits gains

The yellow metal was set to gain nearly 2% this week, its best weekly gain since November 17. It had declined in the previous two weeks.

The US Dollar Index fell 0.2% in Asia hours on Friday but remained near a two-year high it hit last month. The US Dollar Index Futures were also lower.

A weaker dollar typically drives gold prices higher because it makes the metal cheaper for buyers using other currencies.

Markets are cautious at the start of 2025, as the U.S. Federal Reserve has signaled only two more interest rate cuts this year.

High interest rates typically pressure gold prices lower, as they increase the opportunity cost of holding non-yielding assets like gold while making interest-bearing investments more attractive.

Other precious saw gains on Friday. Platinum Futures rose 0.5% $929.70 an ounce, while Silver Futures gained 0.4% to $30.30 an ounce.

Copper remains under pressure, markets await fresh China stimulus

Among industrial metals, copper prices were subdued as a strong dollar weighed, while Chinese factory activity data released a day earlier failed to provide support.

Chinese manufacturing activity grew in December but at a slower-than-anticipated pace, data released on Thursday showed.

The data suggests that the impact of recent stimulus measures is waning. Markets are holding out for more clarity on Beijing’s plans for stimulus measures this year.

The People’s Bank of China said it will cut interest rates from the current level of 1.5% “at an appropriate time” in 2025, the Financial Times reported on Friday.

Benchmark Copper Futures on the London Metal Exchange inched 0.2% higher to $8,815.50 a ton, while February Copper Futures were 0.2% lower at $4.0260 a pound.

Read full article HERE

Yellow metal expected to continue to benefit from buying by global central banks

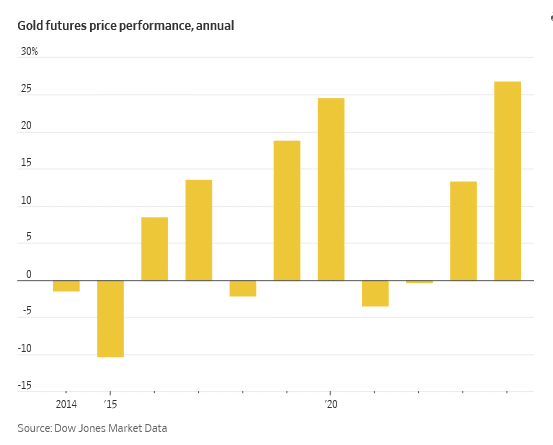

The price of gold is set to rise further in 2025, say Wall Street analysts, although the pace of gains is likely to slow after last year’s bumper 27 per cent rally.

Gold is expected to climb to about $2,795 per troy ounce by the end of the year, according to the average forecast by banks and refiners surveyed by the Financial Times. That is about 7 per cent above current levels.

The yellow metal is expected to continue to benefit from buying by global central banks, which have been diversifying away from the dollar since the US imposed sanctions on Russia following its 2022 full-scale invasion of Ukraine.

Interest rate cuts by the US Federal Reserve, concerns about growing US government debt levels under president-elect Donald Trump and conflicts in the Middle East and Ukraine are also forecast to lift prices. Such factors were behind bullion’s biggest annual gain since 2010 last year.

“We think central bank interest will be a strong base for the buying next year,” said Henrik Marx, global head of trading at Heraeus Precious Metals, which forecast that gold could touch highs of $2,950 per troy ounce this year.

He added that Trump’s second presidential term was also likely to be supportive for gold prices. “Whatever he announces will increase debt, leading to a weaker dollar and increased inflation. That is usually a nice mixture for gold.”

The World Gold Council said in a report that this year’s growth would be “positive but much more modest”.

The most bullish call among those surveyed is from Goldman Sachs, which expects prices to reach $3,000 by the end of 2025. The bank cites central bank demand and expected rate cuts by the Fed.The most bearish forecasts were from Barclays and Macquarie, which both expect gold to sink to about $2,500 per troy ounce by the end of the year — a roughly 4 per cent drop from current levels.

“Our base case into 2025 is for gold to initially face ongoing pressure from US dollar strength, but be supported by improved physical buying and steady official sector demand,” wrote Macquarie analysts in their year-end outlook.

Global central banks bought 694 tonnes of gold during the first nine months of 2024. The People’s Bank of China announced in November that it was resuming gold purchases after a six-month hiatus.

Falling US interest rates have contributed to gold’s rally in the second half of last year, and the pace of further cuts could be crucial to the outlook for the yellow metal. Gold prices pulled back slightly after the Fed lowered rates in December but indicated that borrowing costs will fall more slowly than previously expected in 2025.

Because gold is a non-yielding asset, it typically benefits from lower interest rates, because the opportunity cost of holding it is less.

Trump’s election win in November has provided one of the most favourable scenarios for gold, due to the likelihood of elevated US fiscal spending and increased geopolitical uncertainty, said Michael Haigh, head of commodities research at Société Générale.

“Momentum is taking back over, combined with geopolitical tensions, which is going to add more fuel to the fire,” said Haigh, who expected gold prices to rise to $2,900 per troy ounce at the end of 2025.

Read the full article HERE.

Strategist Jim Paulsen sees lots of economic hurdles ahead

The end of 2024 is nigh, and can’t come soon enough for investors seeing anything but a Santa Rally lately.

Some may blame the Federal Reserve’s rollback of expectations for interest rate cuts, as it worries strong U.S. growth may reignite inflation. Our call of the day from Jim Paulsen, chief investment strategist of The Leuthold Group, sees things differently.

“Although policy officials and investors appear increasingly anxious about the potential for overheated economic growth, I think the more likely outcome for 2025 is an unexpected economic slowdown,” Paulsen says in his Paulsen Perspective blog, where he cautions such a surprise could ultimately lead to a pullback in the stock market of at least 10%.

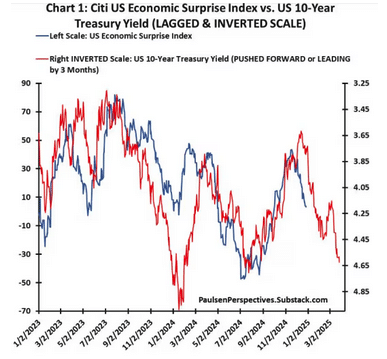

He offers up several examples of weakening growth, such as the Citi Economic Surprise Index—a rise means economic reports have come in stronger than expected, and declines mean economic momentum is trending below expectations. Paulsen’s chart compares that index with the 10-year Treasury yield lagged behind or pushed forward by three months:

Based on history going back to 2003, movements in bond yields have often led to economic surprises, and declining yields have meant an improving economy three months out, and vice versa, he notes. But bond yields, hovering near 4.6%—they hit 4.63% last week—suggest to him the economic surprise index will slow to -35 in the first quarter, slowing GDP as well.

While Paulsen says healthy business and household sectors will likely keep a recession at bay next year, if real GDP slows from a current 2.7% pace to 2% or less, recession fears will dominate financial discussions, drive down profit forecasts and feed through to stocks.

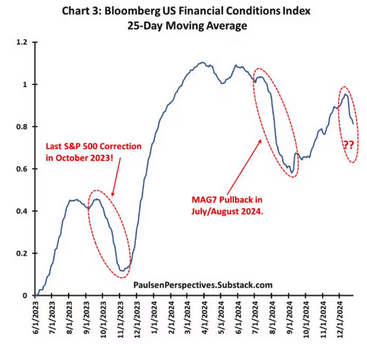

He also looked at the U.S. Financial Conditions Index, which has been worsening since early December. “As illustrated, two other times during the last 18 months, even modest declines in this index led to significant stock market events,” he said, pointing to stock pullbacks of October 2023 and last summer’s rare “Magnificent 7” slump.

“The most recent decline in financial conditions is not yet nearly as pronounced as the last two but it wouldn’t be surprising if financial conditions continue worsening somewhat as economic growth slows further in the new year,” he said.

Paulsen rattled off a number of concerning issues where stocks are concerned, such as deteriorating breadth, where the number of U.S.-listed stocks climbing relative to the number falling has dropping since early October. His read from that is investors are increasingly cautious, noting also underperformance by cyclical and more aggressive stocks since mid-November.

“Since most currently believe the economy is healthy, if not too strong, any meaningful slowdown will come as a surprise. And a ‘surprising slowdown’ which heightens fears could pause the stock market run if not possibly produce a 10% to 15% correction,” cautions Paulsen.

But given corrections are tough to call, he says “most should stay invested since the bull market seems likely to continue during 2025 even if it experiences a bump or two along the way.” That said, a small shift away from cyclical and other “traditionally aggressive investments” toward more defensive ones, may make sense, he says.

The likelihood of a correction and how deep it goes depends much on how technology sector favorites perform in 2025, says Paulsen. If that strength continues, a correction can be avoided, with any slowdown for those stocks a risk. In the below chart he overlays the relative performance of the S&P 500 tech sector with the U.S. financial conditions index:

The last four years have seen obvious close correlation, and in the past a worsening of financial conditions has led to tech underperformance that infects the entire market, Paulsen notes. “So, the primary question for investors in 2025 may be how much will financial conditions deteriorate as the economy slows next year, and how much will this impact technology stocks?”

Read the full article HERE.

Big banks are forecasting prices rising to $3,000 in year ahead

Few investments did better in 2024 than gold, which is wrapping up its best year since 2010 and one of its largest annual gains on record. Wall Street’s gold bugs think prices will climb even higher in 2025.

Prices for the precious metal are up 27% in 2024 to $2,617.20 a troy ounce. That is better than the S&P 500’s 25% gain and not far behind the 31% increase of the technology-stock-laden Nasdaq Composite Index.

Gold futures hit a record ahead of the U.S. presidential election but have declined since then. That was expected, though, as investors who had been nervous about the election’s outcome moved money from the haven and back into riskier assets.

Analysts at JPMorgan, Goldman Sachs and Citigroup share a price target of $3,000. Here are some of their reasons:

Lower interest rates

The extent to which the Federal Reserve cuts interest rates remains to be determined, but investors expect further reductions in 2025. The lower rates get, the lower the opportunity cost of owning gold, which pays no interest or dividends.

Analysts expect some portion of the $6.7 trillion held in money-market funds to find its way into exchange-traded funds that hold gold, such as SPDR Gold Shares, as investors become disenchanted with declining yields. “This is the most bullish part of the cycle for gold,” said Greg Shearer, head of base- and precious-metals strategy at JPMorgan.

Geopolitical uncertainty

Investors large and small tend to flock to gold in times of heightened conflict. And there is plenty of that headed into 2025, from wars in the Middle East and Ukraine to President-elect Donald Trump’s vows to escalate trade disputes with China and other countries. The prospect that inflation will flare up again also has investors on edge.

Investors in China have been especially enthusiastic about buying gold lately, given the country’s slumping economy and stocks, as well as Trump’s threats to levy tariffs on its exports to the U.S.

Central-bank buying

Central banks around the world, especially in countries that have strained relationships with the West, have been gobbling up gold. China, in particular, is a powerful source of demand, with official gold reserves more than tripling since 2008, according to Goldman Sachs.

Western sanctions on Russia after it started its full-scale invasion of Ukraine in 2022 prompted some central banks to move away from dollar-based assets. Instead, they are keeping more of their reserves at hand and in an asset, gold, that is beyond the reach of foreigners.

The Russia sanctions, Goldman analysts said, “marked a clear turning point, leading many emerging-market central banks to rethink what is risk-free.”

In a 2024 poll of central bankers, 29% said they intended to increase their gold reserves in the subsequent 12 months, according to the World Gold Council, the most since it started the survey in 2018.

Little industrial demand

Another thing gold has going for it is there are few uses beyond as a store of wealth. There is jewelry, of course. But jewelry isn’t just about demand. It becomes an important source of supply when gold prices rise and people have more incentive to sell grandma’s old jewelry to scrappers.

“Gold doesn’t have the industrial baggage of other commodities that could really get pulled down under this sort of trade-disruption hit,” JPMorgan’s Shearer said.

That means a slowdown in economic activity, such as what would be expected in a trade war with China, doesn’t really hit gold demand the way it would other precious metals with industrial uses, such as silver and platinum.

Momentum

Gold rallies tend to be long-lasting. In five of the past six years that gold futures have risen by at least 20%, prices rose again the following year. And in those five years, the average increase was more than 15%, according to Citi analysts.

The only year in which gold followed a 20% or better gain with a down year was in 2021, when prices fell 3.6% after gaining about 25% in 2020.

Write to Ryan Dezember at ryan.dezember@wsj.com

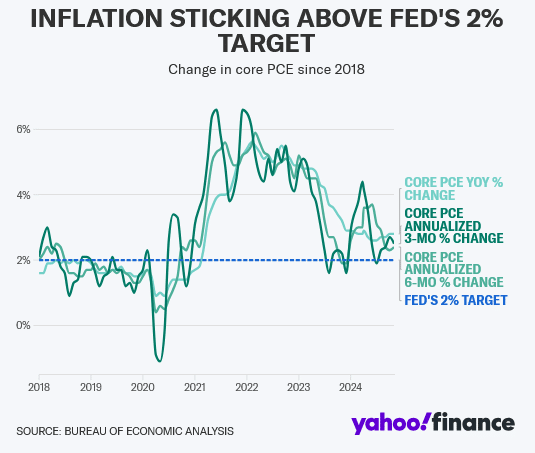

Inflation has been one of the top concerns for the US economy in 2024. And it looks like fears over sticky prices will continue in 2025.

“We expect a gradual deceleration from where we are, but to levels that are still uncomfortably high for the Fed,” Deutsche Bank chief economist Matthew Luzzetti told Yahoo Finance in an interview.

So far this year, inflation has moderated but remains stubbornly above the Federal Reserve’s 2% target on an annual basis, pressured by hotter-than-expected readings on monthly “core” price increases, which strip out volatile food and energy costs.

In November, the core Personal Consumption Expenditures (PCE) index and the core Consumer Price Index (CPI), both closely tracked by the central bank, rose 2.8% and 3.3%, respectively, over the prior-year period.

“Inflation is primarily going to be driven by the services side of the economy,” Luzzetti said, calling out core services like healthcare, insurance, and even airfares. “Shelter inflation is also still high, and although it’ll come down over the next year, it’s likely that it could remain somewhat elevated.”

According to updated economic forecasts from the Fed’s Summary of Economic Projections (SEP), the central bank sees core inflation hitting 2.5% next year, higher than its previous projection of 2.2%, before cooling to 2.2% in 2026 and 2.0% in 2027.

This largely aligns with Wall Street’s current projections. Out of the 58 economists surveyed by Bloomberg, the majority see core PCE moderating to 2.5% in 2025 but they do expect less of a deceleration in 2026, with the bulk of economists anticipating a higher 2.4% reading compared to the Fed.

“The risks are certainly tilted in the direction of higher inflation,” Nancy Vanden Houten, lead US economist at Oxford Economics, told Yahoo Finance. “A lot of the risk comes from the possibility of certain policies being implemented under the Trump administration on tariffs and on immigration.”

President-elect Donald Trump’s proposed policies, such as high tariffs on imported goods, tax cuts for corporations, and curbs on immigration, are considered potentially inflationary by economists.

Those policies could further complicate the Federal Reserve’s path forward for interest rates.

In a press conference following the Federal Reserve’s last interest rate decision of the year, Federal Reserve Chair Jerome Powell said the central bank expects “significant policy changes” but cautioned that the extent of policy adjustments remains uncertain.

“We need to see what they are and what effects they have,” he told reporters at the time, adding the Fed is “thinking about these questions” and will have “a much clearer picture” once policies are implemented.

Trump 2.0 and the ‘inflationary spiral’

For some, the picture is already clearer than not.

Nobel Prize-winning economist and Columbia University professor Joseph Stiglitz said at Yahoo Finance’s annual Invest conference last month that the US economy has achieved a soft landing, in which prices stabilize and unemployment remains low. “But that ends Jan. 20,” he warned, referring to Inauguration Day.

Tariffs have been one of the most talked-about promises of Trump’s campaign. The president-elect has pledged to impose blanket tariffs of at least 10% on all trading partners, including a 60% tariff on Chinese imports.

“It will be inflationary,” Stiglitz said. “And then you start thinking of the inflationary spiral, the prices go up. Workers will want more wages. And then you start thinking of what happens if others retaliate [with their own duties].”

Stiglitz believes Powell will raise interest rates if inflation pressures persist.

“You combine the higher interest rates and the retaliation from other countries, you’re going to get a global slowdown,” he said. “Then you have the worst of all possible worlds: inflation and stagnation, or slow growth.”

BNP Paribas issued a grim 2025 outlook, expecting the Fed to pause its easing cycle next year amid a “substantial rise in inflation from late 2025 into 2026” due to the rollout of tariffs. The firm sees CPI settling at 2.9% by the end of next year before climbing to 3.9% by the end of 2026.

Meanwhile, Minneapolis Fed president Neel Kashkari categorized a possible retaliation by other countries as a “tit-for-tat” trade war, which would keep inflation elevated over the long term.

Investors are starting to take notice of the risk. In the latest Global Fund Manager Survey from Bank of America released earlier this month, expectations of a “no landing” scenario, in which the economy continues to grow but inflation pressures persist, hit an eight-month high.

Headwinds and tailwinds

In the United States, Congress typically sets tariffs, but the president has the authority to impose certain ones under special circumstances, and Trump has vowed to do so.

It remains unclear which policies will be a priority once Trump takes office or if he’ll fully commit to the promises he’s already made.

“Our baseline is that we do get tariffs next year, but they start relatively low and targeted,” Luzzetti said, projecting a 20% cumulative rise in tariffs on China, in addition to more targeted levies on Europe.

“Things like the universal baseline tariff, which is this across-the-board tariff rate that Trump has threatened, we don’t think that that gets implemented,” he said.

Still, the economist believes that whatever tariffs Trump does choose to implement will lead to higher inflation over time. He’s baked in zero interest rate cuts from the Federal Reserve next year for that reason.

“Our view is that inflation does not come below 2.5% next year and that the Fed would not be comfortable with that, and therefore would not keep cutting rates,” he said. “But also we have an expectation that the economy will remain quite resilient.”

And the US economy has been resilient throughout the course of 2024. Retail sales once again topped estimates for the month of November, GDP remains strong and above trend, the unemployment rate continues to hover at around 4%, and despite future uncertainty and its bumpy path down to 2%, inflation has moderated.

“There’s just a good amount of tailwinds to an economy that is already receiving solid growth momentum, and the Fed has just undertaken 100 basis points of rate cuts this year,” Luzzetti said. “All that, we think, sets a pretty solid floor under growth over the next year.”

Read full article HERE.

US and European companies are frontloading orders and weighing price hikes while Chinese factories hunt for buyers elsewhere

A two-hour drive west of Shanghai, Sunny Hu has spent almost two months since the US election rushing shipments of her company’s outdoor furniture and pavilions to American customers and racing to diversify Hangzhou Skytech Outdoor Co. Ltd. into other markets.

Meanwhile, in the heart of Germany’s Riesling belt, eighth-generation winemaker Matthias Arnold has been fielding an influx of special orders from US importers since Donald Trump’s victory. He’s rushing to fill as many as possible before the president-elect can bring back levies on European wines that he imposed in 2019 but the Biden administration suspended.

Across the world, businesses aren’t waiting until US Inauguration Day on Jan. 20 to see which countries, products or tariff rates are announced in Trump’s widely telegraphed trade wars. The mere threat of his universal tariffs is sparking a scramble that’s leaving the global trading system prone to bottlenecks, saddled with higher costs and vulnerable to disruptions should an economic shock come along.

“We’re still in the freakout period,” said Robert Krieger, president of Los Angeles-based customs brokerage and logistics advisory firm Krieger Worldwide. “There’s about to be a king tide in the supply chain.”

At California-based JLab, Chief Executive Officer Win Cramer had already shifted his supply chains away from China to dodge tariffs imposed during Trump’s first presidency. Along with a hiring freeze imposed until June amid the uncertainty, his next move would be raising prices for the company’s headphones and wireless products if a universal tariff is applied this time around.

To get ahead of the game, some firms are frontloading orders. Others are seeking new suppliers or, if that’s not possible, renegotiating terms with existing ones. A common theme: The renewed stress comes with higher costs, in the form of bigger inventories, costlier expedited shipping, or taking a chance on untested partners. Profits will suffer and expenses will be reduced elsewhere, they said. Ultimately consumers will foot the bill.

The problem is, for all the preemptive moves, there’s no guarantee that the strategies that helped some businesses endure Trump’s first trade war will work this time around. As shown by Trump’s late November threat to impose additional 10% tariffs on goods from China and 25% tariffs on all products from Mexico and Canada, both allies and adversaries are in his sights this time around.

Zipfox, an online product-sourcing platform that links US-based businesses with factories primarily in Mexico, has seen a 30% uptick in quote requests and new buyer signups since two weeks before the election, according to founder and CEO Raine Mahdi, who said inquiries spiked again after Trump threatened 100% tariffs on BRICS nations. Most of those are from importers of goods manufactured in China. Mahdi warns against complacency.

“If you wait too long, you’re going to find yourself trying to make the transition in a pinch,” Mahdi said. “This time you’re not catching the tail end of the Trump administration, you’re catching the entire thing and with a new wrath.”

The survival instincts of business leaders are already beginning to show up in high-frequency data, and central bankers are keeping a close eye given the threat that higher import taxes pose to their inflation fights.

China’s ports saw double-digit growth in container throughput in the two weeks around the election and that rose further to an almost 30% gain in the second week of December. International air freight flights have increased by at least a third each week since mid-October and economists expect that’ll continue as customers rush to frontload orders.

Across the Pacific, the busiest container gateway in the US, made up of the twin ports of Los Angeles and Long Beach, is seeing a surge of inbound shipments — not unlike the wave that accompanied Trump’s first tariff volleys at China. Both ports smashed pandemic-era records in the third quarter and volumes are expected to stay elevated into next year.

The advanced ordering started well before the US election in early November and is showing up at the docks now. At the Port of LA alone, inbound container shipments in November jumped 19% from the same period a year earlier, and 2024 is on track to be Long Beach’s busiest year ever. But the cargo crush through Southern California is unlikely to last for long and probably means a slump at some later stage.

“The surge in imports nationwide could continue into the spring of 2025,” Port of Long Beach CEO Mario Cordero told reporters in December. “Back in 2018, tariffs initiated during the first Trump administration resulted in a 20% decrease in imports from China and a 45% decrease in exports to China due to retaliatory actions.”

Tariffs aren’t the only factor at play given the typical rush ahead of China’s annual Lunar New Year holiday, which starts in late January, and the need to get ahead of potential port strikes in the US. Given that backdrop, it wouldn’t take a lot to stoke additional pressure in the global trading system, said Citigroup Inc. senior global economist Robert Sockin.

“Shipping costs may feel additional upward pressure if front-running activity picks up notably,” he said. “If front-running is particularly extensive, it could create some bottlenecks at US ports which would exacerbate supply chain pressures.” Prospects for another dockworkers’ strike just days before Trump’s inauguration only compound those concerns.

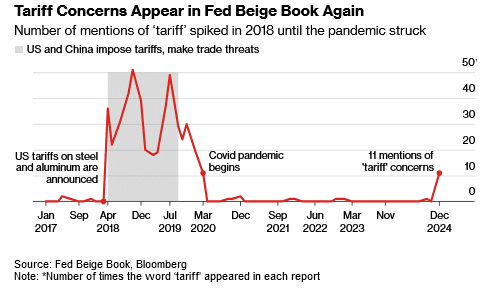

Since the US election in early November, the Federal Reserve has heard more concerns about the levies. The word “tariff” appeared 11 times — — the most since 2020 — in its latest Beige Book report, a regional survey of businesses.

An analysis of earnings-call transcripts to count mentions of tariffs by executives of S&P 500 companies jumped in November to the highest in records going back to late 2019, according to data compiled by Bloomberg. Industrial firms and in particular industrial machinery and suppliers are talking about tariffs the most.

Smaller companies are doing more than talking, though it’s too soon to measure with any precision the extent of the economic fallout.

If Lynlee Brown’s email inbox is any guide, the impact will be widespread. She’s a global trade partner at EY, the consulting giant. In the early morning hours after the US election, she had received more than 400 messages. The queries spanned the globe — from US companies that import raw materials to an Australian apparel company. “There are a lot of questions coming in from companies,” she said.

Among those looking for answers are Kim Osgood and Mike Roach, who own Paloma Clothing, a women’s clothing store in Portland, Oregon. The shop offers products that include jewelry, accessories, sweaters, scarves and rain coats. The store has already begun placing extra orders from its vendors who manufacture overseas.

“The one thing as a business owner that you absolutely abhor is uncertainty,” Roach says. “But there’s not a lot we can do.”

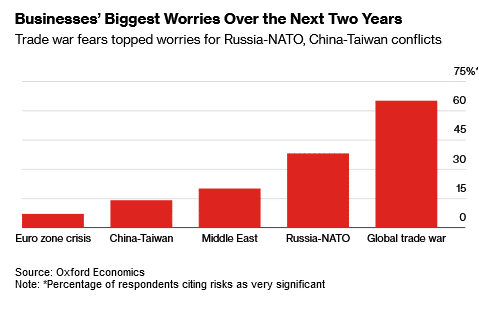

Such paralysis appears to stem from fear. According to an Oxford Economics survey of 156 businesses in the two weeks to Dec. 10, 65% of respondents said a global trade war presents a very significant risk to the global economy over the next two years, compared with 38% for a Russia-NATO showdown and 14% for a China-Taiwan conflict.

Across China’s vast manufacturing hubs, businesses are trying to maintain export sales. In Hangzhou, about 90% of Hangzhou Skytech Outdoor’s products are exported to the US, making it vulnerable to tariffs in excess of the 25% already slapped on its American exports during the first trade war in 2018-19.

The firm is considering offering its US buyers a price that incorporates both tariffs and freight, but those would need to be at least 10% to 15% higher, Hu said, depending on the new tariff level. In the meantime, the company is aiming to ship half of 2025’s expected demand before Trump is sworn in.

About three weeks after the election, when Bloomberg News reporters visited, the workshop and warehouse were piled high with boxes on pallets ready to ship as workers hurried to bend and cut metal to meet the peak demand season. After a boom in sales during the pandemic the firm decided to expand — it’s currently building a new five-story workshop and showroom which would double capacity.

Crossing the muddy construction site, Sunny’s husband, the CEO of the company, looked at the almost-finished building and noted all the uncertainty the company faces.

The unknowns are equally vexing at Carlsbad, California-based JLab. Its products were hit by tariffs in 2019 during the first Trump administration after requests for exclusions from the duties were denied. That prompted Cramer to move about 90% of his contract manufacturing from China to Vietnam, Malaysia and other countries. “We were essentially forced to rebuild our supply chain outside of China, and that’s not an easy thing to do,” he said.

Cramer said trying to build up inventories before tariffs are imposed isn’t really practical because that takes cash and with ever-changing technology, he could be stuck with obsolete inventory. And Trump might do something other than what he said he would during the campaign.

While the company didn’t raise prices after tariffs were enacted in the first Trump administration, that may not be possible this time. His top-selling product is a $24.95 wireless ear bud, and while he can absorb some additional cost from the tariff, he’ll have no choice but to pass on some of it because of his low profit margins.

“We’re designed to offer a fair product at a fair price, and when tariffs come into play, that makes it harder to do,” he said.

Many businesses that adjusted to Trump’s first round of tariffs would struggle to deal with a second blow, according to Evelyn Suarez, a customs attorney based in Washington whose clients include US manufacturing companies that import parts and components from China. “They’re at the level they could manage, but if you add on another 60% — that would be prohibitive.”

Suarez said her clients are “bracing for higher costs and that’s a real challenge because prices are going to go up.”

Arnold, with winemaker Weingut Jul. Ferd. Kimich, had to absorb about 80% of Trump’s tariffs during his first presidency to keep customers who could otherwise pivot to less expensive wines from other regions. Both Arnold and the US importer he works with want to maintain relatively steady prices for customers this time around too; the question is how the additional cost of the tariffs will be split between them.

Arnold, who exports about 10,000 bottles of wine to the US each year amounting to about 5% of his overall volume, said he’s confident he can wait out another round of tariffs, though higher-margin markets like Scandinavia start to become more attractive export destinations if the tariffs are in place longer term. Some German winemakers, however, sell as much as 40% of their product to the US. For them it will be tough, he said.

“This time the tariffs could come fast and last much longer,” Arnold worries.

Read the full article HERE.