Key Points

- The Federal Open Market Committee lowered interest rates by a quarter of a percentage point, setting the target range between 4% and 4.25%.

- Federal Reserve officials hold differing views on economic direction, with some prioritizing labor market weakness and others inflation risks.

- August saw only 22,000 nonfarm positions added and unemployment rose to 4.3%, with 13,000 jobs lost in June.

There may have only been one official dissent vote at the Federal Reserve’s policy meeting last week, but recent comments from policymakers show there are wide and differing viewpoints on where the economy is heading and what potential pitfalls need to be prioritized.

The Federal Open Market Committee opted to lower interest rates by a quarter of a percentage point on Sept. 17, pushing the target fed funds range down to between 4% and 4.25%. Only newly minted Federal Reserve governor Stephen Miran dissented, contending that a half percentage point cut was warranted. On Monday, he noted that monetary policy was “very restrictive” and keeping it elevated risked “unnecessary layoffs and higher unemployment.”

But while Fed officials were more in step with their vote than perhaps expected, there’s little consensus around what lies ahead at this point and which part of the Fed’s dual mandate of maximum employment and price stability needs more attention right now.

Some, like Fed governor Michelle Bowman, continue to warn that materially weaker labor conditions call for a more neutral stance on rates. But others, including Atlanta Fed President Raphael Bostic, are concerned about the risks of higher inflation and call for a more cautious approach to lowering rates lest it spur more price growth.

Bowman, who dissented at the July meeting in favor of a rate cut, said in a speech Tuesday that recent data have revealed a “materially more fragile labor market.” Yet when it came to inflation, she was less worried, noting that price growth continued to hover not far above the Fed’s 2% target.

“I am also more confident that, as trade policy has become more certain, tariffs will have only a small and short-lived effect on inflation going forward,” Bowman said, adding that she was pleased Fed officials have finally begun lowering rates given this shift in labor market conditions.

In August, employers only added about 22,000 nonfarm positions and unemployment ticked up to 4.3%. Additionally, updated estimates of previous monthly payrolls revealed that the economy lost 13,000 jobs in June.

She added that it was “appropriate to begin the process of moving policy toward a more neutral stance” at the September meeting, and that it was important policymakers signaled that additional adjustments were in the offing. In the Fed’s latest summary of economic projections, the median forecast for rates signaled there would be two additional quarter-point cuts this year.

“If the statement had not included a reference to additional cuts, it would have signaled to markets that the committee would not be responsive to weakening labor market conditions,” Bowman said.

But while labor conditions have softened, not all committee members are convinced that these conditions call for significant cuts. The Atlanta Fed’s Bostic said Tuesday that the central bank hasn’t been at target for inflation for four and a half years, so that remains something “we definitely need to be concerned about.”

Policymakers expect the personal consumption expenditures index will top out at 3% this year, not returning to the 2% target until 2028, according to their latest economic projections. Economists surveyed by FactSet are forecasting that the latest PCE inflation reading—due out on Friday—will show prices rose 2.9% in August from a year earlier.

“There’s been a lot of discussion and debate about whether one would expect that tariffs would have an impact on inflation initially and to date, it’s been much more muted, I think, than many expected,” Bostic acknowledged.

But he says it’s still up in the air on whether the changes in tariff policy will ultimately result in a one time shifts or structural changes. Bostic noted that business leaders are telling the Atlanta Fed they are feeling the cost pressures from higher tariffs, and it is becoming increasingly difficult to prevent those from flowing into prices that are faced by consumers.

“I actually think there’s still more to come,” Bostic said. “I’m still worried about it…I don’t think we’re at target today, and given that the forces and the pressures are likely to move us away from that in the short and medium term, I really think we need to pay very close attention to the consumer psyche and to what businesses plan based on what they’re expecting the future to have.”

He added that he has been worried from the “very beginning” that once people have an experience with high inflation they’ll expect that moving forward.

Employment conditions are important as well, Bostic said, though he noted that labor supply and demand are both softer and that could help provide some balance. He also noted that he’s still hearing from businesses that while they’re not hiring, they’re also reluctant to fire anyone.

Keeping the options open and remaining flexible to respond to the changing economic landscape, however, are things policymakers can agree on. “If something happens, we will be responsive and as forcefully as possible,” Bostic added.

Read the full article HERE.

Federal Reserve Governor Stephen Miran said the US central bank risks damage to the economy by not moving rapidly to lower interest rates.

“I don’t think the economy is about to crater. I don’t think the labor market is about to fall off a cliff,” Miran said Thursday on Bloomberg Surveillance.

But given the risks, “I would rather act proactively and lower rates as a result ahead of time, rather than wait for some giant catastrophe to occur,” he said.

Miran, a new Fed board member who was appointed by President Donald Trump, is an outlier among the central bank’s policymakers in calling for immediate, aggressive rate cuts. He argued the Fed’s current policy rate, which is in a range of 4% to 4.25%, is highly restrictive because it’s well above his estimate of the so-called “neutral” level — where policy neither boosts nor restrains the economy.

“The neutral rate is drifting down, and as a result of that, it’s incumbent upon policy to adjust in response,” Miran said. “If policy stays excessively restrictive for too long, then you do get to a situation in which you have a meaningful increase in the unemployment rate.”

Miran spoke just before data released Thursday morning showed second-quarter growth in gross domestic product accelerated to the fastest pace in nearly two years, underscoring the US economy’s resilience. Separate data published simultaneously showed weekly initial filings for unemployment insurance fell to the lowest level since July.

Fed officials voted to lower interest rates at their meeting last week by a quarter percentage point, the first cut of 2025. Miran dissented against the decision, instead favoring a half-point cut.

Several policymakers, including Fed Chair Jerome Powell, have approached rate cuts cautiously, amid concerns Trump’s tariff policies might persistently boost inflation. Powell has said that possibility, along with signs of a weakening labor market, poses a challenge for the Fed’s decision-making in the months ahead.

Kansas City Fed President Jeff Schmid, in remarks prepared for an event Thursday in Dallas, said he supported the recent rate cut but hinted he may not back another reduction any time soon.

“I viewed the 25-basis point cut in the policy rate last week as a reasonable risk-management strategy,” Schmid said. “That said, my view is that inflation remains too high while the labor market, though cooling, still remains largely in balance.”

Speaking earlier Thursday on the Fox Business network, Miran said officials can quickly implement several larger cuts to reach the neutral level, rather than moving slowly over the course of the year.

“My view is that we can get there in a very short series of 50-basis-point cuts, readjust monetary policy, and then move more gingerly once we’re there,” he said.

Read the full article HERE.

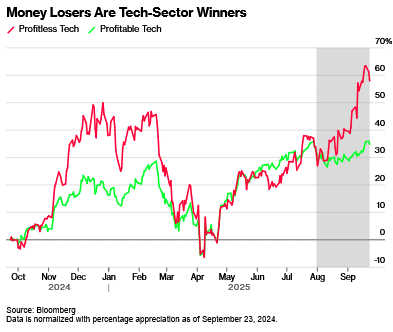

Bets that the Federal Reserve will continue cutting interest rates have fueled a rally in one of the riskiest corners of the technology sector, raising concerns about a potential reversal in the stocks.

A basket of unprofitable tech companies tracked by UBS Group AG has jumped 22% since the end of July, compared with a 2.5% advance for its profitable counterpart and the Nasdaq 100 Index’s 5.9% advance. The run-up has sent the group, which includes lesser-known companies like SoundHound AI Inc. and Unity Software Inc., near its highest since late 2021, when rock-bottom interest rates were fueling a bubble in speculative assets that popped the following year.

The basket of loss-making tech firms rose 0.7% Wednesday, while the profitable equivalent rose 0.4%.

The potential of a hard landing for the stocks was highlighted on Tuesday, when the group sank 2.1%, underperforming the market after Fed Chair Jerome Powell reiterated his view that policymakers face a difficult road ahead as they weigh further rate changes. Even if the central bank follows through with two more cuts this year, the benchmark rate will likely remain above 3%, a far cry from the zero-interest-rate policies during the pandemic that fueled equities.

The move in unprofitable tech stocks marks “a phase of speculative over-exuberance because the expected rate-cut cycle is leading to animal spirits being revived,” said Ted Mortonson, a tech strategist at Robert W. Baird & Co. “The rally looks extremely frothy and risky, and all the speculation from the Reddit and Robinhood crowds makes it feel like a casino, which makes me think this will end with disillusionment.”

With inflation still a problem and artificial intelligence weighing on the labor market, it’s “extremely tricky” to analyze the value of money-losing companies based on what the Fed may or may not do, Mortonson added. Lower borrowing costs are crucial for money-losing firms that need to finance fast-growing operations at valuations based on profit expectations that might take years to hit.

Of course, there are plenty of other areas of the stock market where speculation is running rampant amid prospects for lower rates. Riskier biotech plays are surging and the Russell 2000 Index of small caps recently hit its first record since 2021. However, the move in tech has been pronounced.

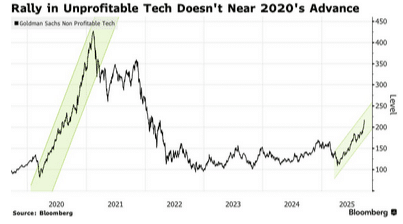

A similar unprofitable basket tracked by Goldman Sachs has nearly doubled from an April low, and recently hit its highest since February 2022.

Notable winners include OpenDoor Technologies Inc., a so-called meme stock championed by Canadian hedge-fund manager Eric Jackson, which has soared by more than 280% since the end of July. IonQ Inc., a quantum-computing company, is up more than 80% over the same period, while SoundHound AI, Xometry Inc. and Lemonade Inc. have gained more than 50%.

Despite the rally, the moves still pale in comparison with the start of the decade. Goldman’s basket soared more than 420% from March 2020 to February 2021 before giving most of the gains over the following 15 months.

Still, some investors see validity in the recent move higher, especially since the scope of the so-called dash for trash is smaller than in the previous rate-cutting cycle. Goldman’s basket for example remains about 50% below its 2021 peak.

“I don’t think the exuberance is unfounded, since growth has been decent, there’s more visibility on tech earnings than other industries, AI is a unique secular tailwind, and the rate backdrop looks favorable,” said Anthony Saglimbene, chief market strategist at Ameriprise Financial Services Inc. He said “it isn’t a stretch to see more risk taking in speculative areas, which is where you find the untapped sources for upside.”

Despite that, Saglimbene stressed that the rally in unprofitable tech stocks could turn easily, with shares in the group likely to face more pressure than their high-quality counterparts in the event of a broader economic downturn.

“The Fed is likely to remain guarded with its rate path, and if it starts to cut more aggressively, that’s probably because something is breaking in the economy, which won’t be positive for risky or unprofitable tech assets,” he said. “We’re in a risk-on mode right now, but if you live by the sword, you might die by it.”

Meanwhile, Alibaba Group Holding Ltd.’s shares surged to their highest in nearly four years after the company revealed plans to ramp up its AI spending past an original $50 billion-plus target, joining tech leaders pledging ever-greater sums toward the race for technological breakthroughs.

Top Tech Stories

- Alibaba is integrating Nvidia Corp.’s suite of artificial intelligence development tools for so-called physical AI into its cloud software platform.

- Cathie Wood’s funds reopened positions in Alibaba for the first time in four years, just as the stock rallied to a multi-year high on optimism over the Chinese firm’s push in AI.

- Three years after OpenAI and Nvidia Corp. helped kick off the global AI frenzy, the two firms are joining forces to pave the way for a more costly phase of development with a deal that’s quickly revived fears of a bubble.

- Micron Technology Inc., the largest US maker of computer memory chips, gave an upbeat forecast for the current quarter, helped by demand for artificial intelligence equipment.

Read the full article HERE.

China aims to become custodian of foreign sovereign gold reserves in a bid to strengthen its standing in the global bullion market, according to people familiar with the matter.

The People’s Bank of China is using the Shanghai Gold Exchange to court central banks in friendly countries to buy bullion and store it within the country’s borders, said the people, who spoke on condition of anonymity as the discussions aren’t public. The effort has taken place over recent months and has attracted interest from at least one country, in Southeast Asia, the people said.

The move would enhance Beijing’s role in the global financial system, furthering its goal of establishing a world that’s less dependent on the dollar and Western centers like the US, the UK and Switzerland. Countries have been snapping up gold as a hedge against mounting geopolitical risks, creating the opportunity for the PBOC to offer a haven for an asset deemed crucial as a buffer to economic shocks.

The PBOC and SGE didn’t respond to requests for comment.

Demand from central banks has been a key pillar in the precious metal’s recent ascent to record highs, and the PBOC itself has been on a buying spree for ten straight months.

Spot gold rose as much as 1.2% to a fresh record after the news, before easing slightly to $3,784.74 an ounce as of 9:42 a.m. New York time.

“Markets may be speculating that China’s bid to host foreign gold reserves signals a long-term push to elevate its role in the global monetary system,” said Wael Makarem, financial markets strategists lead at Exness. “Investors could be interpreting this as incremental de-dollarization momentum, which could support gold.”

The reserves would be held in custodian warehouses linked to the SGE’s International Board, which falls under the PBOC and was set up by the central bank in 2014 as the main venue for foreigners to trade gold with Chinese counterparts. The bullion would be made up of new purchases that count toward the foreign country’s reserves, rather than being relocated from existing stockpiles, the people said.

While China’s move marks another step toward building its role in global bullion trading, it remains some way from challenging established hubs such as the UK. The Bank of England’s vaults hold over 5,000 tons of the world’s reserves, worth nearly $600 billion and anchoring the city’s role as the leading marketplace for the precious metal. Custodian services, which safeguard assets on behalf of clients, are key for a gold center, helping to boost credibility and attract more trading.

The PBOC’s reported reserves are less than half that, putting it at No. 5 in the global ranking of central bank holders, according to the World Gold Council. However, China’s domestic market for gold, whether as jewelry or in bars and coins for investment, is the world’s largest.

Boosting local trading even further should help Beijing accelerate its campaign to reduce reliance on the dollar and internationalize the yuan. Bullion has nearly doubled in value to over $3,700 an ounce in the past two years, and recently eclipsed its inflation-adjusted record set in 1980. The blistering rally may have more room to run, with Goldman Sachs Group Inc. predicting it could hit $5,000 if just 1% of privately-held Treasury holdings shifted to gold.

China has already taken a number of steps to open up its gold market. The SGE launched its first offshore vault and contracts in Hong Kong this year, a move designed to increase transaction volumes in the yuan. The PBOC has also recently eased restrictions on gold imports.

For prospective clients, Chinese vaults could be an attractive option to build reserves and help bypass the risk of being cut off from the world’s financial markets. Central bank buying of gold accelerated after the US and its allies froze Russia’s foreign exchange reserves in 2022 after the invasion of Ukraine.

But there are trade-offs, too. “If countries chose to store their gold in China, they will forgo the ease and liquidity in London,” said Nicholas Frappell, Head of Institutional Market at ABC Refinery.

Read the full article HERE.

Citigroup cast doubt on gold’s run in June

Gold was headed for a fresh record on Monday and silver hit a more than decade high, with Citigroup strategists predicting the rally for the precious metals to continue and carry other metals.

Gold jumped $44.40, or 1.2%, to $3,750 an ounce early Monday, putting it on the path for a fresh closing high, potentially its 36th this year. The contract also set a new intraday high, reaching $3,753 an ounce, according to Dow Jones Market Data.

Silver. meanwhile, rose over 2% to $43.86 an ounce, reaching an intraday level of $44.10, not seen since Aug. 2011. Investors are now watching to see if silver at long last reaches a new settlement high — the last was $48.70 an ounce, reached in January 1980.

Citigroup strategists told clients in a note that they are bullish on those precious metals, as well as two others.

“We see the gold and silver bull market broadening and eventually shifting into copper and aluminum during 2026, driven by the prospect of new dovish Fed leadership (by May/June 2026) and related lower U.S. real interest rates and downward pressure on the dollar,” wrote a team led by Maximilian Layton, global head of commodities.

Driving the upside will be cyclical factors — continued weak labor market, tariff-driven U.S. and global growth worries — and structural ones such as worries about U.S. debt and a weakening dollar.

“In addition, we see stimulus from the [One Big Beautiful Bill Act] reaching households and building capex investment momentum during 1H26, driving an improvement in U.S. and global growth and sentiment,” much like late 2007, early 2008,” they said.

Noting that “just about everything is going right for the gold bull market at the moment,” Layton and his team suggest buying any dips in gold prices, targeting $3,800 an ounce in the next three months, but seeing it peak in the first quarter of next year. Their bull case sees gold reaching $4,000 in the coming months in a scenario of stagflation and growing Fed independence concerns. A bear case projects prices to dip to $3,400, with the economy muddling through and geopolitical de-escalations.

As for aluminum, the strategists say they are “very bullish” over the next six to 36 months, saying any dips would represent “strong long-term buying opportunities.”

“Aluminum is heavily exposed to AI/datacenters, humanoid/other robots given competition for power from the same future-facing sectors, which are driving aluminum demand (aluminum supply is highly power intensive) and given China’s capacity cap,” said Layton and the team.

As for copper, they have a $12,000/ton base case for the next six to 12 months, marking 20% upside, and a bull case of $14,000/ton. “While we are neutral for 4Q25, copper is exposed to structural energy-transition and AI trends and is leveraged to a pickup in U.S. and global growth expectations from 2026, given dovish Fed prospects (especially from May 2026) and related lower U.S. real interest rates,” they said.

Citigroup warned in June that gold prices could be headed for a fall in 2026. In their latest forecasts, though, they have walked back some of that negativity.

In the first quarter they see gold at $3,700 an ounce from a previous $2,900 an ounce. By the fourth quarter of 2026, they see gold at $2,800 an ounce, slightly higher than the $2,600 they had predicted previously

Read the full article HERE.

Unemployment and inflation are starting to rise. But more troubling: how skewed the AI economy is.

The United States is entering a period that looks and feels like stagflation, the dreaded s-word that hasn’t been uttered much since the 1970s and early 1980s. It means both unemployment and inflation are climbing. So far, it has been a modest rise that is probably best described as “stagflation-lite,” but it’s still distressing because it’s almost impossible to cure both of these ills at the same time.

Federal Reserve Chair Jerome H. Powell didn’t use the s-word on Wednesday, but he repeatedly called the situation “unusual.” Fed leaders have predicted conditions will worsen in the coming months, with inflation on track tohit 3 percent(up from 2.2 percent in April) and unemployment expected tohit 4.5 percent (up from 4.2 percent in April). Powell made it clear he’s more worried about the deteriorating jobs situation. The Fed just lowered interest rates by a quarter point (and signaled more cuts are coming before the end of the year) to prevent more layoffs and avoid a recession.

Typically, when people lose their jobs, there’s a downturn, and prices tend to flatline as businesses offer deals to win back customers. But this is a strange time for the economy, mainly because of the highest tariffs in 90 years and the AI boom. These forces are skewing the economy.

Prices for many goods are rising as companies pass along the tariffs they are paying to import items and parts from overseas. At the same time, many business leaders think they over-hired in 2023. The latest job revision data showing 911,000 fewer jobs created between April 2024 and March 2025 suggest many firms slowed hiring in 2024. Now, in 2025, they are growing more cautious because of uncertainty. In the next six months, businesses are either going to pass along more of the tariff costs to consumers or they are going to cut costs by laying off workers. Or a mix of both, as the Fed seems to predict.

The nation is in for a turbulent few months as the worst of the tariff impact hits businesses’ and families’ budgets. Polling and consumer sentiment data show fear of and frustration over high and rising prices and a worsening job market. But economic growth is where things get really bizarre. The word “stagflation” comes partly from stagnation. It’s supposed to be a period of weak growth — or even contraction. Yet the U.S. economy expanded at a brisk 3.3 percent in the second quarter, and the latest estimate from the Atlanta Fed indicates the growth rate could be around 3 percent in the third quarter, too.

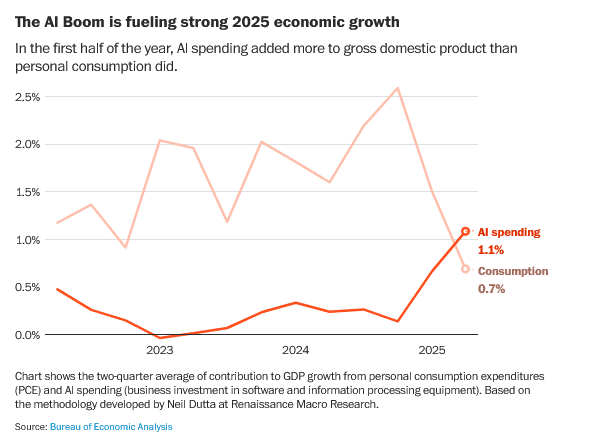

The key to understanding the economy is to recognize that two trends are propping up growth: spending by the rich and companies investing heavily in the AI boom. The economy is highly skewed right now toward certain big players.

So far this year, business spending on software and data centers — mainly for AI — has been a bigger contributor to the economy than consumption. That is stunning. The U.S. is widely known as a consumer economy, where the vast majority of growth typically comes from people spending on everything from burgers and fries to facials and football games. Yet suddenly, this is an AI economy.

As JPMorgan wrote in a recent report, “AI-related capital expenditures contributed 1.1% to GDP growth, outpacing the U.S. consumer as an engine of expansion.” And that spending is dominated by major tech players such as Meta, Alphabet, Microsoft, Amazon and Oracle. (Amazon founder Jeff Bezos owns The Post.)

There’s still some spending going on, but it’s mainly driven by the top 20 percent of earners: those making roughly $175,000 a year or more. As Mark Zandi, chief economist at Moody’s Analytics, points out, the bottom 80 percent of earners are basically treading water: Their spending is just keeping up with inflation. In contrast, the top 20 percent are still growing their spending far faster than inflation, probably because the rich are benefiting the most from record stock-market gains.

There’s a strong likelihood the economy keeps chugging along even as middle- and lower-income households face a big squeeze from higher prices and wages that don’t keep up (or barely do). There’s little incentive for employers to give large pay increases when it’s tough to find another job.

There has been ample discussion about how challenging a stagflation-like environment is for the Fed. As it focuses on cutting rates to stop more layoffs, it runs the risk of higher inflation or some sort of AI bubble forming, reminiscent of the dot-com era. But there’s an equally complex situation in a bifurcated “K-shaped economy” where the top is thriving and the rest are barely staying afloat. Or, in the business context, where AI-related businesses are thriving and many other sectors, such as real estate, farming and manufacturing, are struggling. Which groups are policymakers going to help?

“The fundamental challenge with a K-shaped economy is that for those at the top, you would hike rates sharply — while for those at the bottom, you would lower them dramatically,” said Peter Atwater, president of Financial Insyghts.

There are many unusual forces at play, but too often what gets lost in the conversation is this: It’s a turbulent economy for the middle class, and it would be a mistake to let their situation worsen.

Read the full article HERE.

Despite attempts by the White House to erode the central bank’s independence, Powell showed that he remains firmly in control.

What should one take away from this week’s Federal Reserve monetary policy meeting?

First, Chair Jerome Powell is firmly in control of the interest-rate setting Federal Open Market Committee, which on Wednesday lowered its target for the federal funds rate by 25 basis points to a range of 4% to 4.25%.

Going into the meeting, expectations were that there could be dissents on both sides, with some policymakers in favor of no cut and others in favor of a larger 50-basis-point reduction. And some thought Fed GovernorsChristopher Waller or Michelle Bowman — both appointed to the central bank during the first Trump administration—might join Stephen Miran, the head of the White House’s Council of Economic Advisors who was just sworn in Tuesday as a Fed governor to fill an open slot – in dissenting in favor of that larger cut.

But it wasn’t to be. Those that might have preferred to keep rates unchanged deferred to Powell. Not a surprising outcome, given that the disagreement was about timing rather than direction of rates. In such circumstances, no dissent was warranted.

For Bowman and Waller, it is more difficult to parse their motivations. But their unwillingness to dissent in favor of a larger cut shows that just because one is a Trump appointee doesn’t necessarily mean following his lead. (Recall that Trump has said rates should be closer to 1%.) Their actions demonstrate integrity, commitment to the Fed’s mission and the importance of sustaining the central bank’s independence. A very welcome development!

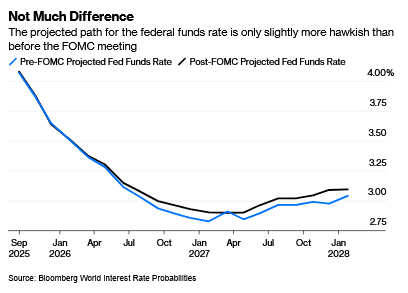

Second, the shift in the median Summary of Economic Projections to 75 basis points of rate cuts by year-end from the 50 basis points projected in June is not significant. Markets initially reacted positively to this development, but the gains turned out to be transitory because on closer examination it was obvious there was no clear consensus. Excluding the one forecast advocating for 150 basis points of cuts this year — which is almost certainly Miran’s projection — the rest of the FOMC was evenly split between one or two more rate cuts.

Third, at Powell’s press conference he was pressed about the apparent inconsistency between cutting the Fed’s rate target at the same time the FOMC raised its median forecast for both economic growth and inflation. I don’t think there is much tension here. The upward revisions were very small, amounting to 0.2 percentage points for both in 2026. More importantly, the motivation for the rate cut was not tied to the modal forecast, but instead was driven by the signs of labor market weakness evident in recent employment data that showed a sharp slowdown in payroll growth to just 29,000 on average over the past three months.

The rationale Powell offered for the rate cut was straightforward, which is that the downside risks to the labor market had increased and come into closer balance with the upside risks to inflation. Because he assessed monetary policy as being “clearly restrictive,” the shift in risks implied that monetary policy should be looser.

So where do we go from here?

Future Fed actions will bedata dependent. Easing will be predicated mainly on whether the downside risks to the labor market are increasing, how the Trump administration’s tariffs pass through into prices and whether the resulting stickiness in inflation pushes up long-term inflation expectations. A series of stronger employment reports, a steady unemployment rate and persistent inflation could undercut support for further easing.

As Powell explained, conducting monetary policy is very difficult right now. First, because the dual mandate objectives of the Fed – full employment and price stability – are in conflict, the Fed has to set policy to balance the risks to those two objectives. As Powell put it, there is “no risk-free path.” Second, tariff policy remains uncertain, with the timing of the tariff impact on prices dependent in part on future court rulings that will govern which tariffs increases are legal. Moreover, while the pass-through of tariffs into prices has been more modest and slower than anticipated, this doesn’t necessarily mean the full effects will be smaller. Instead, the pass-through may just be delayed, reflecting the reluctance of companies to react until they have better visibility.

What about the threat to Fed independence?

Powell was very careful not to respond to questions about allegations by the Trump administration that Fed Governor Lisa Cook lied on mortgage applications or Treasury Secretary Scott Bessent’s critique that the central bank had been guilty of mission creep and should be subject to an independent review. Powell instead pointed to what the Fed was already doing, including the recent revisions to the Fed’s monetary policy framework and the planned 10% reduction in headcount across the Federal Reserve System. Powell concluded that the Fed is always open to ways of improving its operations. He understands that Fed credibility rests on the Fed doing its job — broadly defined — well.

With respect to the third mandate of monetary policy — keeping longer-term interest rates moderate – Powell emphasized that the Fed has not historically focused on this area for a simple reason: If it does a good job in achieving its other two goals of full employment and stable prices, longer-term rates will take care of themselves.

The threat to Fed independence is still very real. While Trump administration may not succeed in removing Cook for cause and not all of Trump’s Fed appointees will necessarily do the White House’s bidding, the efforts show the intent of the President to take control of the central bank. Plus, the administration may explore or invent other options to get its way. The divergence of Miran’s rate forecast from the rest of the FOMC indicates how much monetary policy would likely change if Trump lieutenants were firmly in control. If monetary policy were to follow Miran’s dictate, the result would soon be an overheated economy and higher inflation. Let’s hope that Fed independence with respect to how it conducts monetary policy to achieve the objectives set out for it by Congress prevails.

Read the full article HERE.

Why Is Gold Hitting Record Highs in 2025?

Gold has been on a remarkable run in 2025, surging approximately 40% year-to-date and recently reaching an all-time high analysis of $3,702.95. This impressive performance has prompted Deutsche Bank to significantly revise its price outlook for the precious metal. But what factors are driving this bullish sentiment in the gold market?

Central Bank Purchasing Remains Robust

Central banks worldwide continue to accumulate gold at an extraordinary pace, with official demand running at twice the level of the 2011-2021 average. China has emerged as a particularly aggressive buyer, helping to sustain strong fundamental support for gold prices despite already elevated levels.

The ongoing central bank buying represents a significant shift in global monetary reserves management, with many nations seeking to diversify away from traditional foreign currency holdings.

Federal Reserve Policy Shifts Creating Tailwinds

Deutsche Bank analysts point to several monetary policy factors supporting their revised forecast:

- The Fed is expected to implement three rate cuts in 2025

- Potential additional easing in 2026 contrary to the Fed’s current projections

- Uncertainty surrounding changes in Federal Open Market Committee composition

- Ongoing challenges to Federal Reserve independence

These monetary policy dynamics typically benefit non-yielding assets like gold, which performs well in low-interest-rate environments.

Historically, gold has shown strong inverse correlation with real interest rates, making the anticipated Fed policy trajectory particularly supportive for bullion prices.

What’s Behind Deutsche Bank’s New $4,000 Gold Forecast?

Substantial Upgrade from Previous Projections

In a significant revision, Deutsche Bank has raised its 2026 gold price forecast by $300 to an average of $4,000 per ounce. This represents an 8.1% increase from their previous projection of $3,700 announced earlier in 2025.

The upgraded forecast follows multiple upward revisions from the bank over the past 18 months, reflecting the persistent strength in gold prices despite earlier expectations of a correction.

Supply Constraints Adding Support

The bank noted that recycled gold supply is currently running 4% below expected levels this year, which removes a potential ceiling on price appreciation. With limited new mine supply coming online and recycling activity subdued despite high prices, the supply-demand balance continues to favor higher prices.

Gold mining companies have been cautious about expanding production capacity following previous boom-bust cycles, resulting in relatively constrained new supply despite multiyear price increases.

US Dollar Weakness Expected

Deutsche Bank’s analysis suggests potential US dollar weakness ahead, which historically correlates with stronger gold prices. As the dollar potentially loses value against other major currencies, gold becomes more attractive as an alternative store of value.

The negative correlation between gold and the US dollar has been a consistent market pattern, with currency depreciation often coinciding with bullion appreciation.

What Risks Could Derail the Gold Rally?

Equity Market Competition

Strong performance in global equity markets could potentially divert investment flows away from gold. When stocks deliver robust returns, the opportunity cost of holding non-yielding assets like gold increases.

The historical relationship between gold and equities has been complex, with periods of both correlation and divergence depending on prevailing economic conditions and investor sentiment.

Seasonal Weakness Patterns

Deutsche Bank highlighted that gold has historically shown seasonal weakness during the fourth quarter, based on both 10-year and 20-year trend analysis. This cyclical pattern could create temporary headwinds for gold prices.

The seasonal pattern typically shows:

- Q1: Strong performance (January-March)

- Q2: Mixed performance (April-June)

- Q3: Relatively strong (July-September)

- Q4: Weaker performance (October-December)

Federal Reserve Policy Uncertainty

If US economic conditions remain resilient, the Federal Reserve might hold rates steady in 2026 rather than continuing to cut as markets currently anticipate. Such a scenario would likely be less supportive for gold prices than Deutsche Bank’s base case.

Recent economic indicators have been mixed, creating genuine uncertainty about the future path of monetary policy:

- Employment data shows continued resilience

- Inflation has moderated but remains above target in several categories

- Manufacturing activity has been inconsistent

- Consumer spending patterns show signs of normalization

How Are Other Precious Metals Affected?

Silver Forecast Also Upgraded

Alongside its gold revision, Deutsche Bank also raised its silver price forecast for 2026 to an average of $45 per ounce, up from its previous target of $40. This represents a 12.5% increase in the bank’s outlook for silver.

The bank’s silver upgrade is particularly notable as it represents a more aggressive percentage increase than the gold revision, suggesting expectations for potential outperformance in the industrial/precious metal.

Gold-Silver Ratio Implications

The revised forecasts imply a gold-to-silver ratio of approximately 88:1, suggesting Deutsche Bank expects gold to maintain its relative strength compared to silver, though with silver still posting significant gains.

Historically, the gold-silver ratio has averaged around 60:1 over the long term, indicating:

- Current projections still favor gold in relative terms

- Silver may have additional upside potential if the ratio reverts closer to historical averages

- Industrial demand recovery could further support silver prices

What Does This Mean for Investors?

Portfolio Allocation Considerations

With gold already up approximately 40% year-to-date in 2025 and potentially heading toward $4,000 per ounce, investors may need to reassess their precious metals allocation. Deutsche Bank’s forecast suggests additional upside potential despite already strong performance.

Investment strategies to consider include:

- Maintaining a strategic allocation to gold as a portfolio diversifier

- Potentially increasing exposure during seasonal weakness periods

- Balancing direct metal exposure with mining equities for different risk profiles

- Considering tax-efficient vehicles for precious metals exposure

Mining Company Investment Opportunities

Gold mining companies typically experience operating leverage to rising gold prices, potentially amplifying returns compared to the metal itself. As production costs remain relatively stable while gold prices rise, profit margins for well-positioned miners could expand significantly.

The mining sector presents several interesting dynamics in the current environment:

- Mid-tier producers often provide the best balance of growth and stability

- Royalty companies offer exposure to price increases with reduced operational risk

- Exploration companies offer higher risk/reward profiles but require careful due diligence

- Companies with production costs below $1,200/oz stand to benefit most from higher prices

Timing Entry Points

Given the seasonal patterns noted by Deutsche Bank, investors might consider whether fourth-quarter weakness could present more favorable entry points for establishing or adding to gold positions.

A strategic approach might include:

- Dollar-cost averaging into positions over time

- Increasing allocation during periods of price weakness

- Monitoring technical indicators for potential entry points

- Maintaining discipline regarding position sizing and portfolio balance

How Does This Forecast Compare to Historical Gold Performance?

Historical Context for $4,000 Gold

A $4,000 price target would represent a new paradigm for gold, which only crossed the $2,000 threshold relatively recently. When adjusted for inflation, however, gold’s 1980 peak would equate to approximately $3,500 in today’s dollars, suggesting the metal is entering historically significant territory.

The progression of gold’s major price milestones shows the acceleration in recent years:

- $500/oz first reached: December 1979

- $1,000/oz first reached: March 2008

- $2,000/oz first reached: August 2020

- $3,000/oz first reached: March 2025

- $4,000/oz projected: 2026

Recent Price Acceleration

Gold’s price appreciation has accelerated notably in 2025, with the metal gaining approximately 40% year-to-date. This rapid ascent follows years of consolidation and suggests a potential regime change in how investors value the precious metal.

The current rally has been characterized by:

- Steady upward momentum with limited pullbacks

- Broad participation across investor categories

- Support from both investment and central bank demand

- Muted response to traditional headwinds like rising interest rates

What Broader Economic Signals Does This Send?

Inflation Expectations

Gold’s strong performance and bullish forecasts may reflect persistent concerns about long-term inflation despite central bank efforts to control price increases. The metal has historically served as a record highs & inflation hedge during periods of currency debasement.

Current economic indicators present a mixed picture:

- Official inflation metrics have moderated from 2022-2023 peaks

- Core services inflation remains sticky in many economies

- Money supply growth has slowed but remains elevated by historical standards

- Labor market strength continues to support wage growth

Geopolitical Risk Premium

Rising gold prices often incorporate a premium for geopolitical uncertainty. Deutsche Bank’s elevated forecast may partially reflect expectations for continued or increased global tensions through 2026.

Gold tends to perform well during periods of:

- Regional conflicts and geopolitical instability

- Trade tensions between major economies

- Elections and political transitions

- Regulatory uncertainty affecting traditional assets

Monetary System Evolution

Central banks’ aggressive gold purchasing, particularly from nations seeking to reduce dollar dependence, signals ongoing evolution in the global monetary system. Deutsche Bank’s gold price forecast suggests this trend will continue to support gold prices.

Recent developments include:

- BRICS nations discussing alternatives to dollar-based trade

- Central bank digital currency development accelerating globally

- Growing calls for monetary system reform from various nations

- Increased scrutiny of reserve currency status and implications

Read the full article HERE.

Gold prices rose Tuesday, climbing to fresh record levels as investors remained confident of a U.S. Federal Reserve interest rate cut later this week.

At 08:15 ET (12:15 GMT), spot gold edged 0.4% higher to $3,693.97 per ounce, after hitting a record peak of $3,699.57 earlier in the session, and U.S. gold futures for December were up 0.3% to $3,730.92/oz.

Bullion jumped 1% in the previous session, surpassing record levels notched last week.

“Gold prices have surged more than 40% so far this year amid Trump’s aggressive trade policy, conflicts in the Middle East and Ukraine, and central bank buying,” said analysts at ING, in a note.

Gold scales fresh high on Fed easing bets

This rally was underpinned by widespread market belief that the Fed will deliver a 25-basis-point rate cut at the end of its September 16-17 meeting, its first since December 2024.

A weaker U.S. dollar, trading near one-week lows, added further support.

Political developments in Washington also bolstered metal’s safe-haven appeal.

The Senate confirmed Stephen Miran, Trump’s economic adviser, to the Fed Board of Governors. Investors viewed the appointment as a sign that the central bank could face even more pressure to align with White House policy.

Separately, a U.S. appeals court blocked President Donald Trump’s attempt to remove Fed Governor Lisa Cook, meaning she would likely attend this week’s Fed meeting. President Trump is expected to take the matter to the Supreme Court.

Commerzbank lifts gold price forecasts

Analysts at Commerzbank have lifted their forecast for gold prices by the end of the year, citing predictions for “slightly more” future Federal Reserve interest rate cuts than markets are currently pricing in.

In a note to clients, the analysts led by Carsten Fritsch said they now expect gold prices to stand at $3,600 per troy ounce this year and at $3,800 by the conclusion of 2026 — $200 more than their initial outlook, respectively.

Policymakers are tipped by Commerzbank to roll out 75 basis points of rate reductions over the rest of the year and a further 125 bps in cuts in 2026 — marginally above the level indicated by Fed Funds Futures. Interest rates now stand at a target range of 4.25% to 4.5%.

Copper retreats from 15-month peak

Elsewhere, Silver Futures were up 0.8% to $43.29 per ounce, while Platinum Futures gained 0.4% to $1,423.45.oz.

Benchmark Copper Futures on the London Metal Exchange fell 0.2% to $10,147.00 a ton, after hitting a 15-month high of $10,192 a ton in the previous session.

U.S. Comex Copper Futures fell 0.2% to $4.7085 a pound.

“Recent reports suggest that Chile expects production to grow this year and next, targeting a record 6 million tons by 2027, despite setbacks at two major mines (owned by Codelco and Teck Resources), offering some relief to a tight global market,” said ING.

U.S. and Chinese officials held a fresh round of trade talks in Madrid, led by Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer on the U.S. side, and Vice Premier He Lifeng and negotiator Li Chenggang for China.

The discussions produced a framework deal on shifting ownership of TikTok’s U.S. operations, with Presidents Donald Trump and Xi Jinping expected to speak later this week to confirm the terms.

Easing trade tensions between the two world’s largest economies could provide a boost to industrial metals.

Read the full article HERE.

A 39% price jump this year outpaces Covid-19 pandemic, 2007-09 recession

Kenneth Pack invested in gold for the first time in April to shield himself from what he saw as the disorder of the new Trump administration. The chaos trade was just heating up.

Even after the stock market recovered from Trump’s “Liberation Day” confusion and rose even higher, investors such as Pack have kept plowing money into the precious metal. The Nevada retiree plans to keep holding precious metals and stocks linked to them, which comprise 17% of his portfolio.

His reasons include the stop-and-start policy rollouts that have at times included several tariff changes in a day.

“Strangeness seems to be the new norm,” Pack said.

A modern-day gold rush is stretching from Costco store aisles to underground vaults in London to the flickering screens of Wall Street. Old jewelry now glimmers with potential dollar signs.

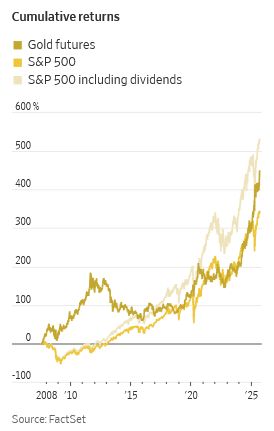

Gold’s value has ballooned by 39% this year, putting it on track for a greater annual price jump than during the depths of the Covid-19 pandemic or 2007-09 recession, according to Dow Jones Market Data. Futures for the precious metal haven’t surged so much in a year since 1979, when a global energy crisis fueled an inflationary shock that thrashed the world’s economy.

These days, it isn’t a financial meltdown that is drawing people to one of the original market refuges. The recent run-up to record prices—reaching $3,649.40 a troy ounce on Friday—instead stems in part from the White House, with investors big and small rushing to shield themselves from an uncertain outlook for the U.S. economy and its role in the world.

President Trump’s attempt to reorder global trade has buoyed inflation and scrambled economic forecasts. A White House pressure campaign against the Federal Reserve is threatening the independence of one of the financial system’s bulwarks. The U.S. dollar by one measure had its weakest first half of the year in more than five decades.

On top of it all, the president has made little progress in ending wars in Ukraine and elsewhere that have periodically upset markets.

“With Trump in the U.S. and [Vladimir] Putin in Russia, a lot of people think: Is this going to get worse?” said Sean Hoey, managing director of IBV International Vaults London.

Operating from a Victorian mansion just steps from Hyde Park, the company has recently seen a surge of wealthy customers hoping to stuff gold into the hundreds of safe-deposit boxes in its subterranean, steel-encased vault. IBV’s in-house trading arm buys gold from the Royal Mint and other certified sources, Hoey said, allowing clients to hold and sell the metal without it ever leaving the building.

“The majority of people right now are buying and thinking it’s going to go up more, rather than selling,” he said. IBV next year plans to roughly double the number of boxes it offers to keep up.

Gold’s run-up began almost three years ago, fueled by central banks and Chinese investors loading up on bullion.

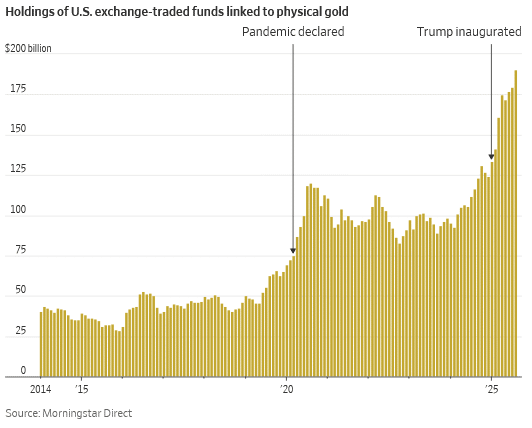

But Westerners have helped drive the rally this year in part by piling into exchange-traded funds. The net assets in U.S. ETFs linked to physical gold have ballooned 43% since January, according to Morningstar Direct, with March and April seeing two of the three-biggest monthly inflows since at least 2014.

Gold prices took another turn higher in August after Federal Reserve Chair Jerome Powell signaled the central bank would begin cutting interest rates at its meeting this week. Speculators piled in. In the short term, lower rates could make gold, which pays no interest, more appealing relative to safe government bonds.

Saxo Bank’s head of commodity strategy, Ole Hansen, said hedge funds by early September had parked 47% of their net commodity holdings in gold.

Lower rates could propel the precious metal in another way. Analysts warn that cutting rates in an economy with low unemployment and above-target inflation may also lead to longer-term price pressures that would erode profits and boost borrowing costs.

Investors’ ultimate fear is a mixture of high inflation and slow growth similar to what fueled gold prices’ meteoric 1979 rise.

“The risk of the s-word—stagflation—has increased,” said Aakash Doshi, head of gold strategy at State Street Investment Management. “That is a perfect environment for gold.”

Renewed confidence in U.S. growth and the dollar’s role as a reserve currency could tarnish the rally. But given trade tensions and America’s retrenchment from the world, Doshi said, “that seems very tenuous.”

Investors haven’t lost their appetite for risk in that new world—the AI-crazed stock market is at records—but instead are hedging their bets with investments not denominated in weakening dollars.

“Trump has been positive for gold,” he added.

On Main Street, where surveys show consumers are increasingly downbeat, more Americans are now handing over their gold to jewelry stores or repair shops to be melted down and sold.

“The value is not in the artistry,” said Lark E. Mason Jr., an appraiser based in Texas and New York. “It’s in the material.”

Even the Trump family has gotten in on the action. Donald Trump Jr., whose father has redecorated the Oval Office with golden flourishes, has in recent months appeared in online ads for a company that helps customers convert retirement accounts into gold.

Advising viewers to reach out for a free consultation, he said in an ad shared on Instagram, “What do you have to lose?”

Read the full article HERE.