Wall Street veterans used to tell their underlings, and their clients as well, that the bond market is a daily referendum for the government. It is facing competition now.

Decisions on taxes, spending, and broader economic policy get baked into Treasury bond prices, and then reflected in yields, almost instantaneously. Government borrowing costs can rise and fall based on those movements, making the bond market’s daily assessment of policy impossible to ignore.

That is still largely the case. Politicians tend not to dismiss fixed-income markets when they start to signal concern, but the recent vintage of bond vigilantes wields significantly less influence.

That has left gold to act as the new canary in the financial market’s coal mine.

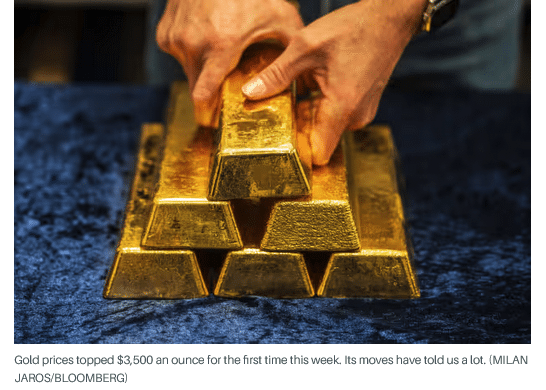

Bullion prices have risen nearly 38% so far this year, topping $3,500 an ounce for the first time this week. The U.S. dollar, meanwhile, suffered its worst first-half performance in five decades. It remains pinned near the lowest levels in three years relative to a basket of its global peers.

Gold was also the best-performing asset over the month of August, according to Bank of America data. It rose about 3.95% as uncertainty about tariffs, data showing inflation is worsening, and President Donald Trump’s effort to remove Federal Reserve governor Lisa Cook rattled investors.

“The latest leg higher [in gold prices] reflects a potent mix of renewed rate cut expectations, mounting concerns over Fed independence, and a fragmenting world order that is reshaping flows across safe-haven assets,” said Ole Hansen, head of commodity strategy at Saxo Bank.

As a haven asset, gold has its issues. It doesn’t pay interest, carries costs associated with storage, and can sometimes be difficult to liquidate on short notice. It has also been subject to recent confusion regarding tariffs.

But gold has been extremely useful in articulating the market’s crucial macroeconomic tension: that Trump’s tariffs will both blunt growth prospects and stoke consumer-price pressures. Meanwhile, his relentless attacks on the Fed could lead to artificially low interest rates that expose longer-dated bonds to increased inflation risks.

“For many investors, long-dated bonds no longer serve as the default defensive allocation, opening the door for gold to capture a larger share of safe-haven demand alongside other tangible assets such as silver and platinum, both supported by constrained supply outlooks,” Hansen said.

Silver prices, which rose past $4o an ounce for the first time since 2011 this week, were at $41.46 late on Wednesday. That extends the metal’s year-to-date advance to around 42%.

Gold is also getting a tailwind from buying by central banks. Those purchases have risen at a record pace over the past three years, led by China’s effort to diversify its foreign-currency holdings away from the U.S. dollar.

The People’s Bank of China has added 21 metric tons of gold to its reserves this year, based on calculations from Reuters, taking its overall total to just over 2,300 tons.

Tariffs have also slowed global trade, leaving foreign countries without the dollars they would normally earn from selling goods into the U.S. Those dollars were often recycled into U.S. Treasury bonds, but that process appears to be unraveling.

Crescat Capital’s macro strategist Otavio Costa notes that global central bank gold holdings represent 27% of their overall reserves, the highest in nearly 30 years. Foreign holdings of U.S. Treasuries, meanwhile, have fallen to around 23%, the lowest since the 2008-2009 financial crisis.

It is difficult to focus on the longer-term challenges posed by staggering levels of government debt, or a central bank at risk of coming under the sway of politics, when stocks continue to print all-time highs thanks to the artificial intelligence investment boom.

But gold’s recent rally, and the signals it echoes, shouldn’t be dismissed as merely an inflation warning. It is a signal that the U.S. is at risk of losing its role at the center of the financial system as doubts rise about the dollar’s long-term value.

Read the full article HERE.