When the yield curve turns positive, the country is usually about to plunge into recession. Hope this time relies on a few historical exceptions.

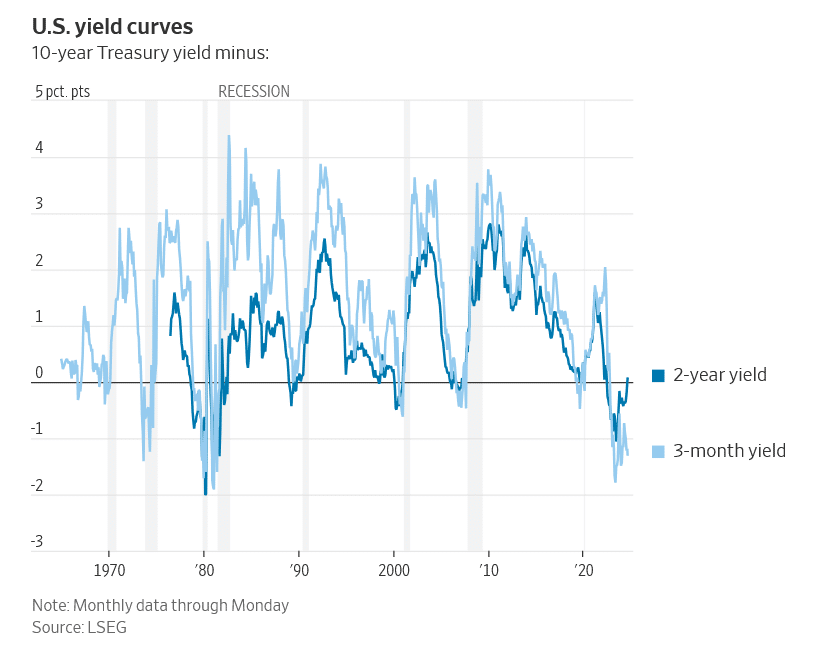

Two years ago, the inversion of the yield curve—shorter-dated Treasurys yielding more than longer-dated bonds—was taken by investors as a surefire sign of recession. Now Wall Street worriers have a new concern: The yield curve is back to normal, a surefire sign of recession.

It might seem odd, but both yield-curve moves are indeed good signs of recession, though not foolproof ones. What really matters is why Treasurys move as they do, and in this case it comes down to the Federal Reserve.

The Fed is expected to embark on a series of interest-rate cuts starting next week, which is why short-dated bond yields have fallen fast, uninverting the yield curve when measured as the 10-year minus two-year yield. If those cuts are purely because inflation has dropped back close to target, that is the ideal of a soft landing for the economy, and absolutely not a sign of imminent recession.

But for most of modern history, deep rate cuts by the Fed have been a sign that the country is about to plunge into recession, or is already in one that economists missed.

The yield curve is rather a crude representation of this problem. The inversion of the past two years tells us that investors thought the Fed had rates temporarily high and they would be lower in the long run. It doesn’t tell us why.

Look at recent market action and you see investors are vacillating between the reasons for rate cuts. Some days they think a weaker economy, particularly a weaker jobs market, will push the Fed to try to boost growth with rate cuts. That is bad news for stocks, because weaker growth might turn into a recession.

Other days, they think growth is fine but lower inflation will allow the Fed to cut rates anyway. That is good for stocks, because it means cheaper financing combined with decent after-inflation profits.

History tells us that in the past when the Fed raised rates a lot, it almost always caused a recession. History also tells us that when the Fed embarked on a big series of rate cuts, it was almost always because of a recession.

The combination gives us the oddity that inverted yields curves appear to predict recession, since they typically result from the Fed raising rates a lot, and uninverting yield curves appear to predict recession since they typically result from the Fed cutting rates a lot. At the moment, futures traders are pricing in 2.5 percentage points or more of rate cuts by the end of next year, which is a lot to cut without a recession.

Hope this time rests on the historical exceptions. There were soft landings in the mid-1960s, mid-1980s and mid-1990s despite big rate rises. In the mid-1960s and very briefly in the mid-1990s, at least some measures of the yield curve inverted, although nowhere near as long or as deeply as in the past couple of years. In the mid-1980s, there was a soft landing without an inverted yield curve after big rate rises turned into rate cuts as large as the markets are predicting by the end of next year.

There is also the question of which yield curve to choose. Economists prefer to compare the 10-year yield with the three-month yield, which captures only impending rate cuts and has a better track record than the two-year used by many investors. The 10-year minus three-month curve is still a long way from uninverting, confusing the picture still further.

None of the historical examples involved both an inverted curve and such rapid predicted cuts. This is where the market might have things wrong. There are good reasons to think investors might be overdoing it in pricing in such deep cuts combined with a soft landing, given the upward pressures on long-term rates from huge and apparently permanent fiscal deficits, increased protectionism and the need for higher defense and energy spending globally.

Yet, if inflation stabilizes close to the Fed’s 2% target, interest rates of 3% are perfectly conceivable for a while. Which takes us back to the deep problem that investors have to wrestle with. Is the slowdown in the economy the start of a slide into recession or a return to normal after the bust-boom cycle of the pandemic?

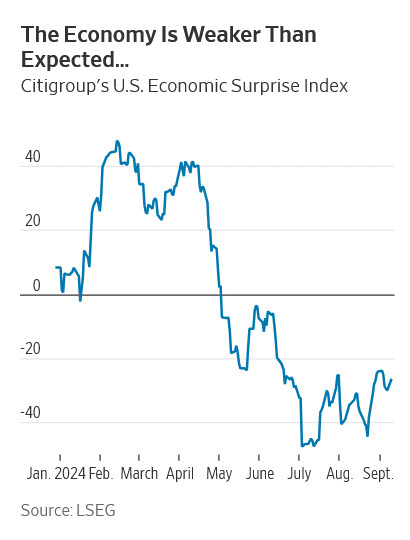

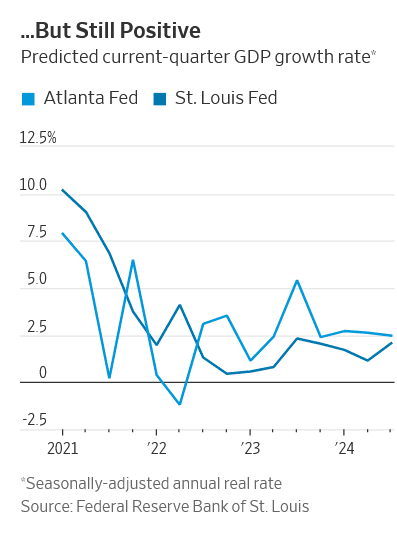

The economic data have undoubtedly been disappointing, but on the plus side they don’t suggest the economy is in trouble at the moment.

Unfortunately, if a recession is on the way, even quite aggressive rate cuts might not stop it. True, higher rates have held back some corporate investment, hit poorer and younger borrowers and made it more difficult for indebted businesses when fixed-rate debt matures.

But the economy as a whole is much less sensitive to rates than it used to be because so much debt is fixed at low rates for long periods, both for mortgages and big companies. Companies have been pouring money into building new factories despite the Fed thanks to government subsidies. And rate cuts take time to affect the economy anyway.

Investors should be careful about taking too much from the yield curve. Right now it tells us what we already know—that the Fed is about to cut rates—without telling us what we really want to know: whether a recession is imminent.

Read the Full Article HERE.