- Air travel, taxpayer services and national parks are among the first government functions to feel the strain of a prolonged impasse, with some agencies implementing a sort of rolling blackout of services to conserve funds and respond only to emergencies.

- More than a quarter million federal employees missed scheduled paychecks this week, with another 2 million expected to go without by next week, and the Pentagon’s next military payday could prove a political flash point if troops begin missing pay for the first time in decades.

- Economists estimate that the shutdown could shave 0.1 to 0.2 percentage points off gross domestic product for each week it continues, with the impact magnified because the government’s data flow has largely gone dark.

The first week of a government shutdown is usually the easy one. It only gets harder after that. As the standoff between President Donald Trump and Congress stretches into its second week — and with no end in sight — the real-world impacts of the shutdown are starting to rise.

Air travel, taxpayer services and national parks are among the first government functions to feel the strain of a prolonged impasse, and some agencies have implemented a sort of rolling blackout of services to conserve funds and respond only to emergencies.

More than a quarter million federal employees missed scheduled paychecks this week, with another 2 million expected to go without by next week. The Pentagon’s next military payday, Oct. 15, could prove a political flash point if troops begin missing pay for the first time in decades.

Early Pain Points

Air travel is emerging as the most visible strain. Flight delays linked to air-traffic-control staffing shortfalls have hit airports from Dallas to Chicago to Washington, DC.

Transportation Secretary Sean Duffy said staffing shortages usually account for about 5% of delays, as air traffic controllers slow traffic to ensure safety. Now those shortages are the cause of more than half of late flights. The US Travel Association estimates $1 billion in lost spending each week.

Taxpayer services are contracting after the IRS furloughed nearly half its staff when carryover funds ran out. Roughly 34,000 employees were sent home this week, while about 40,000 remain on duty preparing for next year’s filing season and implementing Trump’s new tax law. The Taxpayer Advocate Service has shut down entirely.

Food programs could be next in line. The $8 billion Women, Infants and Children nutrition program is being sustained by a $150 million contingency fund that’s nearly gone. The White House has said tariff revenue will be tapped to keep it afloat, but hasn’t explained how or when those transfers would occur. Supplemental Nutrition Assistance Program benefits — food stamps for 41 million Americans — are funded through the end of October.

Some national parks are open but with bare-bones staffing and limited sanitation services, with the impact varying state by state. Cooperative agreements with state governments can keep some parks open using non-federal funds, but others will be closed completely. Smithsonian museums and the National Zoo will close Oct. 11.

Homeowners in flood-prone areas may find themselves without coverage during hurricane season because of a lapse in the National Flood Insurance Program, which cannot issue new policies or renew expiring ones.

A Dynamic Shutdown

After a 35-day holiday shutdown stretching into 2019, the Government Accountability Office faulted the Trump administration for failing to plan for a prolonged lapse in funding.

Some workers are being furloughed and recalled as needed to balance conflicting mandates. The law forbids agencies from spending money not approved by Congress, but the lack of funding doesn’t always delay legal deadlines or prevent emergencies.

So Justice Department lawyers are furloughed as long as their court cases are on hold — but are being called back in cases where judges are declining continuances. And IRS workers could be called back as the tax filing season nears.

Some agencies were able to get around the Antideficiency Act by using special funds that didn’t expire at the end of last year. But those funds are being quickly depleted.

At the Environmental Protection Agency, some furlough notices went out starting Wednesday night, according to the agency’s largest union. EPA’s contingency plan calls for almost 90% of employees to be furloughed once funds lapse, halting most enforcement and permitting.

More so than during previous shutdowns, the second Trump administration is also rewriting the playbook based on new legal interpretations. The Department of Homeland Security anticipated a prolonged lapse and had plans to bring back almost 1,800 workers for the second week — mostly in top-level management, Coast Guard and Customs and Border Protection.

Economic Fallout

Economists estimate that the shutdown could shave 0.1 to 0.2 percentage points off gross domestic product for each week it continues. The impact is magnified this time because the government’s data flow has largely gone dark.

The Bureau of Labor Statistics postponed last week’s jobs report, but it brought back staff in order to prepare the latest consumer price index. Other reports at risk of being delayed include retail sales, housing starts and business inventories from the Census Bureau. The Bureau of Economic Analysis has suspended operations in advance of its initial third-quarter GDP estimate for Oct. 30. Without those data, the Federal Reserve and private forecasters are flying blind.

Those official data are particularly important for annual inflation adjustments throughout the federal government, including cost-of-living increases, tax brackets, loan subsidies and cost-benefit analyses of federal programs.

Some of the economic impact could be blunted once the shutdown ends as federal workers get back pay. But Trump has called into question whether all federal workers will be made whole, and has threatened to lay off thousands of federal employees, making the rebound less certain.

Political Pressure Mounts

Historically, the mounting pain for travelers, taxpayers and troops has provided the impetus for Congress to break the stalemate and approve new funding. In 2019, airport chaos forced the White House to cut a deal after 35 days.

This time, Trump and his Republican allies think they have the upper hand. The administration has tried to increase the pain among Democratic constituencies — threatening to fire thousands of federal workers who live and work in Democratic districts — while maintaining funding for key Republican priorities like immigration enforcement.

Those mass layoffs — which the White House said last week would happen in “two days, imminent, very soon” — haven’t materialized. If they do, the downsizing could put added stress on agencies that have already seen staff cuts inspired by Elon Musk’s Department of Government Efficiency initiative earlier this year.

Read the full article HERE.

Key Points

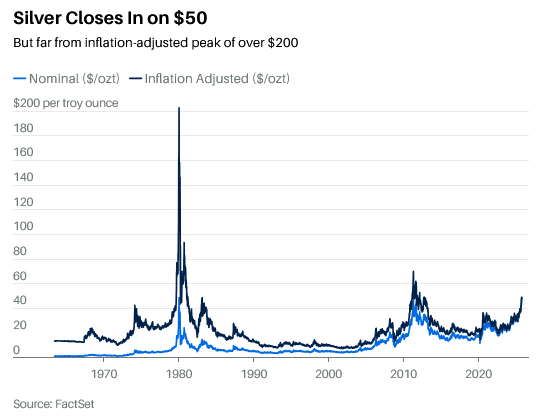

- Silver reached a record high of $48.994, exceeding $49 intraday, and has gained 67.55% this year, outpacing gold’s 54.13% rise.

- The increase in silver prices is driven by booming industrial demand for applications in solar panels and artificial intelligence semiconductors.

- A smaller market size compared to gold means dollar fluctuations have a larger percentage impact on silver, potentially boosting prices if the dollar falls.

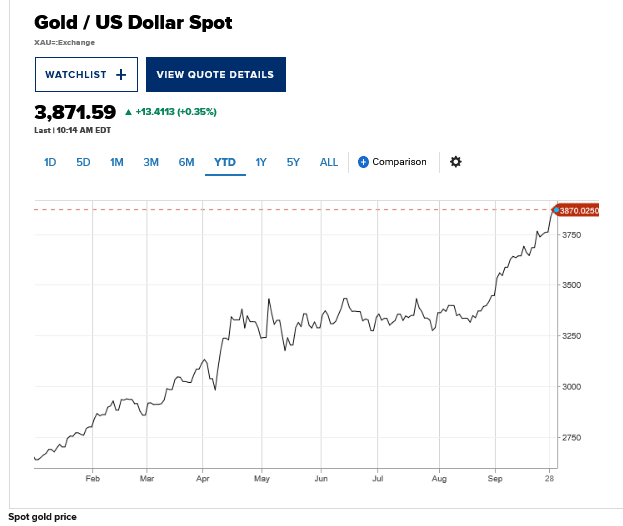

Silver is right at the cusp of touching $50 a troy ounce for the first time since 2011. It has risen in the shadow of gold’s GC00-1.98% rally—but at a faster pace.

Most active silver settled at a record high of $48.994 on Wednesday after officially exceeding $49 during intraday trading, a level last surpassed 14 years ago. The price of silver is paltry when compared with gold’s price of $4,070.50, but the white metal has risen by 67.55% this year so far, or 13.42% more than gold’s 54.13% gain.

Such an outperformance hasn’t been seen in 15 years, according to Dow Jones Market Data team. It’s the biggest year-to-date increase for silver since 1979.

Most other major metals, besides platinum, can’t beat silver’s gain this year. Its rise is rooted in booming industrial demand. Silver is used in everything from solar panels to semiconductors linked to artificial intelligence. There is also a trickle-down of safe-haven money: Investors who see the gold trade as too crowded are looking into silver.

“The bull market in gold has now spread to silver, platinum and palladium, and it even seems to be leaking into copper,” wrote Louis-Vincent Gave, founding partner and CEO of Gavekal Research, in a report last week. “Once a bull market in precious metals gets under way, it usually takes a hawkish Federal Reserve, a hawkish People’s Bank of China, or a sharp rise in the US dollar for the bull market to stop. Right now, none of these developments seems to be in the cards.”

Finding drivers that can pull silver prices down is difficult because the world seems increasingly fragmented. Metals like silver, unlike stocks and bonds, are offering investors a sense of safety and promise to protect cash from inflation erosion.

Silver could go further up if the dollar falls further in value since it spurs more international buying. Silver is globally priced and traded in dollars. The market for silver is significantly smaller than the over $25 trillion gold market, which means a move in the dollar has a bigger impact on silver on a percentage basis than gold. Rising inflation can also support demand for real assets like silver.

“In our view, for the silver price to keep rising, there would need to be severe demand destruction in lower economic value-added end uses for silver, like photography and silverware. Meanwhile, there would need to be a growing demand for higher economic end uses, such as electrical and electronic demand from AI-related spending, photovoltaics and other technology-related demand,” wrote Paul Wong, market strategist at Sprott Asset Management.

To be sure, gold prices are getting support from global central banks buying the metal for their reserves, while no sovereign entity views silver as a neutral reserve asset.

But if silver still manages to trade above $50 sustainably, “it could be a sign that silver’s economic worth and store of value function was being re-evaluated, or it could be a mark-to-market reality repricing of the metal,” Wong writes.

HSBC, in a note this week, said it expects prices to go as far as $53 this year and as high as $55 next year, but decline in the back half of 2026.

Part of the rise will come from gold, which often exerts a “strong gravitational pull on silver” possibly as a result of buying by “investors who have not taken full advantage of the gold rally,” wrote James Steel, HSBC’s chief precious metals analyst.

Read the full article HERE.

Gold — typically a safe-haven in times of turmoil — is soaring at the same time the stock market is hitting new highs, an unusual dynamic that is troubling some market insiders.

Why it matters: The rally in gold reflects investors’ desire to diversify away from dollar-denominated assets as trust in the U.S. slowly erodes, they say.

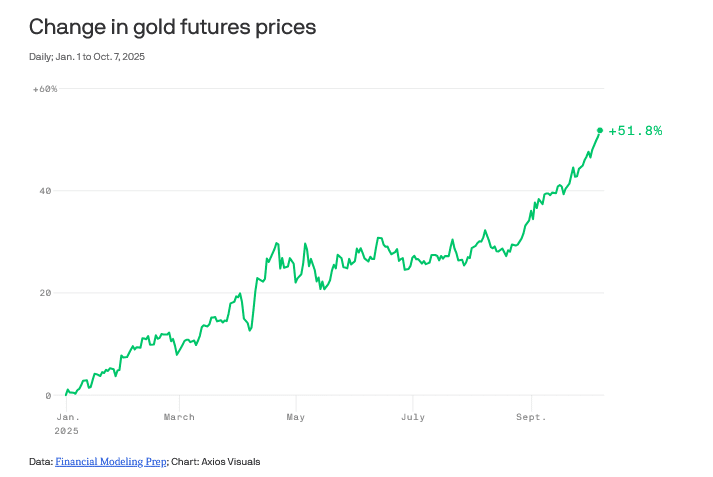

Driving the news: Gold futures on Tuesday topped a record high of over $4,000 an ounce for the first time, putting the precious metal on track for its best year since 1979 — a year of double-digit inflation, a Mideast oil crisis and the Soviet invasion of Afghanistan. So far this year, the price of gold is up 51%.

What they’re saying: “People are willing to go long U.S. enterprise, and they want to short the mess,” Mohamed El-Erian, the former CEO of the asset manager Pimco and current president of Queen’s College, Cambridge, tells Axios.

- “People are starting to lose trust in institutions,” says Ryan McIntrye, a senior managing partner at Sprott, which focuses on precious metals, adding that gold’s rally comes as people are “reassessing what they view as safe.”

- Gold’s rally comes amid President Trump’s trade war and, now, a government shutdown.

- “For the rest of the world, we’re weaponizing the tools of economic policy,” El-Erian says. The concern is that slowly, over time, the rally in gold starts to indicate an eroding belief in “what makes the U.S. special,” he adds.

Between the lines: While gold and U.S. stocks are surging, the U.S. dollar is down over 9% against a basket of other currencies so far this year.

- That indicates that investors want exposure to corporate America’s resilience, but they don’t want what Citadel CEO Ken Griffin called “sovereign risk” in an interview with Bloomberg.

- That flight to gold to try to “de-dollarize” is concerning, Griffin said, given what it says about sentiment around the the U.S. dollar, the world’s global reserve currency.

Follow the money: What else is powering the gold rally?

- Central banks: Other countries’ central banks are looking to diversify their reserves after overallocating to the U.S. dollar. These banks “have enormous buying ability,” El-Erian notes.

- Speculation: As central banks buy gold, pushing up the price, speculators come in, adding fuel to the rally.

- Weak competition: Once, there was no alternative to U.S. Treasuries for investors seeking safety, Now, “there’s no alternative to gold,” McIntyre says.

- Uncertainty: Concerns about a possible resurgence in inflation, the debt load of the U.S., and economic and policy uncertainty are all risks that are driving people to look “outside the financial system” for assets like bitcoin and gold, which aren’t tied to fiat currencies like the dollar.

Yes, but: “I wouldn’t call it strict de-dollarization,” Jay Barry, managing director and global rates strategist at JPMorgan, tells Axios.

- Barry notes continued high demand from foreign banks for U.S. Treasuries, which would not indicate any unease about the dollar.

What we’re watching: Whether the Trump administration starts to consider the rally in gold amid the decline of the dollar as a potential risk.

Read the full article HERE.

- Gold futures broke above $4,000 per ounce on Tuesday for the first time.

- The precious metal has soared this year as investors seek a safe haven from a weaker dollar and geopolitical and economic uncertainty.

Gold prices hit $4,000 for the first time Tuesday as investors seek a safe haven from geopolitical volatility, economic uncertainty and stubborn inflation.

Gold futures were last trading at $4,005.80 per ounce. Prices have gained more than 50% this year as President Donald Trump upends the global trade system and threatens the independence of the Federal Reserve.

Central banks and retail investors are buying gold at a strong clip. Countries like China are diversifying away from U.S. Treasurys and into gold after Washington imposed stiff sanctions on Russia over its invasion of Ukraine. Retail investors, meanwhile, are looking for protection against inflation.

The precious metal has recently taken a leg higher after the Fed cut interest rates in September, making debt instruments like bonds less attractive to investors. The market is expecting two more rate cuts this year.

Ray Dalio, founder of Bridgewater Associates, recommended Tuesday that investors put “something like 15% of your portfolio in gold.” Debt instruments are “not an effective store of wealth,” Dalio said at the Greenwich Economic Forum in Connecticut.

Gold is “the one asset that does very well when the typical parts of your portfolio go down,” he said.

Bank of America urged investors on Monday to approach gold cautiously as prices were heading toward $4,000. BofA warned clients that gold faces “uptrend exhaustion,” which could lead to “a consolidation or correction” in the fourth quarter.

Read the full article HERE.

(Reuters) -Gold prices touched an all-time high on Monday, soaring above the $3,900-per-ounce level, as investors flocked to safe-haven bullion amid the U.S. government shutdown, broader economic uncertainty, and prospects of further Federal Reserve rate cuts.

Spot gold was up 1.4% at $3,940.04 per ounce, as of 1108 GMT, after hitting $3,949.34 earlier in the session.

U.S. gold futures for December delivery climbed 1.4% to $3,964.50.

Washington will start mass layoffs of federal workers if U.S. President Donald Trump decides negotiations with congressional Democrats to end a partial government shutdown are “absolutely going nowhere,” a senior White House official said on Sunday.

“Appetite for gold remains heavily stimulated by the ongoing U.S. government shutdown,” said Lukman Otunuga, senior research analyst at FXTM.

“There may be some FOMO buying on the current price but for others there is likely a sense that this particular financial lifeboat has sailed,” said independent analyst Ross Norman.

Gold has climbed nearly 50% so far this year, underpinned by strong central bank buying, increased demand for gold-backed exchange-traded funds, a weaker dollar and growing interest from retail investors seeking a hedge amid rising trade and geopolitical tensions.

This rally, characterised by low participation and primarily driven by central banks with a long-term outlook and steady investors rather than speculative buyers, indicates that any pullback might be milder than expected, Norman said, adding that this could present a buying opportunity on dips while the rally maintains its momentum.

Alternative data from both public and private sources indicate signs of weakness in the U.S. labor market amid the government shutdown.

Investors are now pricing in a 25-basis-point cut at the Fed meeting this month, with an additional 25 bp cut anticipated in December. [FEDWATCH]

“We see both fundamental and momentum-based reasons for gold to rally further, and now expect bullion to reach $4,200/oz by the end of this year,” UBS said in a note.

Non-yielding gold thrives in a low-interest-rate environment and during economic uncertainties.

Spot gold broke the $3,000-per-ounce level for the first time in March.

Many brokerages have turned bullish on the rally.

Spot silver climbed 1.2% to $48.53 per ounce, hitting its highest level in more than 14 years. Platinum rose 0.6% to $1,615.45 and palladium gained 1.6% to $1,280.75.

Read the full article HERE.

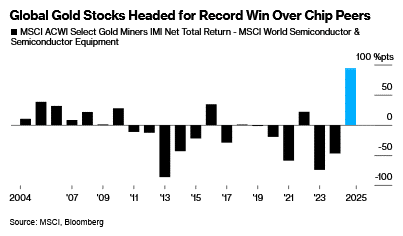

- A gauge of the world’s gold equities from MSCI Inc. has soared about 135% this year, tracking gains in the precious metal.

- Gold itself has soared more than 45% this year, touching a series of new all-time highs and on track for its best year since 1979.

- The MSCI gold miner index trades at 13 times forward earnings estimates, slightly below its average for the last five years.

For all the hype over artificial intelligence and the surge in chip stocks this year, gold miners have actually been the better buy.

A gauge of the world’s gold equities from MSCI Inc. has soared about 135% this year, tracking gains in the precious metal. It’s on course for its greatest-ever outperformance versus the index compiler’s measure of major global semiconductor firms, which is up 40%.

The surprisingly large gap underscores a key dynamic in this year’s global markets: Even as a sense of FOMO drives investors to chase gains in anything related to AI, they are also lured by the relentless rally in gold as central banks around the world accumulate the metal.

“Gold and gold miners are one of my most bullish medium thematic calls,” said Anna Wu, a cross-asset investment strategist at Van Eck Associates Corp. in Sydney. Gold has safe haven appeal, “while gold miners are also set to benefit from margin expansion and valuation re-rating.”

Gold itself has soared more than 45% this year, touching a series of new all-time highs and on track for its best year since 1979. In addition to central bank buying, the metal has also been supported by Federal Reserve rate cuts, the trend of de-dollarization and rising holdings in gold-backed exchange-traded funds.

Among the heavyweights in MSCI’s gold miners index, Newmont Corp. and Agnico Eagle Mines Ltd. have seen their New York-listed stocks more than double in 2025. Zijin Mining Group Co.’s shares have jumped more than 130% in Hong Kong, outpacing gains in China’s AI darling Alibaba Group Holding Ltd. And London-listed gold and silver miner Fresnillo Plc has almost quadrupled, making the stock by far the best performer in the benchmark FTSE 100 Index.

Moreover, valuations are much less of a concern for the precious metals sector than they are for tech. The MSCI gold miner index trades at 13 times forward earnings estimates, slightly below its average for the last five years. In contrast, the chip gauge is at 29 times, well above its five-year average.

“Even after a near-vertical move in the yellow metal, miners’ multiples look undemanding because earnings have run faster than prices,” said Charu Chanana, chief investment strategist at Saxo Markets in Singapore. “If gold stays near record territory, the cash-flow math still argues for elevated margins.”

Read the full article HERE.

Gold prices hovered near record highs Thursday as haven demand remained underpinned by an ongoing U.S. government shutdown and growing conviction in more interest rate cuts.

At 07:55 ET (11:55 GMT), Spot gold gained 0.5% to $3,885.19 an ounce, and gold futures for December rose 0.3% to $3,909.70/oz. Spot prices hit a record high of $3,895.33 on Wednesday.

The yellow metal has hit a series of peaks this week as the U.S. government shut down after Congress failed to pass a spending bill. The shutdown will delay the release of key labor market data this week, leaving markets in the dark over the path of interest rates.

U.S. government shutdown helps haven demand

The U.S. government is expected to remain shut for a prolonged period, disrupting several federal operations across the country, with Senate lawmakers making little progress towards reaching consensus on a spending bill.

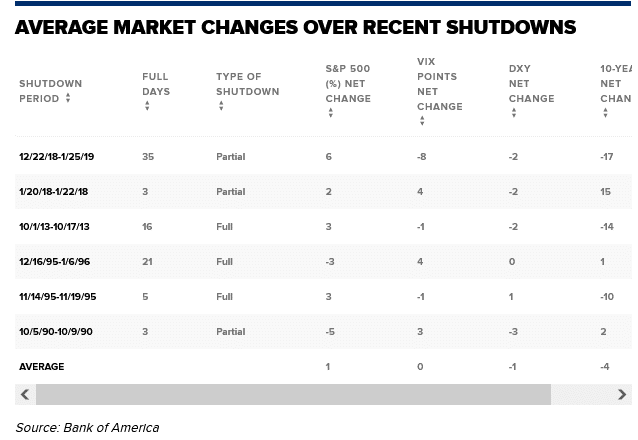

The 19 partial or full government shutdowns over the past 50 years have gone on for an average of about eight days, according to analysts at Canaccord Genuity.

A prolonged shutdown could hurt the U.S. economy with disruptions in essential services. President Donald Trump’s threats of firing more federal workers also stand to further hurt the labor sector.

Oxford Economics estimated that a partial government shutdown reduces economic growth by between 0.1 and 0.2 percentage points per week.

Other precious metals have put in strong performances this week. Spot platinum gained 1.7% to $1,618.35/oz, while spot silver fell 0.2% to $47.55/oz. Both metals crested over 10-year highs this week.

Among industrial metals, benchmark copper futures on the London Metal Exchange rose 1.1% to $10,492.55 a ton, while COMEX copper futures rose 1.6% to $4.9600 a pound.

Markets see 97% chance of October rate cut

Markets are pricing in a 97% chance for a 25 basis point cut by the Fed in late-October, and a 3% chance for a bigger, 50 bps cut, CME Fedwatch showed.

A slew of recent readings showed the U.S. economy was steadily cooling, with particular weakness in the once strong labor market. The Fed had cut rates by 25 bps in September on concerns over cooling jobs growth.

A slew of Fed officials warned that sticky inflation could deter the central bank from cutting rates further. PCE price index data– the Fed’s preferred inflation gauge– rose as expected in August, with core inflation remaining above the central bank’s 2% annual target, data showed last week.

But private payrolls data released on Wednesday showed a further cooling in the labor market, keeping markets largely optimistic over more interest rate cuts by the Federal Reserve. This notion weighed on the dollar and benefited metal markets.

Closely-watched nonfarm payrolls data, which was initially scheduled to be released this Friday, is now expected to be delayed until at least next week.

Read the full article HERE.

- The timing of the U.S. government shutdown is critical as key jobs data will be delayed by the shutdown.

- Amid the uncertainty, risk assets lost ground, while gold continued its bumper rally.

- Strategist Michael Field told CNBC the U.S. government shutdown was “just the straw that broke the camel’s back.”

Gold prices soared to new highs on Wednesday, as the U.S. government entered its first shutdown in almost seven years after lawmakers failed to reach a deal on government funding.

Spot gold hit a record of $3,894.63 an ounce, while U.S. gold futures for December delivery extended gains to hit a high of $3,922.70.

While the impact of government shutdowns on markets is usually minimal, the timing of this one is significant. Critical U.S. jobs data due to be published on Friday will be delayed, clouding the outlook for the Federal Reserve just weeks ahead of its next meeting. President Donald Trump has also threatened to use the shutdown to cut “a lot” of federal employees, who are ordinarily furloughed during a shutdown and brought back to work once it ends.

With no clear path toward a deal, it’s also unclear how long the shutdown will last. During Trump’s first term in office, a 34-day partial shutdown took hold — the longest in history.

Amid the uncertainty, risk assets lost ground, while gold — typically viewed as a safe haven asset in times of economic or geopolitical turbulence — continued its bumper rally to hit its 39th record high this year.

$4,000 gold?

“Gold’s status as a safe haven is well publicized, but the inexorable rise in the gold price over the last few years has been truly astounding, with the metal hitting fresh highs today,” Michael Field, chief equity strategist at Morningstar, told CNBC in an email on Wednesday.

While he noted that the driver behind Wednesday’s rally was the U.S. government shutdown, Field argued that it was “just the straw that broke the camel’s back.”

“Two major ongoing conflicts, political instability in France, newly announced tariffs, all of this is combining to create a very unstable picture for investors,” he said. “And when the going gets tough, gold gets a boost.”

Philippe Gijsels, chief strategy officer at BNP Paribas Fortis, has long held the view that gold can cross the $4,000 mark — and he now believes the metal can go even higher.

“Gold is fast closing in on the 4000 target that we put forward … about a year and a half ago,” he said. “Back then, the move was solely driven by central bank buying while investors were net sellers of the yellow metal, [but] since the beginning of the year, investors have come on board which has clearly accelerated the move to the upside.”

He argued that amid ongoing uncertainty and volatility, and an environment of sticky inflation across the globe, investors were broadly taking the view that they should diversify away from the classic 60/40 portfolio strategy “with hard assets” like gold.

“Still, we are still very early in the game as gold, and gold related investments are barely 2% of an average investment portfolio worldwide,” Gijsels added. “To say it in baseball terms, we are only in the second or third inning. $4,000 [will not be] the endpoint — just the start of the strongest bull market in precious metals the world has ever seen.”

In a note to clients on Wednesday morning, UBS Strategist Joni Teves also argued that gold remains under-owned.

“We expect gold’s bull run to continue over the coming quarters, driven by rising investor positions and a continued broadening in gold’s investor base. With the Fed easing cycle under way, dollar weakness and declining real rates should be bullish for the gold price,” she said.

Teves noted that UBS expected the rally to taper off toward the end of 2026, in anticipation of the end of the Fed’s easing cycle and improving economic conditions.

“That said, given the structural shift in gold’s role to becoming a core part of strategic asset allocations, we expect the correction to ultimately be contained and for prices to stabilise at historically higher levels over the long run,” she added.

Read the full article HERE.

Key Points

- A potential government shutdown could delay the September jobs report, complicating Federal Reserve monetary policy decisions.

- Economists estimate a shutdown could increase the unemployment rate by 0.1 to 0.2 percentage points and reduce fourth-quarter GDP growth by 0.1 to 0.2 percentage points per week.

- Unlike previous shutdowns, this one could have a more extensive impact on economic data releases because appropriations bills have been enacted for fewer agencies.

Government shutdowns are rarely big enough events to cause lasting damage to the U.S. economy. But that doesn’t mean the latest congressional impasse over spending couldn’t affect growth and monetary policy.

If congressional leaders can’t agree to pass even a short-term funding measure by 12.01 a.m. Eastern on Wednesday, the government will shut down. That deadline is particularly problematic for the publication of economic data, especially the jobs report for September, which is scheduled to be released by the Bureau of Labor Statistics on Friday. The last time a shutdown held back a jobs report was in October 2013.

Delays in that report and other data could create challenges for Federal Reserve officials. The bank is always reliant on economic statistics in making its calls on monetary policy, but the numbers are especially important now because the risks of higher inflation and a weakening job market are so closely balanced.

“An increasingly data dependent Federal Reserve with limited visibility into the September data increases the probability of an October pause,” writes Mike Reid, senior U.S. economist for the Royal Bank of Canada.

President Donald Trump is set to meet with congressional leaders on Monday afternoon, but BNP Paribas Securities senior economist Andrew Husby writes that the odds of a shutdown are “effectively a coin-flip” at this point. There are no indications about how long a shutdown might last.

While the longest U.S. federal government shutdown took place during Trump’s first term in office, starting in December 2018 and lasting 35 days, most are much shorter. Of the 20 government shutdowns since 1977, only seven have exceeded the average length of eight days.

Economic data continued to be published during the 2018-2019 shutdown because budgets for agencies including the Department of Labor had already been enacted. The disruption this time would be more “extensive” because Congress hasn’t passed appropriations bills for more agencies, write economists from the Wells Fargo Investment Institute.

“In the event of a federal government shutdown, the Bureau of Labor Statistics (BLS) will suspend data collection, processing, and dissemination,” an agency spokesperson told Barron’s via email on Monday. “Once funding is restored, BLS will resume normal operations and notify the public of any changes to the news release schedule on the BLS release calendar.”

The Metropolitan Area Employment and Unemployment release for August would be published on Wednesday as part of the agency’s shutdown process, it said.

The delay of economic releases would likely last slightly longer than the shutdown. A prolonged government closure could also jeopardize the Oct. 15 release of the latest consumer price index data and the September retail sales report from the U.S. Census Bureau.

If there is just a short, technical funding lapse that ends within a day, the September payroll report could still be released as scheduled, on the first Friday in October, Husby writes. When the government shut down for 16 days starting on Oct. 1, 2013, a Thursday, the BLS released the employment report on Oct. 22, he said. Husby only sees a “small likelihood” that a shutdown would last long enough to prevent the report’s release before the Federal Open Market Committee’s next meeting on Oct. 28-29.

If the BLS doesn’t publish its employment data on Friday, the ADP National Employment Report, scheduled for release on Wednesday, will likely gain outsize significance in the interim. The ADP report would be the only gauge of conditions in the broader labor market for September.

There are also potential implications for employment and growth. About 900,000 federal employees—about 40% of the workforce—would be furloughed if the government shuts down on Wednesday, estimate Goldman Sachs economists Alec Phillips and Ronnie Walker. Paychecks for all federal employees would be delayed until after Congress votes to restore funding or passes a continuing resolution, though in past government shutdowns, furloughed workers were still counted as employed in the monthly establishment survey.

Many government contractors, however, may be forced to simply go without pay for the duration of the shutdown with no reimbursement.

“The overall fiscal effect of a shutdown would be small, as benefit and interest payments would continue along with tax collections and other revenue functions,” the Goldman economists note. “That said, the administration has some flexibility in determining how to operate during a shutdown and could differ from the approach prior administrations have taken.”

Phillips and Walker expect that October payrolls will be largely unaffected, but that depending on the duration, the unemployment rate could be pushed up by 0.1 to 0.2 percentage points. If a shutdown does last more than a couple of weeks, other October economic data and releases could be affected as well.

Initial claims for unemployment benefits could also rise. And based on past shutdowns, Nomura’s chief economist, David Seif, calculates that there would be a drag of 0.1 to 0.2 percentage point per week on inflation-adjusted growth in gross domestic product for the fourth quarter.

In addition, Seif says, the Trump administration’s threat to lay off federal workers in the event of a shutdown could have a “more severe near-term impact” on public-sector employment in the October payroll data. Economists are already expecting a significant loss of public-sector jobs as a result of deferred resignations earlier in the year.

The Office of Management and Budget released a memo last week instructing agencies to prepare to permanently reduce their workforces. While those terminations would likely be challenged in the courts and some people would be rehired after the government reopened, the layoffs could make the situation look worse for the short term.

So while the U.S. economy is unlikely to falter in the midst of a shutdown, there are still consequences. The current complicated economic situation likely would become even more complex.

Read the full article HERE.

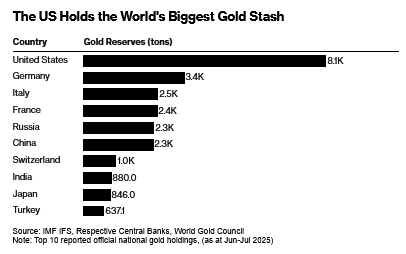

- The US Treasury’s gold reserves have surpassed $1 trillion in value as the precious metal breaks new all-time highs.

- The world’s biggest gold stash passed the milestone after prices rose above $3,824.50 an ounce on Monday, in a 45% rally this year.

- The official value of the gold reserves, based on the $42.22-an-ounce price set by Congress in 1973, is fixed at just over $11 billion.

The US Treasury’s gold reserves have surpassed $1 trillion in value — more than 90 times what’s stated on the government’s balance sheet — as the precious metal breaks new all-time highs.

The world’s biggest gold stash passed the milestone after prices rose above $3,824.50 an ounce on Monday, in a 45% rally this year. Its official value, however, based on the $42.22-an-ounce price set by Congress in 1973, is fixed at just over $11 billion.

Bullion has broken successive records this year as investors seek safety in the face of turbulence from trade wars, geopolitical tensions and growing concerns about a potential government funding crisis in the US. The rally has also been fueled by inflows into exchange-traded funds and the resumption of interest rate cuts by the Federal Reserve.

Earlier this year, an offhand comment from Treasury Secretary Scott Bessent sparked speculation that the government’s gold hoard would be marked to market, releasing a windfall of hundreds of billions of dollars. Bessent later dismissed the suggestion and Bloomberg reported that the idea isn’t under serious consideration.

Unlike most countries, the US’s gold is held by the government directly, rather than the central bank. The Fed instead holds gold certificates corresponding to the value of the Treasury’s holdings, and credits the government with dollars in return. That means that an update of the reserves’ value in line with today’s prices would unleash roughly $990 billion into the Treasury’s coffers.

That would cover about half of the $1.973 trillion total US budget gap for the fiscal year through August, a deficit level that was only surpassed in 2020 and 2021, a senior Treasury official said when the numbers were released earlier this month.

While it might seem tempting to change the way gold reserves are booked given the government’s debt-ceiling constraints, it would have far-reaching implications for the financial system, boosting liquidity and prolonging the Fed’s balance-sheet unwind.

The US would not be the first country to do so, though. Germany, Italy and South Africa all have taken the decision to revalue their reserves in recent decades, as an August note from an economist at the Federal Reserve noted.

Just over half of the US gold reserves are held in deep storage in a vault beside the US Army base of Fort Knox, Kentucky, where gold was transferred from New York and Philadelphia in the 1930s, in part to make it less vulnerable to foreign military attacks via the Atlantic. The rest is spread between depositories in West Point, Denver, and a vault 80 feet (24 meters) below the Fed’s building in lower Manhattan

The US gold hoard totals about 261.5 million ounces, according to Treasury data.

Conspiracy theories circulated in February, encouraged by comments by President Donald Trump and billionaire Elon Musk, that the gold held in Fort Knox might not in fact be there.

“We’re going to go to Fort Knox — the fabled Fort Knox — to make sure the gold is there,” Trump said at the time. “If the gold isn’t there, we’re going to be very upset,” he added.

Spot gold traded 1.5% higher at $3,814.82 an ounce as of 1:35 p.m. in London, paring some of its earlier gains.

Read the full article HERE.