Rare GOP advantage takes pressure off Trump to win over independent voters

Beneath the headline results in many polls, something unusual has turned up with big implications for politics: More voters are calling themselves Republicans than Democrats, suggesting that the GOP has its first durable lead in party identification in more than three decades.

The development gives former President Donald Trump an important structural advantage in the November election. But other factors could prove more important to the outcome. Democratic Vice President Kamala Harris still leads narrowly in many polls, in some cases because she does well with independent voters.

Bill McInturff, a GOP pollster who works on NBC News surveys, first noticed in May that more voters were calling themselves Republicans. “Wow, the biggest deal in polling is when lines cross, and for the first time in decades, Republicans now have the national edge on party ID,” he wrote. He called the development “the underrecognized game-changer for 2024.”

In combined NBC polls this year, Republicans lead by 2 percentage points over Democrats, 42% to 40%, when voters were asked which party they identified with. That compares with Democratic leads of 6 points in 2020, 7 points in 2016 and 9 points in 2012.

“Republicans being 5 to 9 points down on party identification—that is like running uphill,” McInturff said. “We don’t know the election’s outcome, but we know Republicans have a better shot at doing well if party ID is functionally tied, with perhaps the smallest tilt toward Republicans.”

Gallup also found more voters identifying as Republican than Democratic, by 3 points in its July-to-September surveys. It was the first time that the GOP had an advantage in the third quarter before a presidential election in Gallup surveys dating to 1992.

Pew Research Center found the GOP with a 1-point lead this spring in an extensive, 5,600-person poll it conducted to create benchmarks for its other surveys. As with Gallup and NBC polls, each party’s share of voters included people who call themselves independents but also say they consistently lean toward one party.

The last time that presidential Election Day exit polls found Republicans on a level playing field with Democrats in party identification was in 2004, when the two were tied. That was also the only year in about three decades that Republicans won the national popular vote.

“It’s definitely unusual,” Jeffrey Jones, senior editor of Gallup polling, said of the GOP advantage. Gallup said party affiliation is one of several foundational factors favoring the GOP this year, along with its finding that Republicans are trusted more to handle the economy and immigration, which voters see as the nation’s most challenging problems.

Not all polls find the same tilt toward the GOP, and a lead in party affiliation isn’t a guarantee of success. In the 2022 midterm elections, Republicans turned out more voters than Democrats did in Pennsylvania, Arizona and Michigan, according to the AP VoteCast survey of the electorate. But independent voters favored Democrats so heavily that the party won the governor’s races in all three states, as well as Senate races in Pennsylvania and Arizona. Democrats also benefited from an erosion of support among Republican voters for many GOP candidates who aligned themselves closely with Trump.

More recently, NBC’s September poll found Republicans with a 1-point advantage on party identification, and yet Harris led Trump by 5 points. Her lead rested on an advantage among independent voters and that she was winning more than 20% support among Republicans who don’t consider themselves part of Trump’s “Make America Great Again” movement, a group that ultimately could shift back to Trump.

Similarly, a New York Times/Siena survey released this week found Republicans outnumbering Democrats among likely voters by 1 percentage point, but Harris leading Trump by 3 percentage points. Defections from Trump among some GOP voters was one reason for her lead.

Patrick Ruffini, a Republican pollster, said the GOP advantage in party identification lessens the pressure on Trump to win over independent or swing voters, “but it does not say that Trump is going to win” this year.

“It’s a loose indicator that you have a number of people who are disappointed in the Democratic Party’s performance,” Ruffini said. “It should be a good indicator for Trump. But as we saw in 2022, it doesn’t mean the candidates who are running are going to maximize their advantage.”

Jones said party identification tends to rise and fall in tandem with views of the president. In combining all its surveys in a given year, Gallup has found the GOP leading in party identification only three times since 1991. That was in 1991, after President George H.W. Bush led allies in the first Gulf War, and in 2022 and 2023, as President Biden’s job approval ratings sank.

The GOP has held a short-term edge on occasion, such as after the Sept. 11, 2001, terrorist attacks, when voters rallied behind President George W. Bush. But the advantage soon faded.

Party identification in polling gives a snapshot of voters’ current thinking about the two parties, and it can be a different picture than the one drawn by voter-registration data. Many analysts said more voters nationwide are registered as Democrats than as Republicans, though the numbers include some estimates because many states don’t record a party affiliation when people register to vote.

L2, a nonpartisan company that collects and updates the voter lists from each state, said more than 38% of U.S. voters are Democrats and 32% are Republicans, based on state records and its modeled calculation of voter preferences in states that don’t register voters by party.

Election results show that some of those Democrats have been voting Republican for years in states such as Pennsylvania, and that some with GOP registration back Democrats. They just haven’t updated their voter-registration records.

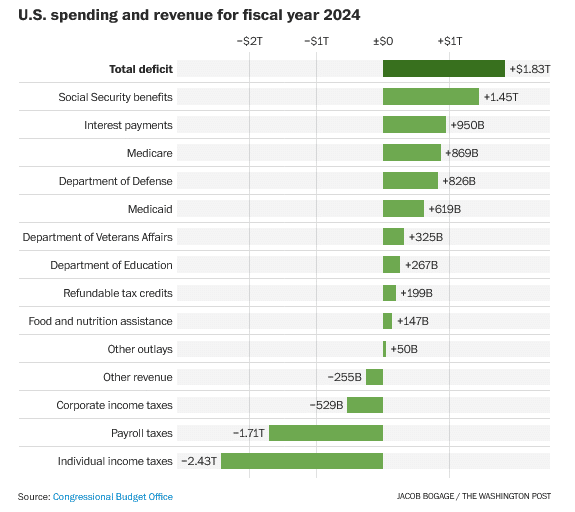

Interest payments on the existing national debt cost more than the Pentagon’s budget in the last fiscal year, the Congressional Budget Office reported.

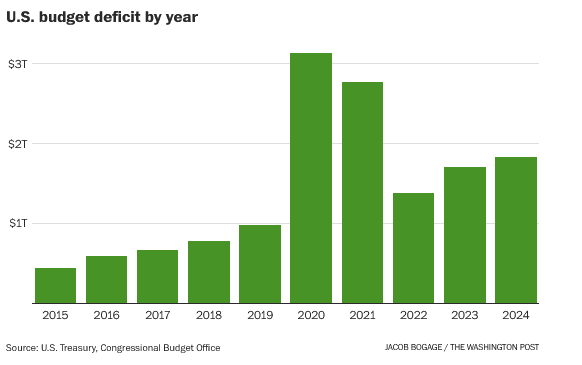

The federal budget deficit swelled to $1.8 trillion in the fiscal year that ended in September, an enormous sum that significantly increases the national debt as Washington barrels toward a potential 2025 showdown over spending and taxes.

The Congressional Budget Office warned in a Tuesday report that interest payments on the debt reached $950 billion, larger than the Pentagon budget.

The next president is likely to face key decisions, along with Congress, about whether and how to tackle the debt and skyrocketing interest costs. Neither former president Donald Trump nor Vice President Kamala Harris has made deficit reduction a key plank of their campaigns for the White House.

As of Friday, the United States had accumulated a public debt of $35.7 trillion. The CBO projected in June that the debt would exceed $50 trillion by the end of this decade. The nation’s debt compared with the size of the overall economy, a key metric of fiscal stability, is projected to exceed its all-time high of 106 percent by 2027.

“A [nearly] $2 trillion deficit is bad news during a recession and war, but completely unprecedented during peace and prosperity,” said Brian Riedl, a senior fellow at the conservative-leaning Manhattan Institute. “The danger is the deficit will only get bigger over the next decade due to retiring baby boomers and interest on the debt.”

While the debt receded as a political issue as the nation spent big to combat the coronavirus pandemic, that is likely to change in the coming year, when major portions of Trump’s 2017 tax cut law expire. Without new legislation, millions of Americans would see a sharp tax increase. But extending the cuts is likely to necessitate massive new borrowing.

Meanwhile, Social Security and Medicare are projected to run out of money in 2035 and 2036, respectively, forcing sharp reductions in benefits without action from lawmakers. And rising interest rates on the debt risk crowding out spending on other vital needs.

Trump has proposed programs or tax policies that could increase the debt by as much as $15.2 trillion or as little as $1.45 trillion through 2035, according to a nonpartisan estimate released Monday by the Committee for a Responsible Federal Budget (CRFB), a top Washington fiscal watchdog.

He’s proposed massive tariffs on imports that could raise as much as $4.3 trillion over 10 years but would also probably spike consumer inflation and depress economic growth, according to even some of his own economic advisers.

Stephen Moore, an economist at the conservative Heritage Foundation and a Trump economic counselor, has said the former president prioritizes economic growth over spending cuts, reasoning that a growing economy would produce enough tax revenue to outpace inflation.

Trump’s campaign did not respond to a request for comment. Earlier this week, Trump senior adviser Brian Hughes said in a statement that the former president’s plan to control the deficit would “rein in wasteful spending, defeat inflation, reduce the burden of interest costs, and ignite economic growth that fuels federal revenue, so we can make our economy great again.”

But Trump’s plans, and his campaign’s focus on gross domestic product growth, are far from enough to reduce annual deficits, even if the U.S. economy expands well beyond most forecasts.

“You cannot grow your way out of this problem,” said Doug Holtz-Eakin, president of the right-leaning American Action Forum and a former CBO director. “They are arithmetically in the wrong place.”

Harris’s proposals, the CRFB projected, could carry a maximum price tag of $8.1 trillion, or they could be fully paid for with new revenue from targeted tax increases on the wealthiest earners and major corporations, and higher tax rates on capital income.

Harris has pledged to extend the 2017 tax cuts for those making less than $400,000 a year and said earners in the top tax bracket would pay a 39.6 percent rate. But she has not proposed specific new tax rates for filers in between those ranges, making it difficult to assess the budgetary impact of that policy.

A Harris campaign spokesperson said in a statement that Harris as president would commit to reducing the deficit in her budgets.

“One of the things that I’m going to make sure is that the richest among us, who can afford it, pay their fair share in taxes,” Harris said in a “60 Minutes” interview broadcast Monday, when asked about paying for her proposals. “It is not right that teachers and nurses and firefighters are paying a higher tax rate than billionaires and the biggest corporations. And I plan on making that fair.”

A White House spokesman said Republican tax plans would worsen the fiscal crunch.

“While the deficit is lower than it was last year, President Biden believes we need to reduce the deficit further by making the wealthy and large corporations pay their fair share, and by reducing wasteful spending on special interests like Big Pharma,” spokesman Jeremy Edwards said.

Many Democrats say tax cuts — dating to legislation under President George W. Bush in 2001 — have taken too big a bite out of federal revenue, especially in recent years. And the memory of past congressional fiscal battles is haunting some liberal lawmakers. Sen. Elizabeth Warren (D-Mass.) this spring warned Democrats against taking “the coward’s way out” by not raising taxes enough on the wealthy and corporations in the coming tax debate.

“Over the last two decades, we are dealing with the ramifications of about $10 trillion of missing revenue. We’ve had four rounds of massive tax cuts, mostly skewed to the wealthy, none of which were paid for,” Rep. Brendan Boyle (Pa.), the top Democrat on the House Budget Committee, told The Washington Post. “As we get ready for the big once-in-a-decade fight that’s going to happen in 2025 over what tax policy will look like for the next eight to 10 years, we need to be serious about ensuring that we have the proper revenues in order to pay for the size of government we want and the American people expect.”

But the tenor of the presidential campaign has set many budget watchdogs on edge, as both candidates put forward ever-larger spending proposals and embrace extending at least some of the 2017 tax cuts.

After Trump’s running mate, Sen. JD Vance (Ohio), proposed a $5,000 child tax credit — a policy Trump himself has not endorsed — Harris countered with a $6,000 tax credit proposal for parents with newborns. Both candidates have embraced ending taxes on tips: Trump would exempt tipped wages from all taxes; Harris would exempt them only from income taxes and has discussed other policy guardrails.

“It’s a patchwork of targeted fiscal bribes, and it in no way adds up to an overall economic vision, which is really needed at a moment when our economy is changing dramatically,” CRFB President Maya MacGuineas said.

A larger debt burden — fueled by growing annual deficits — could prevent lawmakers from appropriately responding to those changes, experts and policymakers worry.

As the United States is forced to spend more money paying back its lenders, it has less to fund new investments and vital services.

“Debt service is nonnegotiable, so you’ve got to pay that, and you can’t use those funds for any other budgetary priorities,” Holtz-Eakin said.

Precious metals hold a unique place in the investment universe. Gold, silver, platinum and palladium combine aspects of financial instruments with characteristics of raw materials used in manufacturing.

Investors often hold relatively small amounts of precious metals when they’re worried about currency devaluation amid government spending or high inflation during economic boom times. Precious metals, especially gold, also have an allure as a place to park cash during times of heightened global economic or political worries.

“The timeless element of precious metals has led investors to perceive them as safe havens, inflation hedges and wealth diversifiers,” said Rohan Reddy, director of research with investment management firm Global X. “Historically, this has made them useful hedging instruments during market downturns as well as times of geopolitical uncertainty.”

Understanding investing in precious metals

The first thing to understand about precious metals is that they’re not all created equal.

While these metals can serve as portfolio diversifiers or hedges against inflation or weakness in the US dollar, they all have different demand dynamics.

“Investors should seek to understand the driving factors behind each precious metal, as each can behave differently under a variety of circumstances,” Reddy said.

Types of precious metals

The main precious metals for the investment community are gold, silver, platinum and palladium.

1. Gold

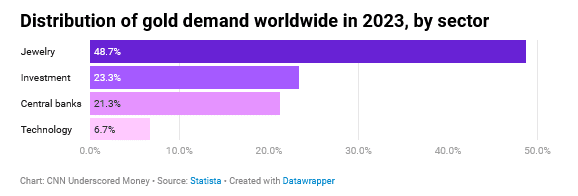

Of the four main precious metals, gold is the most popular for pure investment considerations, but the biggest source of its demand is for the jewelry market, especially in India and China.

“Gold is the preferred hedge against geopolitical tensions around the world, inflation and economic uncertainty,” said Alex Ebkarian, chief operating officer of physical precious metals dealer Allegiance Gold. “While it has periods of volatility, it has clearly proven to be a great long-term investment and will continue to be so for the foreseeable future. Overall, gold tends to carry less risk than the other three metals.”

That’s in part due to gold having a much larger market than silver, platinum or palladium, meaning investment in the “yellow metal” may be more liquid — easier to buy and sell — than metals with smaller markets.

2. Silver

Silver is often called “the poor man’s gold” because it is much cheaper than the yellow metal and often moves along with gold based on similar investment considerations.

But silver has long been more widely used as an industrial metal in electronics, automobiles and appliances, and the demand outlook amid the energy transition is bright because of its heavy use in solar panels.

That industrial demand also makes silver a hedge against inflation. When the economy is gaining ground, or expected to, silver prices might rise, giving investors a cushion against rising consumer prices for goods and services.

3. Platinum

Platinum is rarer than gold and has a smaller market, and the limited supply makes the metal subject to volatile price swings, Reddy said. With most global platinum coming from South Africa, problems in the mining industry there — such as struggles with electricity — can exacerbate the volatility.

Demand for platinum is largely dominated by jewelers and industrial buyers, especially the auto industry, which uses the metal in catalytic converters.

4. Palladium

Palladium is also a key ingredient for catalytic converters, making demand for it highly influenced by the automotive sector.

Due to its rarity, palladium is often extracted along with other metals, which can make it difficult to get pure-play palladium exposure from mining companies, Reddy said.

Benefits and drawbacks of investing in precious metals

Volatility

Like other commodities, precious metals prices are often volatile.

Diversification

But George Cheveley, metals and mining specialist with investment manager Ninety One, pointed out that precious metals also often perform well when equities are falling, providing portfolio diversification.

Robert Johnson, a finance professor at Creighton University, agreed that precious metals are good portfolio diversifiers. He studied the relationship between precious metals, equities and fixed-income investments for a book he co-authored called “Invest with the Fed: Maximizing Portfolio Performance by Following Federal Reserve Policy.”

“What we found is that the correlation between the returns to precious metals and stock and bond indices was near zero,” Johnson said. “So, while the returns to precious metals historically have been lower than those of stock market indices, the low correlation between stocks and precious metals makes them ideal diversifiers in a portfolio context.”

Economic sensitivity

A key risk to the diversification aspects of silver, platinum and palladium, however, is their increased links to economic cycles because of their industrial uses. That could mean these metals underperform gold in an economic downturn as investors flock to the perceived safety of the yellow metal.

Options for investing in precious metals

Investing vehicles for precious metals have proliferated in recent years, but retail investors just dipping their toes in the water will probably want to consider three relatively straightforward methods — buying bars or coins, shares in mining companies or funds that invest in mining companies or that are backed by physical metals.

1. Buying bars or coins

Investors can buy all four of the aforementioned precious metals in the form of bars or coins, also known as bullion.

While bullion provides the most tangible way to invest in precious metals, there are downsides. Storage, transportation and insurance costs all dampen price appreciation, which is the only way to make money with bars and coins because they don’t pay interest or dividends.

Investors will also pay a premium over the value of the physical weight of the metal in bullion form.

2. Buying shares in mining companies

Buying stocks of mining companies in a brokerage account is as easy as buying shares in any other type of company.

You’ll want to pay attention to whether the miner is a smaller company that’s exploring or developing a mine, known as a junior miner, versus a larger enterprise that already has a mine or multiple mines in operation.

The former provides huge returns but comes with more risk, while the latter offers more stability, cash flow and the potential for dividends.

Miners that produce precious metals can outperform when prices rise because their costs are relatively fixed, and higher prices increase their profit margin. They can also sometimes ramp up production to take advantage of higher prices.

However, mining is a risky business, even for established companies. There can be accidents or cost overruns, poor management decisions or the risk that a mine might be closed for political reasons or nationalized.

3. Buying funds for precious metals investment

Exchange-traded funds (ETFs) have become a popular way to own multiple mining companies under a single ticker symbol, making for instant diversification to ward off some of the company-specific risks of investing in mining.

Other ETFs are backed by physical metals held in vaults, with each share representing a certain amount. These have become popular ways to invest in physical metal without having to store it yourself.

Outlook for precious metals investment

Generally speaking, Reddy said his outlook for precious metals is constructive because of falling inflation, a generally stable macroeconomic environment and demand growth from emerging markets and emerging technologies.

Gold

For gold, he sees the combination of possible dollar weakening and continued federal funds rate cuts as supportive. When interest rates fall, non-interest-bearing assets like gold can become more attractive.

Emerging market central banks may also be a source of gold demand, and geopolitical uncertainties might buoy the safe-haven metal, he said.

Silver

“Silver toes the middle ground as both a haven asset and an industrial input, which may position it optimally should economic conditions remain resilient and global demands rise,” Reddy said. “Additionally, the structural growth trends in the solar energy sector may represent a viable source of long-term demand for silver.”

Platinum and palladium

Meanwhile, limited mine production and persistent global deficits may act as short-term floors for platinum pricing.

“The outlook for both platinum and palladium will likely depend on global automotive production, as industrial buyers continue to work through existing inventories of precious metals,” he said. “Prospects for a soft landing within the United States, as well as hopes for a recovery in Chinese demand, offer possible tailwinds for the sector. We believe that there are also long-term structural demand growth opportunities for these metals, as renewable investments ramp up.

What to know before investing in precious metals

Before investing in precious metals, Ebkarian said investors should determine whether they are looking for long-term wealth preservation, capital appreciation or portfolio diversification. They should also determine an exit strategy when thinking about what metal to invest in and whether to do that through stocks, physical metal or other options. Considering liquidity is an important part of that, as some metals and investment vehicles are more easily sold than others.

Gold is the best option for long-term investments, while silver might be better for short- to mid-term objectives, he said. Platinum might be better for portfolio diversification, exposure to industrial demand and potential for price appreciation, while palladium could be better suited for those who want to capitalize on strong automotive demand, supply constraints and potential price growth, he added.

“Consider diversifying your wealth into two or three metals versus choosing one over the other,” he said. “This allows you to minimize risk.”

Frequently asked questions (FAQs)

Which precious metal is the best investment option for beginners?

Reddy said gold and silver might be best for beginner investors given their large trading markets and high liquidity.

“Gold is the more easily understood of the two, given its primary use as a store of value,” he said. “By contrast, silver’s lower price point may make it an accessible investment for new precious metal investors.”

How much should you invest in precious metals?

Cheveley said institutional investors often allocate 5% to 10% of their portfolios to precious metals, while retail investor allocations vary based on their portfolio and risk requirements.

Reddy reiterated that 5% to 10% figure would be an appropriate part of a diversified portfolio as an upper bound for precious metals.

“Generally, we think that precious metals should make up a limited part of investor portfolios, given their lack of corresponding cash flows and cyclical behavior,” Reddy said. “It’s important that any allocation to precious metals be accompanied by a broadly diversified portfolio of stocks and bonds to avoid negatively impacting long-term performance.”

Various forces are fueling gold’s rise. We take a look at whether it makes sense to latch on to the rally.

Gold is glittering, although not necessarily for the reasons everyone is talking about.

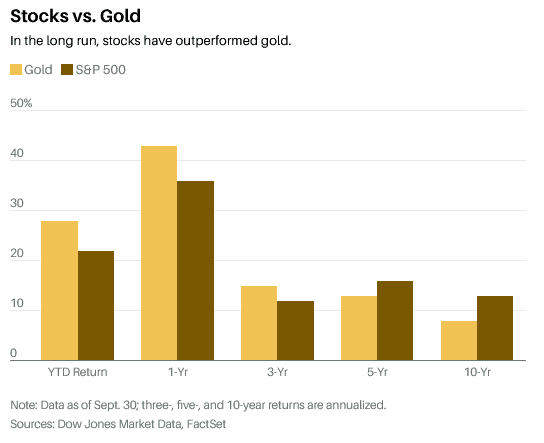

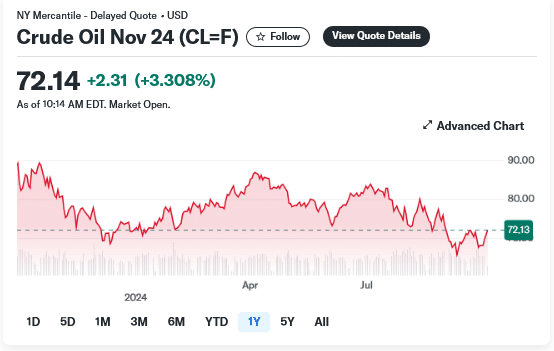

It’s rare for gold to beat stocks, but it’s doing so handily this year. The metal has hit no fewer than 40 record highs, the latest on Sept. 26, when it reached $2,695 an ounce. Prices got a lift after Iran attacked Israel. Its 28% year-to-date return beats the S&P 500.

Short-term trading is part of it. Hedge funds have piled in—collectively they are more bullish than at any time since at least the mid-1980s, according to an analysis of futures market data by Bespoke Investment Group. Some Wall Street firms expect more gains: Bank of America and Citigroup see gold at $3,000 next year, good for an 11% gain from recent prices.

But what’s really behind gold’s ascent? Everyone has a story: falling interest rates, central-bank buying, the rising deficit, or a hodgepodge of horribles like wars, pandemics, and erosion of the dollar’s purchasing power.

There’s truth in all of it, yet most of the stories explaining gold’s rise aren’t as strong as they appear. Gold has support, but it’s important to know what it is, especially if you want to add some to your portfolio.

Consider the interest-rate tale. The idea is that gold should rise as rates decline, which pushes down bond yields and makes bonds less appealing. Gold’s rise this year coincided with the market’s anticipation of rate cuts by the Federal Reserve, along with hopes for more cuts in the pipeline.

But there’s a muddled history of gold and interest rates: According to a 2021 study by researchers at the Federal Reserve Bank of Chicago, soaring inflation expectations from 1971-80 coincided with a surge in gold. The metal’s prices then fell in the early ’80s as inflation and rates started cooling.

In more recent history, gold has been inversely correlated to long-term “real” yields, adjusted for inflation. The idea is that if you own a “risk-free” Treasury bond, for instance, your inflation-adjusted yield will look less attractive as rates fall. That makes gold—and other tangible assets like real estate—more appealing. From 2001 to 2012, long-term real interest rates fell about four percentage points, accompanied by an “over fivefold rise in the real gold price,” the Fed researchers found.

Fund manager Pimco has estimated that a one percentage-point decline in real rates for 10-year Treasury notes should lead to a 24% increase in gold prices. Yet Pimco acknowledges that the relationship hasn’t held lately—gold rallied in the past two years when interest rates were higher. And the real yield on the 10-year Treasury is historically low at around 1.5%, leaving little room for more declines.

Other forces fueling gold’s rise include central banks. Led by China, India, Poland, and others, central banks bought more than 1,000 metric tons of gold in both 2022 and 2023, according to the World Gold Council. Central-bank buying has represented up to a quarter of global gold demand in recent years. Recently, however, purchases have begun to slow as prices crept up. China stopped buying gold in May. Overall, central-bank purchases amounted to just 183 metric tons in the second quarter, down 39% from 300 metric tons in the first quarter.

Gold still only represents 5% of China’s foreign currency reserves, leaving plenty of room for more large purchases. China and other large-scale buyers could become increasingly sensitive to gold prices. But if the dollar loses value as U.S. interest rates fall, central banks in China and other countries may pick up more gold as a reserve currency (though it would be more costly).

Gold bulls are pinning hopes on retail investors stepping up and buying through exchange-traded funds. Investors pulled more than $4 billion from these funds in 2023 as prices climbed, according to Morningstar data. Money continued to pour out during the first half of 2024, but fund flows turned positive in July.

“Gold ETF holdings are starting to increase,” says Imaru Casanova, portfolio manager of the VanEck International Investors Gold fund. “We see the re-emergence of Western investors as a very strong near-term catalyst.”

Longer term, gold bulls argue that the metal will hold up against the dollar or other currencies losing value. Granted, this is an ancient argument promoted by those who constantly worry about governments inflating away the value of their “fiat” currencies. And it doesn’t necessarily mean gold will beat other “real” assets like commodities or real estate. Stocks with cash flows and dividends would also be a hedge.

The idea, though, is that we’re entering dangerous fiscal territory: The U.S. debt has swelled to more than 120% of GDP, and neither Vice President Kamala Harris nor former President Donald Trump has spent much time talking about curbing the deficit or the country’s $35 trillion public debt.

In theory, the growing imbalance between tax receipts and spending will force the government to “print money,” leading to dollars losing value and prompting people to buy gold, due to its relatively fixed supply. (The same argument is made for Bitcoin as “digital gold.”)

Some advisors say that’s a good reason to buy. “It doesn’t matter who is running the government; they are both spending,” says Arnold Van Den Berg, founder of Austin, Texas–based registered investment advisor Century Management. The firm started adding gold to clients’ portfolios two to three years ago and now has it at 6% to 7% of most accounts, says Van Den Berg, who worries about inflation eroding the purchasing power of dollars.

“We’re not gold bugs. I bought gold in the 1970s, but we didn’t own it again until a few years ago,” he says. “We can’t predict what inflation is going to be but I have a pretty good sense history repeats itself.

Some fund managers like the geopolitical argument. Gold’s recent rally coincided with Russia’s invasion of Ukraine in 2022. On Oct. 1, as Iran fired missiles at Israel, gold rose 1%. Pimco portfolio manager Greg Sharenow is bullish on gold, partly because geopolitical instability has increased. Russia’s invasion of Ukraine “was a fracturing of the world order,” he says.

What’s an ounce worth? Gold doesn’t have cash flows, so analysts try to peg prices to other commodities, demand from China, and factors like jewelry demand in India. Data analytics firm Quant Insight uses mathematical models to gauge which macroeconomic factors are driving prices; they conclude that gold today is most closely linked to copper—a proxy for Chinese growth. The firm says gold is more or less fairly valued, given today’s macro picture.

Other firms see gains ahead. Leuthold Group notes that gold historically does well after each rate cut in an easing cycle and actually gains momentum as the cycle progresses and the dollar weakens. “The rally looks a bit extended in the near term,” the firm said in a recent note, but “there is plenty of room for upside from a medium- to long-term perspective.”

There are a number of options for investors, including bullion, mining stocks, and gold ETFs.

Buying bullion holds a certain appeal, and has been a hit for Costco Wholesale: Members rush to snap up $2,689.99 single-ounce bars that quickly sell out. But apart from the hassles of storage, selling bullion may require a dealer who will charge a markup— sometimes as much as 5% to 10%.

Gold miner stocks present a different problem. While cheap and easy to trade, their share prices don’t always match gold’s price moves. That has been especially true over the past several years, when higher labor costs cut into profit margins. While gold prices have jumped 71% over the past five years, the VanEck Gold MinersETF has returned 44%. Gold miners have leapt ahead over the past few months, but the mining industry’s ups and downs are an added variable.

That leaves ETFs like the $75 billion SPDR Gold Shares and the $32 billion iShares Gold Trust . These funds charge fees—0.4% for the SPDR fund and 0.25% for the iShares version—but they offer direct exposure to gold, and investors can buy and sell them cheaply and easily in a brokerage account.

How much to own depends on your appetite for insurance. Arnold’s approach is in line with some asset allocation research, which argues that gold can smooth your portfolio’s returns. Most advisors recommend keeping allocations below 15%.

Keep in mind that if gold keeps rallying, it may be for bad-news reasons. Pessimism about the economy’s future is usually positive for gold, according to academic research. Watch the University of Michigan surveys of consumer sentiment. Gloomier forecasts by consumers are good for gold and worse for stocks.

“Gold is the counterinvestment,” says Martin Murenbeeld, editor of Capitalight Research’s Gold Monitor. “Have a little in your portfolio and hope it doesn’t go up.”

Mohamed El-Erian says the Federal Reserve needs to renew its focus on its fight against rising prices after September’s surprisingly hot jobs report served as a reminder that “inflation is not dead.”

His comments came after Friday’s numbers blew away estimates, triggering a jump in US stocks and bond yields. Nonfarm payrolls rose by 254,000 in September, the most in six months.

“This is not just a solid labor market, but if you take these numbers at face value, it’s a strong labor market late in the cycle,” El-Erian, the president of Queens’ College, Cambridge, told Bloomberg Television on Friday.

“For the Fed, it means push back much harder against pressure from the markets to put you in the single mandate box,” he added. “Enough talk about, ‘The Fed should only be concerned about maximum employment.’”

Investors rapidly slashed wagers on sharper Fed policy easing in November and December after the release. The data also showed the unemployment rate unexpectedly fell to 4.1%, while annual wage growth picked up to 4%.

Swaps traders are now factoring in a little over 50 basis points of interest-rate cuts from the US central bank before the end of the year, down from more than 60 on Thursday. The yield on policy-sensitive two-year Treasury yields surged after the release, trading more than 15 basis points higher at 3.86%.

“For markets, this is pushing back on overly aggressive expectations of rate cuts by the Fed,” said El-Erian, who’s also a Bloomberg Opinion columnist. “This will get the market closer to what’s likely.”

A strike hitting ports along the East and Gulf coasts could stoke prices for food, autos and a host of other consumer goods but is expected to cause only modest broader impacts — so long as it doesn’t drag on for too long.

From a macro perspective, the impact will depend on duration. President Joe Biden, under powers granted by the Taft-Hartley Act, could step in and order an 80-day cooling off period that would at least temporarily halt the stoppage, though there’s little indication he will do so.

That will leave hopes in the hands of negotiators for the union and the U.S. Maritime Alliance that the strike won’t drag on and cause greater hardship for a U.S. economy heading into the critical holiday shipping season.

“Labor action by port workers along the East and Gulf coast of the United States will provide a modest hit to GDP,” said RSM’s chief economist, Joseph Brusuelas, who put the weekly impact at a bit more than 0.1 percentage point of gross domestic product and $4.3 billion in lost imports and exports.

“Given that the American economy is on a 3% growth path at this time we do not expect the strike to derail the trajectory of the domestic economy or present a risk to an early and unnecessary end to the current economic expansion,” he added.

Indeed, the $29 trillion U.S. economy has dodged multiple land mines and has been in growth mode for the past two years. The Atlanta Federal Reserve is tracking third-quarter growth of 2.5%, boosted by an acceleration in net exports.

A prolonged work stoppage, though, could threaten that.

Impacted areas

Some of the main industries facing challenges include coal, energy and agricultural products. One rule of thumb is that for each strike day, it takes nearly a week to get ports operating at normal levels.

“The costs of the strike would escalate over time as backlogs of exports and imports grow,” Citigroup economist Andrew Hollenhorst said in a client note. “Perishable products like imported fresh fruit might be first to come into short supply. If the strike extends beyond a few days, shortages of certain production inputs could eventually slow production and raise prices for manufactured goods like autos.”

There are potential buffers, though, to the damage a strike could cause.

For one, West Coast ports are expected to take on some of the freight business that would normally go to the eastern ports. Also, some companies had been anticipating the stoppage and stockpiled ahead of time.

Moreover, pressure on supply chains, exacerbated sharply during the pandemic, has largely eased and is in fact below pre-Covid levels, according to a New York Fed measure.

“We think fears around the potential economic impacts are overdone,” wrote Bradley Saunders, North America economist at Capital Economics. “Frequent shocks to supply chains in recent years have left producers more attuned to the risks of running low inventories. It is therefore likely that firms will have taken precautionary measures in case of a strike – not least because the possibility has been touted by the ILA for months.”

Saunders added that he thinks there’s a strong possibility that the White House could step in to the fray and invoke a cooling-off period, despite the administration’s strongly pro-union leanings.

“There is little chance that the administration would risk jeopardizing its recent economic successes less than two months before a tightly-contested election,” he said.

Inflation threat

In the meantime, there are a slew of other issues that could complicate things.

Snags in the supply chain could exacerbate inflation just as it appears price pressures have cooled from their mid-2022 peak that sent the annual rate to its highest level in more than 40 years. The maritime association is proposing raises approaching 50%, another factor that could reignite inflation just as wage pressures also have receded. The union is looking for larger increases plus guarantees against automation.

“This is clearly transitory. They will have some resolution,” said Christopher Ball, economics professor at Quinnipiac University. “That being said, in the short run, if it lasts more than a few days, if it lasts more than a week … that will certainly push up the prices of a lot of those goods and services now. It could cause price spikes in the short run during the strike, and I can easily see that pushing up prices of certain goods a lot.”

Ball expects the main areas to be impacted will be food and vehicles, both of which have exerted either disinflationary or deflationary pressures in recent months. Small businesses near the ports also could feel adverse impacts, he added.

“If it goes a week or two, you’re running into businesses that have real shortages and, yeah, they’ll absolutely have to raise those prices just to prevent broad shortages of those goods,” Ball said.

That all comes at an inopportune time for the Federal Reserve. The central bank last month cut its benchmark borrowing rate by half a percentage point and indicated more trimming is to come as it gains confidence that inflation is easing.

However, the strike could complicate decision-making. The October jobs report, which is the last one the Fed will see before its Nov. 6-7 policy meeting, will be influenced both by strike-impacted layoffs as well as those from Hurricane Helene.

It coincides with a looming presidential election on Nov. 5, and the economy as a pivotal issue.

“This would just completely complicate everything that the Fed is trying to do because they’re not getting a read to what the economy is actually performing,” Jim Bianco, head of Bianco Research, told CNBC’s “Fast Money.”

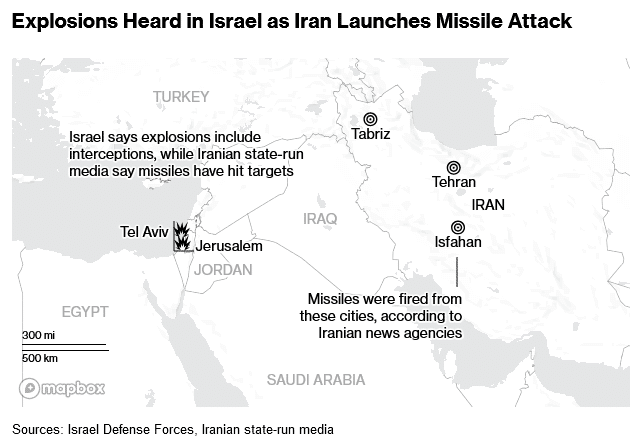

Israeli Prime Minister Benjamin Netanyahu is telling Iran that Israel can “strike anywhere.” But so can its enemies.

Iran’s latest barrage of missiles against Israel was again easily repelled. But two blasts near Israel’s embassy in the outskirts of Copenhagen today show how the Middle East’s spiral into a multi-front war has unknowable ramifications for the entire region and beyond.

Few could have foreseen how far the violence would expand when Iran-backed Hamas attacked Israel on Oct. 7 from its base in Gaza, killing 1,200 people and abducting 250 others, followed a day later by Hezbollah firing rockets into northern Israel from Lebanon.

Israel’s response, reducing the Palestinian enclave to rubble and claiming the lives of more than 40,000 people, ignited global protests and spurred allegations of war crimes, which Israel denies.

Netanyahu has promised to repay in kind yesterday’s long-range Iranian missile launches against his country. How such region-rattling reprisals might transpire hinges on targets and timing.

Former Prime Minister Naftali Bennett, one of Netanyahu’s most potent rivals, argues it’s the moment for a long-promised strike on Iran’s nuclear sites.

The focus now is on whether Iran has lost face, as its firepower appears simply no match for Israel. Questions are also being asked about whether Netanyahu was justified in defying pleas from the US and others for caution, and if escalation — taking out Hezbollah’s leader and a ground incursion in Lebanon — was the right move.

Lebanon is practically a failed state. Its government says a million people have been displaced. Meanwhile, Turkey is taking measures within Syria to halt a new surge of refugees and fears an unstoppable flow of people fleeing Iran.

Washington seems in a bind too, a month from the US elections. President Joe Biden doesn’t want his legacy to be one of unprecedented instability and is keen to avoid denting Vice President Kamala Harris’ chances of prevailing over Donald Trump.

We’re in dangerous and unpredictable new territory.

But there’s another key driver adding structural bullishness to commodities: China’s largest stimulus package since the pandemic, with the promise of more to come.

New support for China’s beleaguered housing market this week adds to prior measures — including support for Chinese-listed stocks — which all told now total over $500 billion (though estimates vary widely).

These aggressive actions are already reverberating through global commodity markets. Iron ore futures have surged over 20% in China, leading Jim Bianco, president of Bianco Research, to weigh in on X:

“The Chinese finally stimulating domestic demand gives hope that they will start to consume more. This idea is significantly contributing to this unfolding rally in industrial metals.”

Connecting the dots, it’s a short trip to higher energy prices. As Bianco notes, “The Chinese consume more energy than the US or the EU.”

Institutional investors have been caught flat-footed all around. According to the BofA September Global Fund Manager Survey, China’s growth expectations had fallen to a record low. Any shorts have likely been sent scrambling.

But US consumers might not feel the pinch in oil and gas prices, as OPEC+ was already on track to increase production by 180,000 barrels per day, starting in December. The move, spearheaded by Saudi Arabia, would increase their market share at the expense of lower prices.

For US stock investors, there may be a trade to capitalize on in the confusing geopolitical melee. In a separate report published Tuesday, BofA Global Research upgraded the Materials sector (XLB) to Overweight, saying that the sector has the highest correlation to China’s economic growth.

BofA noted that large-cap materials suffered the most when the Federal Reserve aggressively raised rates starting in 2022. It also highlighted the sector’s underweight positioning by long-only managers, both of which leave room for a potential re-rating as China’s demand accelerates.

“Underinvestment in manufacturing, single-family [homes], [and] mining over [the] last decade should drive [materials prices] higher,” noted the bank.

Commodities, it seems, are primed to have a moment.

Gold prices on COMEX rebounded from losses earlier in the day as escalating tensions in the Middle East aided safe-haven demand for the precious metal.

The Palestinian militant group Hamas said that its leader, Fatah Sharif and his family was killed in an Israeli airstrike in Lebanon Monday. The news supported demand for safe-haven assets such as gold.

However, gold prices were under pressure in Asian trade today after the US Federal Reserve Chair Jerome Powell on Monday signalled a moderate pace in the central bank’s easing cycle.

Powell says Fed in no hurry to cut rates

On Monday, Fed Chair Powell said that interest rates may fall to a level that neither restricts nor boosts the economy, though the central bank is not in a hurry to cut rates further.

Powell said at the National Association for Business Economics Annual Meeting, Nashville, Tennessee:

Looking forward, if the economy evolves broadly as expected, policy will move over time toward a more neutral stance. But we are not on any preset course. The risks are two-sided, and we will continue to make our decisions meeting by meeting.

The US Fed at its last policy meeting cut interest rates for the first time in four and a half years by 50 basis points to begin its monetary policy easing cycle.

Gold prices have benefited from the interest rates cut as lower rates boost demand for the non-yielding yellow metal.

“If the economy slows more than we expect, then we can cut faster. If it slows less than we expect, we can cut slower, and that’s really what’s going to decide it. But I think from a base case standpoint, we’re looking at it as a process that will play out over some time, not something that we need to go fast on,” Powell said on Monday.

Traders will be assessing these data points to understand the direction of the monetary policy easing cycle of the Federal Reserve in the months to come.

“The moderation in job growth and the increase in labor supply have led the unemployment rate to increase to 4.2 percent, still low by historical standards. We do not believe that we need to see further cooling in labor market conditions to achieve 2 percent inflation,” Powell said.

Gold prices still near record highs

Even though the US Fed has hinted at a slower pace in its monetary policy easing cycle, gold prices are still likely to benefit from lower rates.

Neils Christensen, editor at Kitco.com, said in a report:

Gold has managed to maintain its purchasing power, achieving broad-based gains and reaching all-time highs against major currencies like the euro, the British pound, the Canadian dollar, and the Australian dollar.

At the time of writing, the most-active December gold contract on COMEX was 0.2% higher at $2,665.45 per ounce.

Christensen added:

Althoughgold prices encountered some resistance at all-time highs above $2,680 an ounce last week, many analysts expect the precious metal still has plenty of upside as the Federal Reserve now leads central banks in a global interest rate easing cycle.

It wasn’t that long ago that candidates vying for the White House tried to win voters over with their plans to reduce the budget deficit, or, better yet, leave the country with no deficit at all.

But now, as the dangers of a widening deficit and mounting debt grow, former President Donald Trump and Vice President Kamala Harris are making little effort to address it. Quite the opposite: Both their economic policy agendas, if enacted, would add to the ever-growing deficit, several nonpartisan groups project.

That’s a major problem, though, and Americans cannot afford to have a president who takes the issue lightly, with everything from your ability to afford buying a home to the government’s ability to deal with emergencies like Covid on the line.

A budget deficit occurs when a country’s spending exceeds what it collects in revenue, primarily through taxes. The government makes up the difference by borrowing money through sales of securities like Treasury bonds and notes. The deficit is expected to widen under the status quo and could get even worse under proposals by both Harris and Trump, if enacted.

Already, the US is knee-deep in debt. At $28 trillion, publicly held federal debt is worth almost as much as the entire US economy.

Even Federal Reserve Chair Jerome Powell, who seldom weighs in on what elected officials should do, is concerned.

“It’s probably time, or past time, to get back to an adult conversation among elected officials about getting the federal government back on a sustainable fiscal path,” Powell said in a “60 Minutes” interview earlier this year.

During the Trump-Harris presidential debate earlier this month, the budget deficit was mentioned just twice, when Harris jabbed Trump for his proposals, which are expected to add considerably more to the deficit than hers. However, neither she nor Trump spoke about trying to reduce the deficit, and the moderators of the debate didn’t ask about it.

No matter who wins the presidential election, there will be a “mandate to make things worse unless something changes,” said Maya MacGuineas, president of the nonpartisan Committee for a Responsible Federal Budget. The debt contributions both candidates’ plans carry would undermine “every part of their agendas about helping American families,” she said.

It wasn’t always like this

During the third presidential debate leading up to the 2008 election, then-Senator Barack Obama said, “There is no doubt that we’ve been living beyond our means, and we’re going to have to make some adjustments.”

“I have been a strong proponent of pay-as-you-go,” he added. “Every dollar that I’ve proposed (spending), I’ve proposed an additional cut so that it matches.”

The government had just wrapped up a fiscal year where it ran a $450 billion deficit, not adjusting for inflation. Still, that’s one-fourth the $1.9 trillion deficit the country is running for the 2024 fiscal year.

When Obama sought a second term, now-Senator Mitt Romney, then the Republican presidential nominee, said at one of their debates, “My number one principle is there’ll be no tax cut that adds to the deficit.” Obama and Romney even spent a good chunk of a debate butting heads over whose plan would be better for the deficit.

In fiscal year 2017, when Obama left office, the nation’s deficit clocked in at $670 billion, about half as large as when he arrived in 2009. But that’s mainly a result of moving past the Great Recession, which meant the government didn’t spend as much on social safety net programs and far fewer funds were expended on propping up financial institutions.

In 2016, Trump briefly mentioned the deficit in his second debate with Democratic nominee Hillary Clinton, saying, “I will bring our energy companies back and they will be able to compete and they’ll make money and pay off our national debt and budget deficits, which are tremendous.” (The country’s debt is an accumulation of the deficits it has run over time.)

But after Trump took office in 2017, the deficit gradually widened, and the national debt levels grew each year before both skyrocketed in 2020 as government spending ramped up to deal with the health crisis and stimulate the economy. In the 2021 fiscal year, during which Trump left office, the country ran a $2.8 trillion deficit.

Why you should care about the size of the deficit

Wider deficits tend to go hand-in-hand with owing more money to people who buy US debt, creating more risk for the people who loan us money and likely making them demand higher interest returns from the US government. In turn, since banks and other lenders often base interest rates on US bond yields, that could make it more expensive for everyday Americans to get a mortgage.

Additionally, when the government spends more money to pay interest on its debts, there’s less money available to, for instance, invest in new infrastructure. Case in point: The government is set to spend more on interest payments than on national defense, Medicaid and programs dedicated to supporting children, according to Congressional Budget Office projections for the 2024 fiscal year, which ends September 30.

Powell summed it up in his “60 Minutes” interview: “We’re borrowing from future generations,” he said, when instead we “should pay for those things and not hand the bills to our children and grandchildren.”

All the borrowing taking place is slowing economic growth, MacGuineas told CNN. It also may be creating “a national security risk,” since the US has become increasingly dependent on foreign countries like China and Japan to buy our debt, she said.

There’s also a risk that inflation will ramp up if the widening deficit prompts the Fed to “print more money” to help the government pay off its debt, said Kent Smetters, a professor at the University of Pennsylvania’s Wharton School who studies the budget.

If it’s such a big problem, why aren’t Trump and Harris addressing it?

“Politicians love to deliver gravy and not the spinach,” said Smetters, the faculty director of the Penn Wharton Budget Model, a nonpartisan research initiative that forecasts the effects of fiscal policies.

There’s also a game of chicken going on, he said. “Both sides want to get their stuff in there before sacrifices have to be made.” For Republicans, that means solidifying more tax cuts; and for Democrats, getting more government spending out the door. But, eventually, the country risks reaching a pointwhere it can’t continue to borrow more money to get by, which will force elected officials to make tough choices about where to cut spending and levy higher taxes.

Covid and the Great Recession have also made Americans “numb” to thinking about the problems associated with rising debt levels, Smetters told CNN. “In most people’s minds, people are much more likely to see the government borrowing money as a positive effect if it helped us get through a crisis.”

Yet voters fail to recognize that the economy would grow faster and social safety net programs would be funded for longer if the debt burden were reduced, MacGuineas said.

“If there’s deficit denial at the top, what voter is going to say, ‘Please raise my taxes and cut my spending’ if their leaders aren’t even saying it’s a problem?”